Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Airport Lounge Service Market: $16.1B by 2034, 14.1% CAGR

Airport Lounge Service

Airport Lounge Service Market: $16.1B by 2034, 14.1% CAGR

Airport Lounge Service by Service Type (Business Lounges, VIP Lounges, Airline Lounges, Pay-per-use Lounges, Others), by Access Type (Membership Card, Pay-per-use, Invitation-based, Others), by Airport Type (Domestic Airport Lounges, International Airport Lounges), by End User (Airlines, Airports, Independent Operators, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 111

Key Insights into the Airport Lounge Service Market

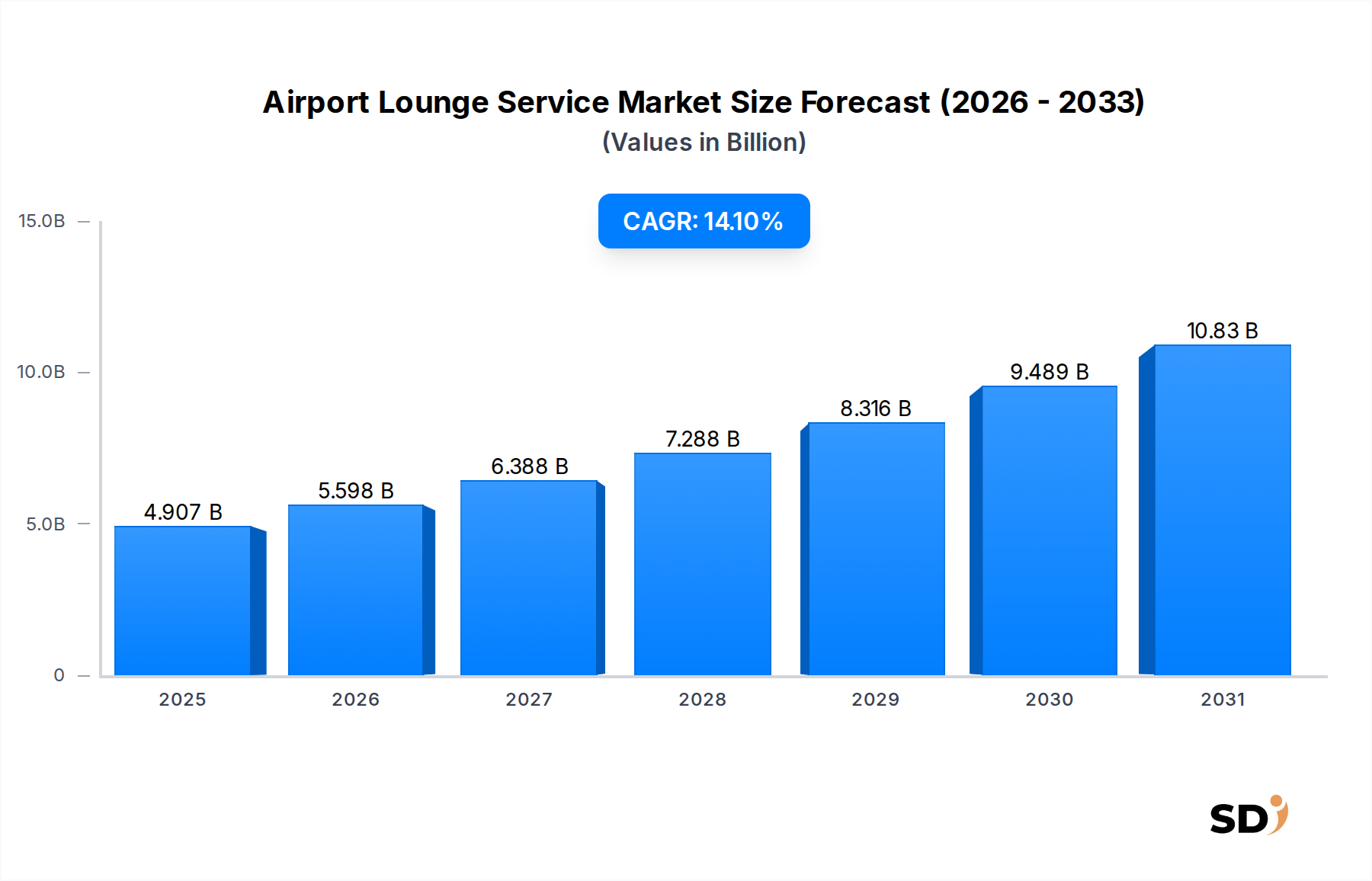

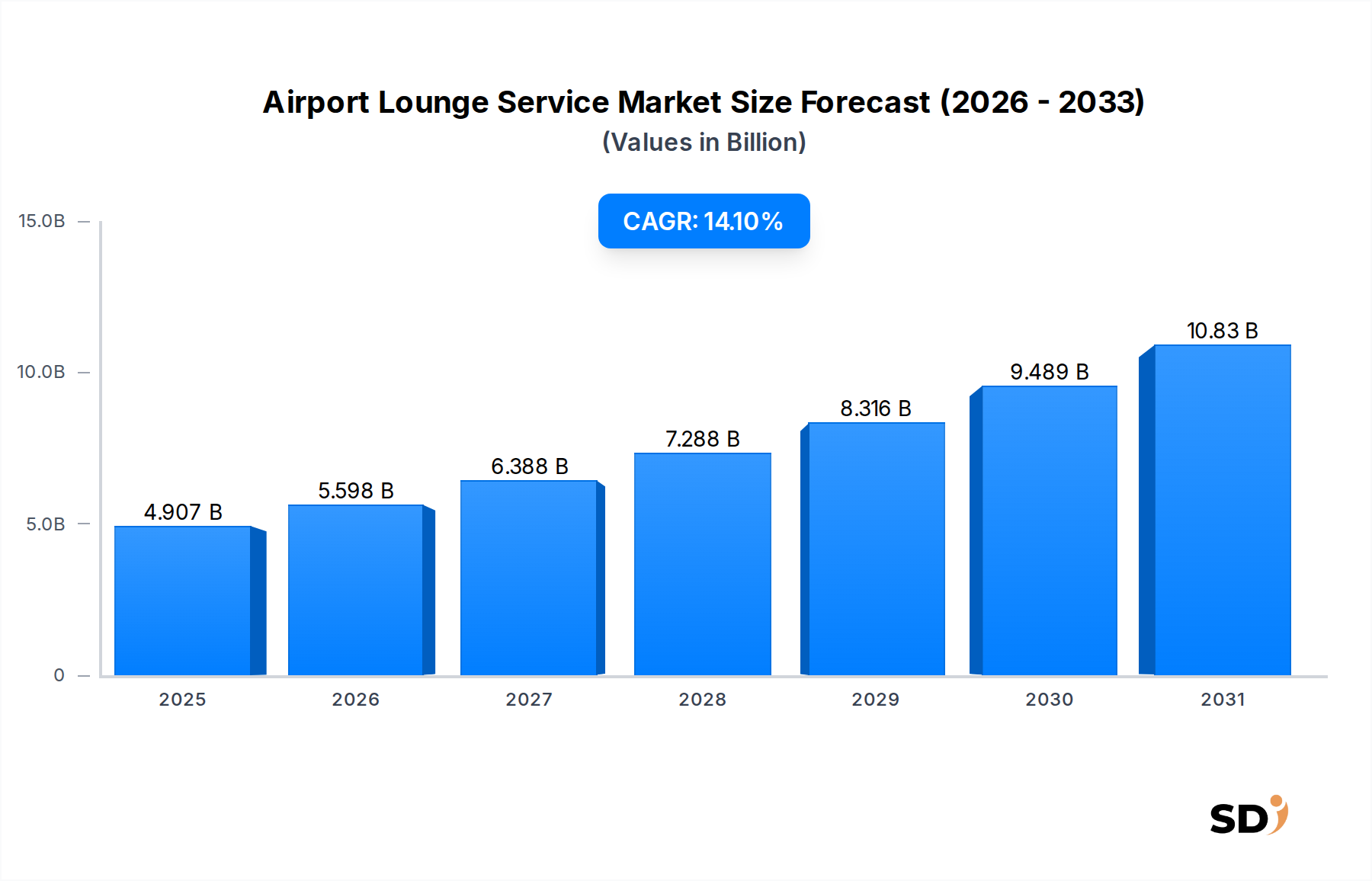

The global Airport Lounge Service Market is exhibiting robust growth, propelled by a confluence of factors including increasing air passenger traffic, a rising demand for premium travel experiences, and strategic expansions by key industry players. Valued at an estimated $4906.53 million in the base year 2025, the market is projected to expand significantly, demonstrating a compound annual growth rate (CAGR) of 14.1% through to 2034. This impressive growth trajectory underscores the evolving expectations of air travelers who increasingly seek comfort, productivity, and exclusivity pre-flight.

Airport Lounge Service Market Size (In Billion)

15.0B

10.0B

5.0B

0

4.907 B

2025

5.598 B

2026

6.388 B

2027

7.288 B

2028

8.316 B

2029

9.489 B

2030

10.83 B

2031

Key demand drivers for the Airport Lounge Service Market include the resurgence of the Business Travel Market, where corporate clients prioritize efficient and comfortable transit, alongside the burgeoning Leisure Travel Market, where individuals are more willing to pay for enhanced travel amenities. Furthermore, the expansion of global air routes, particularly in emerging economies, is creating new demand hubs. Macro tailwinds such as increasing disposable incomes in Asia Pacific and the Middle East, coupled with a growing focus on customer satisfaction by airlines and airport authorities, are providing substantial impetus. The competitive landscape is characterized by a mix of airline-owned lounges, independent operators, and alliances, all vying to offer differentiated services, from gourmet dining and spa facilities to dedicated workspaces and enhanced connectivity options. The integration of advanced technologies, such as seamless booking platforms and biometric access, is also playing a crucial role in modernizing lounge operations and enhancing the passenger experience, thereby contributing to the overall market expansion. The long-term outlook for the Airport Lounge Service Market remains highly positive, driven by continuous innovation in service offerings and a sustained global appetite for air travel.

Dominance of Airline Lounges in the Airport Lounge Service Market

Within the Airport Lounge Service Market, the 'Airline Lounges' sub-segment under Service Type currently holds a dominant share by revenue, a trend anticipated to continue throughout the forecast period. This dominance is primarily attributed to the historical provisioning of lounges as a loyalty benefit for airlines' premium passengers, frequent flyers, and elite status holders. Major global carriers like Emirates, Lufthansa Group, and Delta Air Lines operate extensive networks of lounges, often co-located at their hub airports, offering exclusive access to their loyal customer base. These lounges are integral to an airline's brand positioning and customer retention strategy, providing a seamless extension of the premium travel experience.

The widespread reach and established infrastructure of airline-operated lounges ensure a significant market footprint. These lounges are typically integrated into airline ticketing and loyalty programs, making them a default choice for a large segment of air travelers. While pay-per-use lounges and independent operators like Plaza Premium Group are rapidly expanding their footprint and diversifying access options, airline lounges continue to benefit from their deep integration into the Global Aviation Market ecosystem and strong brand recognition. The growth of this segment is closely tied to the overall growth of air travel and the increasing number of passengers opting for business or first-class tickets, as well as the enrollment in frequent flyer programs. Furthermore, airlines are continuously investing in upgrading their lounge facilities, incorporating modern designs, improved amenities, and personalized services to maintain their competitive edge. This ongoing investment, coupled with strategic partnerships and alliances (e.g., Star Alliance, SkyTeam, Oneworld), allows for broader accessibility to a diverse set of passengers, solidifying the 'Airline Lounges' segment's leading position within the Airport Lounge Service Market. Despite the rise of other access models, the intrinsic value proposition for airline loyalty program members remains a powerful driver for this segment's sustained dominance, though its growth rate might be marginally outpaced by more agile, independent operators catering to a broader demographic, including those within the Leisure Travel Market.

Key Market Drivers Influencing the Airport Lounge Service Market

The Airport Lounge Service Market is significantly influenced by several key drivers. Firstly, the burgeoning demand for a seamless and enhanced pre-flight experience is a primary catalyst. As global air passenger traffic continues its upward trajectory, with projections indicating a return to and exceeding pre-pandemic levels by 2025, the sheer volume of travelers seeking comfort and convenience directly fuels lounge demand. Travelers are increasingly willing to pay for amenities that alleviate the stress of air travel, such as quiet spaces, quality dining, and dedicated workspaces, transforming lounges from a luxury into a preferred travel component.

Secondly, the competitive pressure among airlines and airports to differentiate their offerings plays a crucial role. In a highly competitive Global Aviation Market, providing superior lounge services is a key strategy for customer acquisition and retention. Airlines invest heavily in their lounges to attract high-value passengers, offering exclusive benefits that strengthen brand loyalty. For example, the continuous upgrade of facilities and service portfolios, mirroring trends seen in the broader Premium Airport Service Market, helps maintain a competitive edge. This dynamic often leads to a 'race to the top' in terms of luxury and service quality.

Thirdly, the expansion of independent lounge networks and pay-per-use models is democratizing access and widening the customer base. Historically, lounge access was primarily reserved for premium class passengers or elite loyalty members. However, the rise of providers like Collinson Group (Priority Pass) and Plaza Premium Group, along with growing acceptance of day passes, has made lounges accessible to a much broader demographic, including the robust Leisure Travel Market. This expansion of accessibility removes traditional barriers, allowing more travelers to experience lounge benefits and contributing significantly to the overall revenue generation of the Airport Lounge Service Market. The integration with credit card benefits further lowers the barrier to entry.

Competitive Ecosystem of Airport Lounge Service Market

The Airport Lounge Service Market is characterized by a diverse competitive landscape, comprising major airlines, independent operators, and airport authorities. Strategic alliances, digital integration, and service diversification are key competitive strategies.

Plaza Premium Group: A global leader in independent airport lounge services, known for its extensive network of pay-per-use lounges and innovative offerings, targeting both leisure and business travelers seeking premium airport experiences.

Airport Dimensions: An integral part of the Collinson Group, this entity focuses on creating and managing airport experiences, including lounges, with a strong emphasis on digital solutions and partnerships to enhance passenger dwell time and satisfaction.

SATS Ltd: A leading provider of gateway services and food solutions, SATS operates lounges primarily in Asia, leveraging its integrated airport operations to offer comprehensive passenger and catering services.

Lufthansa Group: A major European airline group, operating numerous exclusive lounges across its global network for its premium passengers and frequent flyers, prioritizing comfort and efficiency for its brand loyalists.

American Express: A significant player through its Centurion Lounge network, offering exclusive, high-end lounge access to its premium cardholders, which drives customer loyalty and reinforces its luxury brand image in the travel sector.

Delta Air Lines: Through its Delta Sky Club lounges, Delta provides a crucial amenity for its Medallion members and premium cabin passengers, enhancing the overall travel experience and cementing its position in the competitive US aviation market.

Emirates: Renowned for its luxurious lounges, particularly at its Dubai hub, Emirates offers an opulent pre-flight experience that aligns with its premium global brand image, catering to high-spending international travelers.

Qantas Airways: As Australia's flag carrier, Qantas operates an extensive lounge network that forms a vital part of its customer loyalty program, providing comfortable and well-appointed spaces for its domestic and international passengers.

Collinson Group: A dominant force in the loyalty and benefits sector, Collinson operates Priority Pass, a global program offering access to a vast network of lounges, significantly expanding options for frequent travelers.

Swissport International: Primarily known for its ground handling and cargo services, Swissport also manages and operates a number of lounges, particularly for third-party airlines, contributing to the broader Airport Concession Market.

Others: This category includes numerous smaller independent lounge operators, regional airlines, and airport authorities that manage their own lounge facilities, collectively contributing to the fragmented yet growing Airport Lounge Service Market.

Recent Developments & Milestones in Airport Lounge Service Market

January 2024: Plaza Premium Group announced a strategic partnership with a major credit card provider to expand complimentary lounge access for premium cardholders across its Asia Pacific network, enhancing market reach and customer engagement.

November 2023: Delta Air Lines unveiled its newest flagship Delta Sky Club lounge at a key international hub, featuring expanded seating, enhanced dining options, and local art installations, signaling continued investment in premium passenger experience.

September 2023: Collinson Group's Priority Pass program surpassed the milestone of offering access to over 1,500 airport lounges and experiences worldwide, solidifying its position as a leading independent lounge access provider in the Airport Lounge Service Market.

July 2023: American Express expanded its Centurion Lounge network with a new opening in a high-traffic European airport, underscoring its commitment to providing exclusive benefits to its premium cardholders.

May 2023: Several independent lounge operators began trials of Biometric Access System Market technologies for seamless entry, aiming to reduce wait times and improve operational efficiency across their facilities.

March 2023: A leading Middle Eastern airline invested significantly in the renovation and expansion of its business and first-class lounges at its primary hub, introducing new wellness facilities and dedicated quiet zones.

February 2023: Airport Dimensions partnered with an innovative food & beverage technology company to launch new digital ordering and delivery services within select lounges, improving the customer experience and operational agility within the Airport Concession Market.

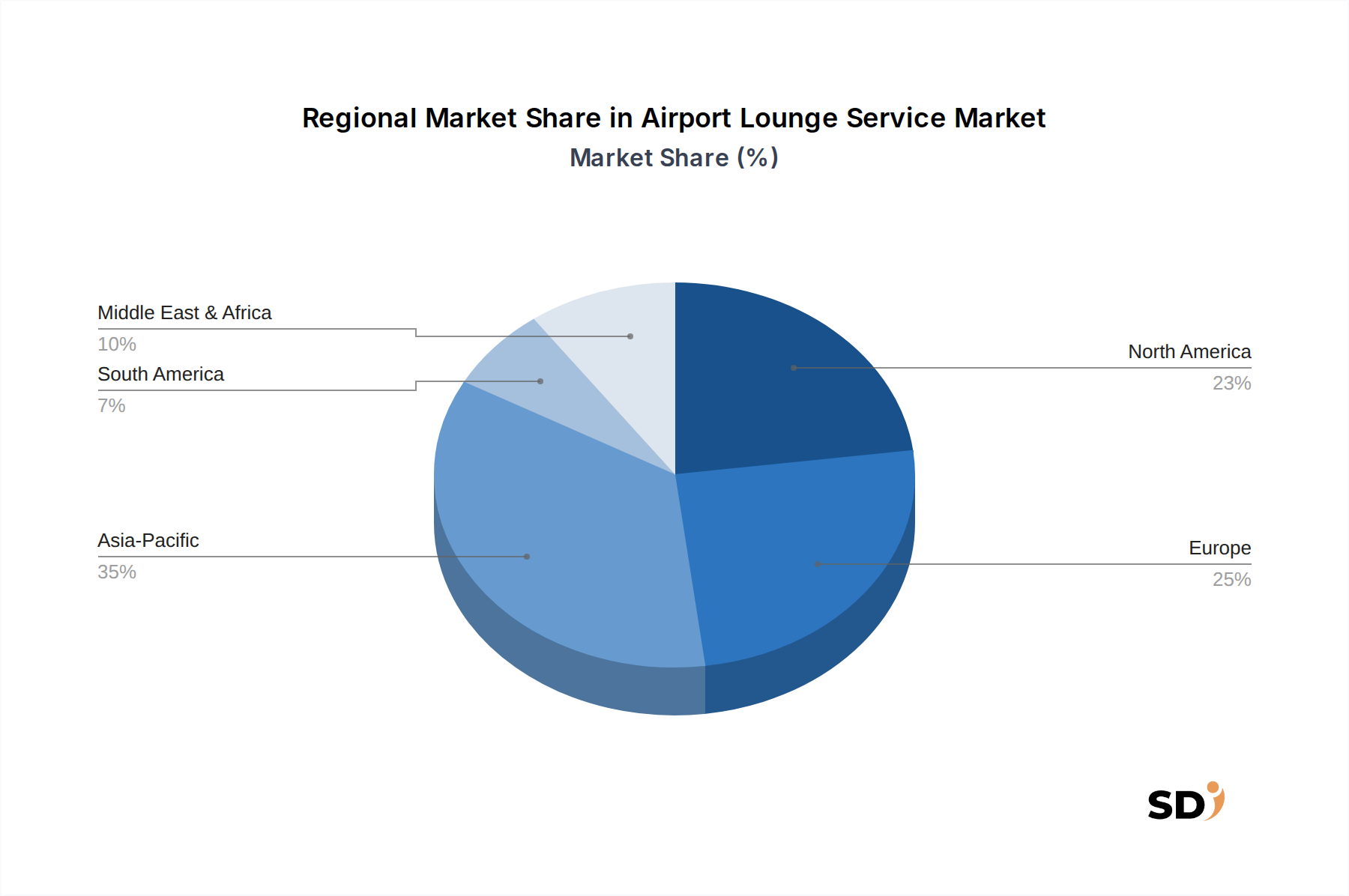

Regional Market Breakdown for Airport Lounge Service Market

The Airport Lounge Service Market demonstrates varied growth dynamics across key global regions, driven by distinct economic, demographic, and travel trends. North America and Europe, representing mature aviation markets, hold substantial revenue shares due to established airline networks, high volumes of business and leisure travel, and a strong presence of both airline-owned and independent lounge operators. In North America, the significant uptake of premium credit cards offering lounge access is a primary demand driver, alongside the robust Business Travel Market. Similarly, in Europe, intercontinental travel and the expansion of low-cost carrier premium offerings contribute to stable demand. These regions benefit from a high penetration of frequent flyer programs and an established culture of air travel, though their growth rates may be more moderate compared to emerging markets.

Asia Pacific is identified as the fastest-growing region within the Airport Lounge Service Market, propelled by rapidly increasing disposable incomes, expanding middle-class populations, and significant investments in airport infrastructure. Countries like China and India are witnessing unprecedented growth in domestic and international air travel, leading to a surge in demand for premium airport services. This region is also a hotspot for the expansion of independent lounge networks and the adoption of technologies, including advancements in the Digital Travel Platform Market, to enhance passenger experience. The Middle East & Africa region also shows strong growth potential, primarily driven by major aviation hubs in the GCC countries that serve as critical transit points for global travel. Investments in luxury travel and hospitality are fostering an environment conducive to the expansion of premium lounge services. In contrast, while South America and other parts of Africa exhibit growth, they currently hold smaller revenue shares, with development tied to economic stability and infrastructure improvements. The competitive landscape in each region is shaped by local airline dominance, the presence of global independent operators, and regulatory frameworks affecting the Airport Concession Market.

Pricing Dynamics & Margin Pressure in Airport Lounge Service Market

Pricing dynamics within the Airport Lounge Service Market are complex, influenced by a blend of access models, competitive intensity, and perceived value. Average selling prices (ASPs) for pay-per-use lounge access typically range from $30 to $75, varying significantly based on location, amenities offered, and duration of stay. Membership-based access, often through credit card partnerships or loyalty programs, generates revenue through annual fees or per-visit charges negotiated at bulk rates. The margin structure is generally healthy, especially for well-managed independent lounges and premium airline lounges, driven by economies of scale in F&B procurement, efficient staffing, and high utilization rates. However, margin pressure can arise from several factors.

Key cost levers include rent and operational expenses at airports, which can be substantial, particularly at prime locations. Staffing costs, especially for highly trained service personnel, also represent a significant expenditure. Additionally, the constant need to upgrade facilities and refresh F&B offerings to meet evolving customer expectations – a trend prevalent across the Premium Airport Service Market – requires continuous capital investment, which can compress margins if not managed effectively. Competitive intensity from other lounge providers and alternative airport amenities (e.g., enhanced duty-free areas, upscale restaurants) can limit pricing power. Furthermore, the reliance on credit card partnerships for a significant portion of access can introduce complex revenue-sharing models and negotiating pressure. The market is also sensitive to commodity cycles impacting food and beverage costs, though these are typically a smaller component compared to fixed operational costs. Overall, maintaining a balance between premium offerings and cost efficiency is crucial for profitability in the Airport Lounge Service Market, with digital solutions and strategic partnerships playing a vital role in optimizing revenue streams and managing expenses.

Sustainability & ESG Pressures on Airport Lounge Service Market

The Airport Lounge Service Market is increasingly facing scrutiny and pressure related to sustainability and ESG (Environmental, Social, and Governance) factors. As part of the broader Global Aviation Market, lounges are being pushed to align with overarching industry goals for environmental stewardship and social responsibility. Environmental regulations, particularly those targeting carbon emissions and waste reduction, are reshaping operational practices. Lounges are examining their energy consumption, waste management protocols (especially food waste), and sourcing of materials and products.

The drive towards circular economy mandates influences procurement decisions, with a growing preference for suppliers offering sustainable and ethically produced goods, ranging from F&B to furniture and amenities. Many lounge operators are now prioritizing locally sourced, organic food items, and implementing recycling programs for plastics and other consumables. Carbon targets, set by airports and airlines, indirectly impact lounge operations, encouraging investments in energy-efficient appliances, LED lighting, and even renewable energy sources where feasible. The transition towards more sustainable packaging and reduced single-use plastics is also a significant trend. From a social perspective, fair labor practices, employee well-being, and diversity and inclusion initiatives are becoming increasingly important. ESG investor criteria are also playing a pivotal role; investors are more likely to support companies demonstrating robust ESG performance, pushing lounge operators and their parent companies to integrate these considerations into their business strategies. For instance, the selection of materials for new lounge constructions or renovations often now includes certifications for environmental impact. Operators in the Airport Concession Market are finding that demonstrating a commitment to sustainability not only meets regulatory and investor expectations but also resonates positively with a growing segment of environmentally conscious travelers, potentially enhancing brand reputation and customer loyalty. This holistic approach to ESG is redefining product development and procurement within the Airport Lounge Service Market, driving innovation towards more responsible and sustainable practices.

Airport Lounge Service Segmentation

1. Service Type

1.1. Business Lounges

1.2. VIP Lounges

1.3. Airline Lounges

1.4. Pay-per-use Lounges

1.5. Others

2. Access Type

2.1. Membership Card

2.2. Pay-per-use

2.3. Invitation-based

2.4. Others

3. Airport Type

3.1. Domestic Airport Lounges

3.2. International Airport Lounges

4. End User

4.1. Airlines

4.2. Airports

4.3. Independent Operators

4.4. Others

Airport Lounge Service Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Airport Lounge Service REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 14.1% from 2020-2034

Segmentation

By Service Type

Business Lounges

VIP Lounges

Airline Lounges

Pay-per-use Lounges

Others

By Access Type

Membership Card

Pay-per-use

Invitation-based

Others

By Airport Type

Domestic Airport Lounges

International Airport Lounges

By End User

Airlines

Airports

Independent Operators

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Service Type

5.1.1. Business Lounges

5.1.2. VIP Lounges

5.1.3. Airline Lounges

5.1.4. Pay-per-use Lounges

5.1.5. Others

5.2. Market Analysis, Insights and Forecast - by Access Type

5.2.1. Membership Card

5.2.2. Pay-per-use

5.2.3. Invitation-based

5.2.4. Others

5.3. Market Analysis, Insights and Forecast - by Airport Type

5.3.1. Domestic Airport Lounges

5.3.2. International Airport Lounges

5.4. Market Analysis, Insights and Forecast - by End User

5.4.1. Airlines

5.4.2. Airports

5.4.3. Independent Operators

5.4.4. Others

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Service Type

6.1.1. Business Lounges

6.1.2. VIP Lounges

6.1.3. Airline Lounges

6.1.4. Pay-per-use Lounges

6.1.5. Others

6.2. Market Analysis, Insights and Forecast - by Access Type

6.2.1. Membership Card

6.2.2. Pay-per-use

6.2.3. Invitation-based

6.2.4. Others

6.3. Market Analysis, Insights and Forecast - by Airport Type

6.3.1. Domestic Airport Lounges

6.3.2. International Airport Lounges

6.4. Market Analysis, Insights and Forecast - by End User

6.4.1. Airlines

6.4.2. Airports

6.4.3. Independent Operators

6.4.4. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Service Type

7.1.1. Business Lounges

7.1.2. VIP Lounges

7.1.3. Airline Lounges

7.1.4. Pay-per-use Lounges

7.1.5. Others

7.2. Market Analysis, Insights and Forecast - by Access Type

7.2.1. Membership Card

7.2.2. Pay-per-use

7.2.3. Invitation-based

7.2.4. Others

7.3. Market Analysis, Insights and Forecast - by Airport Type

7.3.1. Domestic Airport Lounges

7.3.2. International Airport Lounges

7.4. Market Analysis, Insights and Forecast - by End User

7.4.1. Airlines

7.4.2. Airports

7.4.3. Independent Operators

7.4.4. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Service Type

8.1.1. Business Lounges

8.1.2. VIP Lounges

8.1.3. Airline Lounges

8.1.4. Pay-per-use Lounges

8.1.5. Others

8.2. Market Analysis, Insights and Forecast - by Access Type

8.2.1. Membership Card

8.2.2. Pay-per-use

8.2.3. Invitation-based

8.2.4. Others

8.3. Market Analysis, Insights and Forecast - by Airport Type

8.3.1. Domestic Airport Lounges

8.3.2. International Airport Lounges

8.4. Market Analysis, Insights and Forecast - by End User

8.4.1. Airlines

8.4.2. Airports

8.4.3. Independent Operators

8.4.4. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Service Type

9.1.1. Business Lounges

9.1.2. VIP Lounges

9.1.3. Airline Lounges

9.1.4. Pay-per-use Lounges

9.1.5. Others

9.2. Market Analysis, Insights and Forecast - by Access Type

9.2.1. Membership Card

9.2.2. Pay-per-use

9.2.3. Invitation-based

9.2.4. Others

9.3. Market Analysis, Insights and Forecast - by Airport Type

9.3.1. Domestic Airport Lounges

9.3.2. International Airport Lounges

9.4. Market Analysis, Insights and Forecast - by End User

9.4.1. Airlines

9.4.2. Airports

9.4.3. Independent Operators

9.4.4. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Service Type

10.1.1. Business Lounges

10.1.2. VIP Lounges

10.1.3. Airline Lounges

10.1.4. Pay-per-use Lounges

10.1.5. Others

10.2. Market Analysis, Insights and Forecast - by Access Type

10.2.1. Membership Card

10.2.2. Pay-per-use

10.2.3. Invitation-based

10.2.4. Others

10.3. Market Analysis, Insights and Forecast - by Airport Type

10.3.1. Domestic Airport Lounges

10.3.2. International Airport Lounges

10.4. Market Analysis, Insights and Forecast - by End User

10.4.1. Airlines

10.4.2. Airports

10.4.3. Independent Operators

10.4.4. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Plaza Premium Group

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Airport Dimensions

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. SATS Ltd

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Lufthansa Group

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. American Express

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Delta Air Lines

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Emirates

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Qantas Airways

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Collinson Group

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Swissport International

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Others

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Service Type 2025 & 2033

Figure 3: Revenue Share (%), by Service Type 2025 & 2033

Figure 4: Revenue (million), by Access Type 2025 & 2033

Figure 5: Revenue Share (%), by Access Type 2025 & 2033

Figure 6: Revenue (million), by Airport Type 2025 & 2033

Figure 7: Revenue Share (%), by Airport Type 2025 & 2033

Figure 8: Revenue (million), by End User 2025 & 2033

Figure 9: Revenue Share (%), by End User 2025 & 2033

Figure 10: Revenue (million), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (million), by Service Type 2025 & 2033

Figure 13: Revenue Share (%), by Service Type 2025 & 2033

Figure 14: Revenue (million), by Access Type 2025 & 2033

Figure 15: Revenue Share (%), by Access Type 2025 & 2033

Figure 16: Revenue (million), by Airport Type 2025 & 2033

Figure 17: Revenue Share (%), by Airport Type 2025 & 2033

Figure 18: Revenue (million), by End User 2025 & 2033

Figure 19: Revenue Share (%), by End User 2025 & 2033

Figure 20: Revenue (million), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (million), by Service Type 2025 & 2033

Figure 23: Revenue Share (%), by Service Type 2025 & 2033

Figure 24: Revenue (million), by Access Type 2025 & 2033

Figure 25: Revenue Share (%), by Access Type 2025 & 2033

Figure 26: Revenue (million), by Airport Type 2025 & 2033

Figure 27: Revenue Share (%), by Airport Type 2025 & 2033

Figure 28: Revenue (million), by End User 2025 & 2033

Figure 29: Revenue Share (%), by End User 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (million), by Service Type 2025 & 2033

Figure 33: Revenue Share (%), by Service Type 2025 & 2033

Figure 34: Revenue (million), by Access Type 2025 & 2033

Figure 35: Revenue Share (%), by Access Type 2025 & 2033

Figure 36: Revenue (million), by Airport Type 2025 & 2033

Figure 37: Revenue Share (%), by Airport Type 2025 & 2033

Figure 38: Revenue (million), by End User 2025 & 2033

Figure 39: Revenue Share (%), by End User 2025 & 2033

Figure 40: Revenue (million), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (million), by Service Type 2025 & 2033

Figure 43: Revenue Share (%), by Service Type 2025 & 2033

Figure 44: Revenue (million), by Access Type 2025 & 2033

Figure 45: Revenue Share (%), by Access Type 2025 & 2033

Figure 46: Revenue (million), by Airport Type 2025 & 2033

Figure 47: Revenue Share (%), by Airport Type 2025 & 2033

Figure 48: Revenue (million), by End User 2025 & 2033

Figure 49: Revenue Share (%), by End User 2025 & 2033

Figure 50: Revenue (million), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Service Type 2020 & 2033

Table 2: Revenue million Forecast, by Access Type 2020 & 2033

Table 3: Revenue million Forecast, by Airport Type 2020 & 2033

Table 4: Revenue million Forecast, by End User 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Revenue million Forecast, by Service Type 2020 & 2033

Table 7: Revenue million Forecast, by Access Type 2020 & 2033

Table 8: Revenue million Forecast, by Airport Type 2020 & 2033

Table 9: Revenue million Forecast, by End User 2020 & 2033

Table 10: Revenue million Forecast, by Country 2020 & 2033

Table 11: Revenue (million) Forecast, by Application 2020 & 2033

Table 12: Revenue (million) Forecast, by Application 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue million Forecast, by Service Type 2020 & 2033

Table 15: Revenue million Forecast, by Access Type 2020 & 2033

Table 16: Revenue million Forecast, by Airport Type 2020 & 2033

Table 17: Revenue million Forecast, by End User 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue million Forecast, by Service Type 2020 & 2033

Table 23: Revenue million Forecast, by Access Type 2020 & 2033

Table 24: Revenue million Forecast, by Airport Type 2020 & 2033

Table 25: Revenue million Forecast, by End User 2020 & 2033

Table 26: Revenue million Forecast, by Country 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue (million) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Revenue (million) Forecast, by Application 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue million Forecast, by Service Type 2020 & 2033

Table 37: Revenue million Forecast, by Access Type 2020 & 2033

Table 38: Revenue million Forecast, by Airport Type 2020 & 2033

Table 39: Revenue million Forecast, by End User 2020 & 2033

Table 40: Revenue million Forecast, by Country 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue million Forecast, by Service Type 2020 & 2033

Table 48: Revenue million Forecast, by Access Type 2020 & 2033

Table 49: Revenue million Forecast, by Airport Type 2020 & 2033

Table 50: Revenue million Forecast, by End User 2020 & 2033

Table 51: Revenue million Forecast, by Country 2020 & 2033

Table 52: Revenue (million) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Revenue (million) Forecast, by Application 2020 & 2033

Table 55: Revenue (million) Forecast, by Application 2020 & 2033

Table 56: Revenue (million) Forecast, by Application 2020 & 2033

Table 57: Revenue (million) Forecast, by Application 2020 & 2033

Table 58: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market sizing and forecasting are predominantly driven by rigorous primary research, constituting 70-80% of our total research effort. This extensive engagement ensures real-time insights, validation of secondary data, and nuanced understanding of market dynamics directly from industry participants. Our primary research strategy involves in-depth interviews conducted via telephonic conversations, virtual meetings, and, where feasible, face-to-face interactions with key stakeholders across the airport lounge service value chain. This iterative process allows for the refinement of hypotheses and the discovery of emergent trends.

Key stakeholders interviewed include:

VP of Commercial Strategy & Airport Services

Director of Concessions & Passenger Experience

Global Head of Lounge Operations

Senior Product Manager, Premium Travel Benefits

Companies targeted for primary interviews span various crucial segments of the market:

Independent Airport Lounge Operators (e.g., Plaza Premium Group, Aspire Lounges)

Major Global Airlines (e.g., Delta Air Lines, British Airways, Qatar Airways)

Premium Credit Card Issuers & Loyalty Program Providers

20%

Airport Concession Developers/Managers

10%

Secondary Research & Industry Benchmarking

The remaining 20-30% of our research is dedicated to comprehensive secondary research and industry benchmarking. This phase lays the foundational understanding of the market, identifies key trends, and provides a robust dataset for triangulation. Our secondary research methodology strictly avoids data from other market research websites to ensure originality and independent analysis. Instead, we leverage authoritative and credible sources, including:

Financial Databases: Bloomberg, Factiva, Hoovers, and PitchBook for company financials, investment trends, and strategic developments.

Government & Regulatory Bodies: Official publications, reports, and statistical data from national and international government agencies (e.g., U.S. Department of Transportation, Eurostat). For instance, U.S. Department of Transportation.

Industry Associations & Organizations: Publications, annual reports, whitepapers, and statistical yearbooks from globally recognized industry bodies. These include:

Corporate Filings & Investor Presentations: Annual reports (10-K, 20-F), quarterly earnings calls transcripts, and investor presentations of publicly traded companies within the value chain.

Academic Research & White Papers: Peer-reviewed journals and reputable thought leadership pieces relevant to aviation, hospitality, and passenger experience.

Demand Modeling & Market Estimation

Our market estimation employs a dual-pronged approach, utilizing both top-down and bottom-up methodologies, which are then rigorously validated through multi-level data triangulation. This ensures a comprehensive and robust market size calculation and forecast.

Bottom-Up Approach: This method involves aggregating granular data points to build the total market size. Key metrics and variables used for this approach in the airport lounge market include:

Number of Operational Airport Lounges (segmented by service type and airport type)

Average Annual Passenger Throughput (by airport type, region, and segment e.g., premium vs. economy)

Average Revenue per Lounge Visit (ARPAM) - segmented by access type (e.g., membership, pay-per-use, invitation-based) and lounge type

Penetration Rate of Lounge Access among Eligible Travelers (e.g., premium passengers, loyalty program members)

Top-Down Approach: This approach starts with broader market indicators (e.g., global air travel passenger numbers, travel retail market size) and segments them down to derive the specific airport lounge market size, cross-referencing with industry reports and expert opinions.

Multi-Level Data Triangulation: Data derived from both primary and secondary sources, and from top-down and bottom-up calculations, are meticulously cross-referenced and validated at various levels (service type, access type, airport type, end-user, and regional segments) to eliminate discrepancies and enhance accuracy.

Data Accuracy & Quality Check

Our commitment to data integrity is paramount. We guarantee an estimated data accuracy level of 85-90% for our market figures and forecasts. This high level of precision is achieved through:

Expert Validation: Insights and data points collected during primary research are continuously validated against secondary research findings and through subsequent expert interviews.

Proprietary Analytical Models: We utilize sophisticated proprietary statistical and forecasting models, built specifically for the nuances of the aviation and travel services industry, to project future market trends.

Continuous Updates: Every report is meticulously updated up to the date of purchase, ensuring that our clients receive the most current market intelligence, reflecting the latest industry developments, economic shifts, and regulatory changes.

Peer Review: All research findings and market estimates undergo a stringent internal peer review process by senior analysts to ensure methodological rigor and analytical soundness.

Frequently Asked Questions

1. What is the investment outlook for the Airport Lounge Service market?

The market exhibits a robust investment outlook, projected to reach $16.1 billion by 2034 with a 14.1% CAGR. This growth attracts capital toward enhancing premium passenger experiences and expanding global lounge networks. Companies like Plaza Premium Group and Collinson Group actively invest in new facilities and technology.

2. What are the primary growth drivers for airport lounge services?

Primary drivers include the global increase in air travel and a rising demand for premium amenities. The expansion of international airport lounges and the popularity of pay-per-use access models further propel market expansion. Airlines and independent operators are investing to enhance passenger comfort and loyalty.

3. What are the main competitive barriers in the Airport Lounge Service sector?

Significant barriers include the high capital investment required for facility development and maintenance, along with securing prime airport real estate. Established brands like American Express and Lufthansa Group benefit from strong brand loyalty and extensive global networks, creating substantial competitive moats. Operational complexities and regulatory compliance also pose entry challenges.

4. Which recent developments impact the airport lounge service market?

Recent developments include strategic partnerships between airlines and independent operators, and the increasing adoption of digital access technologies. Companies like Airport Dimensions and Swissport International are expanding their service portfolios and geographic reach to capture new market segments. Consolidation or new product launches by key players are continuous.

5. How are consumer behaviors shifting regarding airport lounge usage?

Consumer behavior is shifting towards seeking enhanced comfort, connectivity, and personalized experiences before flights. There's a growing preference for pay-per-use and membership card access, especially among frequent travelers and business clients. This trend drives demand for diverse offerings beyond traditional airline lounges, including VIP and business lounge types.

6. What are the post-pandemic recovery trends for airport lounge services?

The post-pandemic recovery shows strong resilience in the airport lounge service market, with the 14.1% CAGR signaling robust long-term growth. Increased emphasis on health protocols, contactless services, and premium amenities are key structural shifts. Both domestic and international airport lounges are experiencing renewed demand as global travel resumes.