Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Airline Ticketing System Trends: Market Analysis & 2034 Forecasts

Airline Ticketing System

Airline Ticketing System Trends: Market Analysis & 2034 Forecasts

Airline Ticketing System by Component (Software, Hardware, Services), by Deployment Mode (Cloud-based, On-premises, Hybrid), by Platform (Desktop-Based Systems, Mobile-Based Systems, Web-Based Systems), by End User (Commercial Airlines, Low-Cost Carriers (LCCs), Charter Airlines, Cargo Airlines, Travel Agencies, Others), by Booking Channel (Online Booking, Offline Booking), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 106

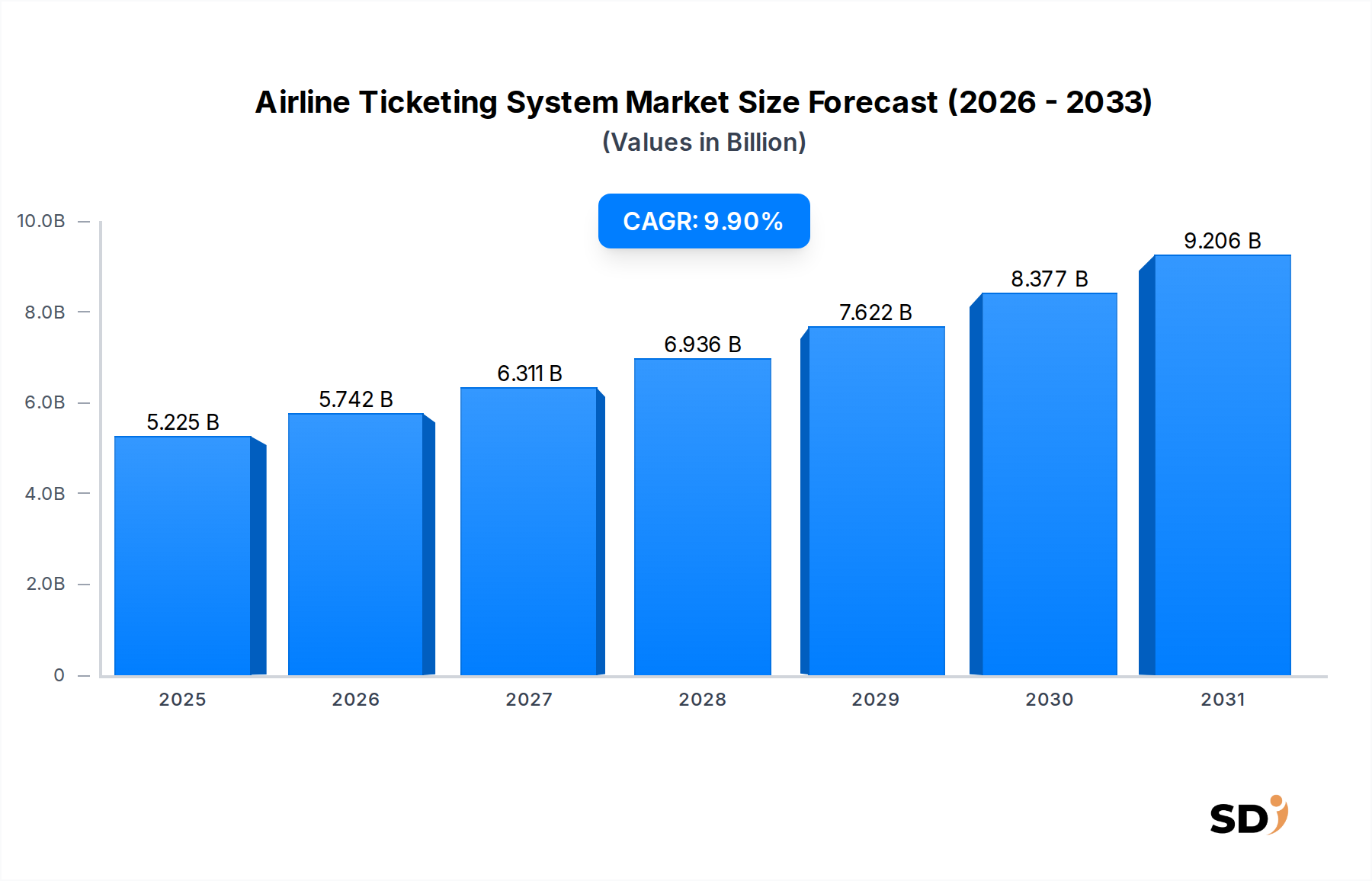

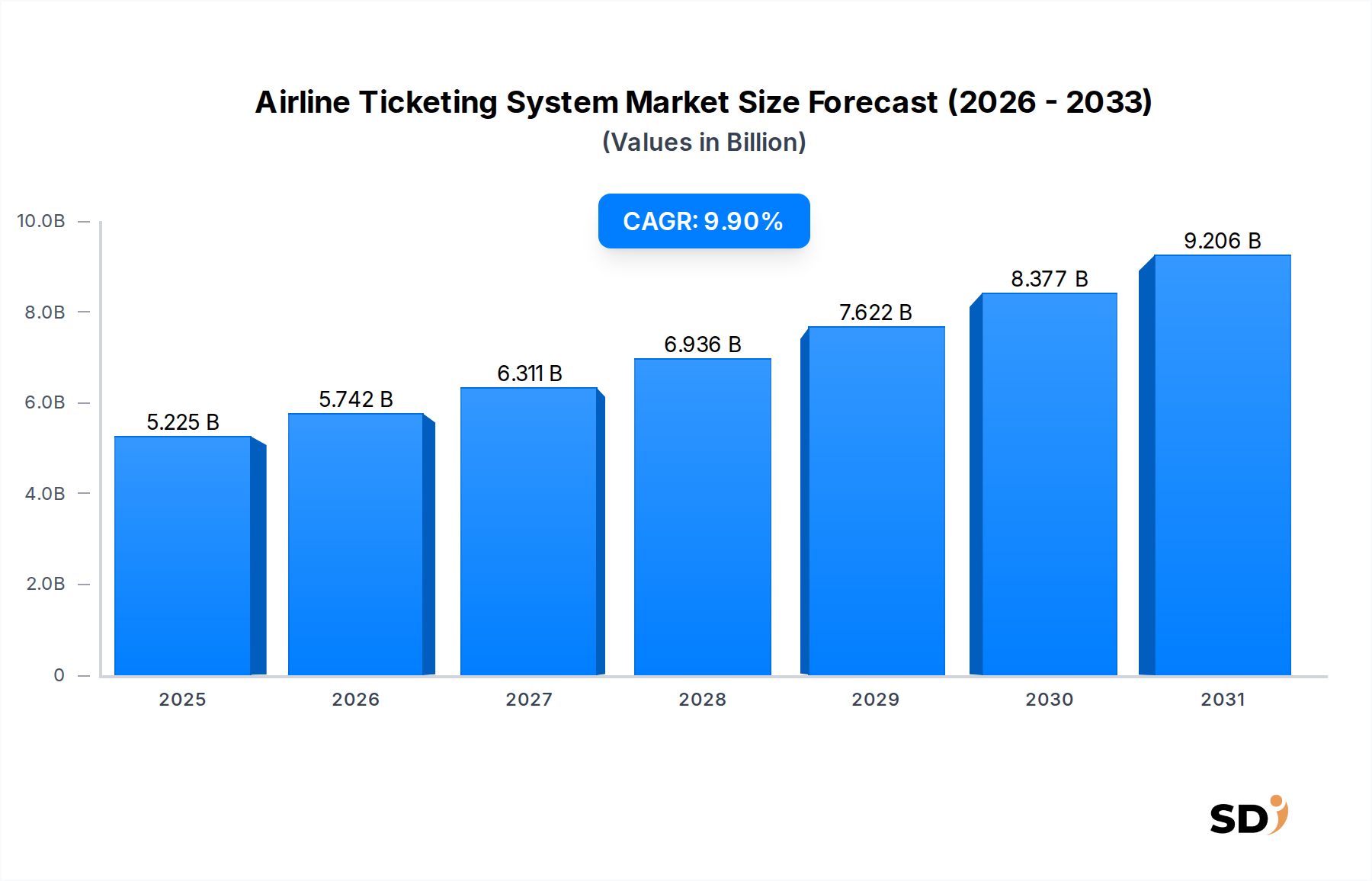

The global Airline Ticketing System Market achieved a valuation of $5,225 million in 2024. Projections indicate substantial expansion, with the market anticipated to reach approximately $13,508 million by 2034, advancing at a robust Compound Annual Growth Rate (CAGR) of 9.9% over the forecast period. This growth trajectory is primarily propelled by the escalating demand for streamlined, efficient, and personalized air travel booking experiences. A pivotal driver is the ongoing Digital Transformation Market within the aviation sector, compelling airlines and travel agencies to upgrade legacy systems to cloud-native and AI-powered platforms. The robust recovery and sustained growth in global air passenger traffic, particularly from emerging economies, provide a significant tailwind.

Airline Ticketing System Market Size (In Billion)

10.0B

8.0B

6.0B

4.0B

2.0B

0

5.225 B

2025

5.742 B

2026

6.311 B

2027

6.936 B

2028

7.622 B

2029

8.377 B

2030

9.206 B

2031

Technological advancements are at the core of this market's evolution. The pervasive shift towards cloud-based deployments offers scalability, enhanced data security, and reduced operational costs, making it an attractive option for carriers of all sizes. Furthermore, the increasing penetration of Mobile Applications Market for booking, check-in, and ancillary services is reshaping consumer behavior, necessitating sophisticated mobile-compatible ticketing solutions. Airlines are also heavily investing in Data Analytics Market capabilities embedded within ticketing systems to optimize pricing strategies, manage inventory dynamically, and offer hyper-personalized services, thereby enhancing customer loyalty and revenue streams. The imperative for real-time data processing and seamless integration across various travel ecosystem components further underscores the market's expansion. Geographically, while mature markets focus on system optimization and personalization, emerging regions are characterized by new route development and a surge in first-time flyers, driving demand for scalable and accessible ticketing infrastructure. The competitive landscape is dynamic, with established GDS providers and new technology entrants vying for market share through innovation and strategic partnerships.

Software Segment Dominance in Airline Ticketing System Market

The Software component segment stands as the unequivocal dominant force within the Airline Ticketing System Market, commanding the largest revenue share and exhibiting consistent growth. This supremacy is attributable to the inherent nature of ticketing operations, which are fundamentally driven by complex algorithms, database management, and user interface functionalities. Core functionalities such as inventory management, fare calculation, booking, payment processing, and customer relationship management are all software-centric. The sophistication required to handle global distribution, dynamic pricing, interlining agreements, and ancillary service integration necessitates advanced software solutions. This segment is not merely about static programs but encompasses a continuous development cycle, including regular updates, security patches, and feature enhancements to meet evolving industry standards and consumer demands.

Key players in this dominant segment include global distribution system (GDS) providers like Amadeus, Sabre Corporation, and Travelport, whose platforms serve as central hubs connecting airlines with travel agents and online travel agencies worldwide. These companies continuously invest heavily in research and development to offer next-generation solutions, including NDC (New Distribution Capability)-compliant APIs and AI-driven personalization engines. Beyond the GDS giants, specialized airline IT solution providers such as Navitaire, SITA, and IBS Software offer proprietary software suites tailored for specific airline models, including low-cost carriers (LCCs) and full-service network carriers. The increasing adoption of the Cloud Computing Market paradigm is further bolstering the Software segment's dominance, enabling Software-as-a-Service (SaaS) models that offer greater flexibility, scalability, and cost-efficiency for airlines. This shift allows airlines to access cutting-edge functionalities without significant upfront capital expenditure on hardware infrastructure, thereby lowering barriers to entry for advanced ticketing capabilities. Moreover, the critical need for integration with other airline operational systems—from flight operations and crew management to loyalty programs—ensures that the underlying software architecture remains the primary value driver. The Software Market for airline ticketing is not merely growing in size but also in its complexity and integration capabilities, solidifying its dominant position.

Key Market Drivers for Airline Ticketing System Market

The Airline Ticketing System Market is primarily driven by several critical factors, each contributing to its sustained expansion. A significant driver is the increasing global air passenger traffic. Following a period of disruption, the Airline Industry Market is witnessing a strong resurgence, with passenger volumes steadily approaching and, in some regions, surpassing pre-pandemic levels. This surge in travel directly translates into higher demand for efficient and robust ticketing systems capable of handling increased transaction volumes and complex routing. For instance, IATA projects global passenger numbers to reach 4.7 billion in 2024, exceeding the 4.5 billion registered in 2019, underscoring the necessity for scalable ticketing infrastructure.

Another pivotal driver is the relentless pursuit of operational efficiency and cost reduction by airlines. In a highly competitive environment, airlines leverage advanced ticketing systems to optimize inventory management, implement dynamic pricing models, and automate various customer service functions, thereby minimizing manual intervention and associated costs. The push for direct booking channels and personalized customer experiences is also a substantial catalyst. Airlines are increasingly investing in proprietary Online Booking Market portals and mobile applications to foster direct relationships with customers, bypass GDS fees, and offer tailored ancillary services. These initiatives necessitate sophisticated backend ticketing systems that can support complex bundling and personalization algorithms. Furthermore, the continuous technological advancements in areas such as artificial intelligence (AI), machine learning (ML), and blockchain for features like fraud detection, predictive analytics, and secure payment processing are enhancing the capabilities and attractiveness of modern ticketing systems. However, the market faces constraints such as high initial investment and ongoing maintenance costs, particularly for smaller carriers or those integrating with fragmented legacy systems. Data security and privacy concerns, especially with the proliferation of personal data, also represent a significant challenge, driving demand for robust Cybersecurity Market solutions within these platforms.

Competitive Ecosystem of Airline Ticketing System Market

The Airline Ticketing System Market is characterized by a concentrated yet innovative competitive landscape, featuring established global distribution system (GDS) providers and specialized software vendors. These entities compete on the basis of technological sophistication, global reach, integration capabilities, and the breadth of services offered.

Amadeus IT Group: A global leader in travel technology, Amadeus provides comprehensive IT solutions for airlines, including passenger service systems (PSS), inventory management, and distribution solutions, enabling airlines to manage operations and connect with travel sellers worldwide.

Sabre Corporation: A major technology provider for the travel industry, Sabre offers a broad portfolio of solutions spanning airline and hospitality operations, including its GDS platform, which facilitates global travel bookings and advanced ticketing functionalities.

Travelport: As a technology company and GDS provider, Travelport focuses on modernizing travel retailing through its next-generation platform, offering airlines robust distribution, shopping, and booking capabilities to enhance their market reach.

Navitaire: A wholly owned subsidiary of Amadeus, Navitaire specializes in technology solutions for low-cost and hybrid airlines, providing scalable reservation systems, ancillary revenue tools, and internet booking engines.

SITA: A leading IT provider for the air transport industry, SITA delivers a range of solutions, including passenger management, baggage handling, and airport operations, with ticketing and distribution capabilities integrated into its broader airline portfolio.

Hitit: An airline and travel industry software provider, Hitit offers an advanced passenger service system (PSS) called Crane, which includes reservation, ticketing, and departure control modules tailored for various airline business models.

Lufthansa Systems: A prominent airline IT service provider, Lufthansa Systems offers a comprehensive suite of solutions, including its own passenger service system (PSS) and innovative digital platforms for flight operations, scheduling, and distribution.

IBS Software: Specializing in SaaS solutions for the travel industry, IBS Software provides highly modular and integrated systems for airlines, including passenger services, loyalty programs, cargo operations, and flight management.

Radixx: Acquired by Sabre, Radixx provides an innovative passenger service system (PSS) tailored for hybrid, low-cost, and ultra-low-cost carriers, focusing on flexible merchandising and direct distribution capabilities.

TravelSky Technology: A state-owned enterprise in China, TravelSky provides comprehensive information technology and commercial services for the air travel and tourism industry, including airline PSS and global distribution systems within the Chinese market.

Others: This category includes emerging players and niche providers focusing on specific components or regions, contributing to the diversity and innovation within the Airline Ticketing System Market.

Recent Developments & Milestones in Airline Ticketing System Market

January 2024: Amadeus announced a strategic partnership with a major European airline to implement its next-generation passenger service system (PSS) to enhance digital retailing capabilities and streamline booking processes. This move underscores the continuous evolution of core ticketing infrastructure.

November 2023: Sabre Corporation launched an enhanced version of its intelligent retailing platform, incorporating advanced AI and machine learning algorithms to enable airlines to offer more personalized offers and dynamic pricing across all booking channels, responding to demands for Data Analytics Market integration.

September 2023: Travelport finalized agreements with several airlines to adopt its New Distribution Capability (NDC) content, signifying a major shift towards more flexible and attribute-rich content distribution, impacting how ticketing systems interact with third-party aggregators.

June 2023: SITA introduced new Cloud Computing Market-based solutions for air travel, allowing airlines to deploy and scale ticketing and passenger processing services more flexibly and securely, directly addressing the industry's need for agile IT infrastructure.

April 2023: Navitaire collaborated with a rapidly growing low-cost carrier in Asia to deploy its state-of-the-art reservation and distribution system, enabling the airline to optimize ancillary revenue strategies and manage rapid expansion. This highlights the focus on the Airline Industry Market's specific segments.

February 2023: IBS Software expanded its partnership with a leading global airline to implement its next-gen loyalty platform, integrated directly with the ticketing system, to offer more seamless personalized rewards and incentives to passengers, further driving Digital Transformation Market initiatives.

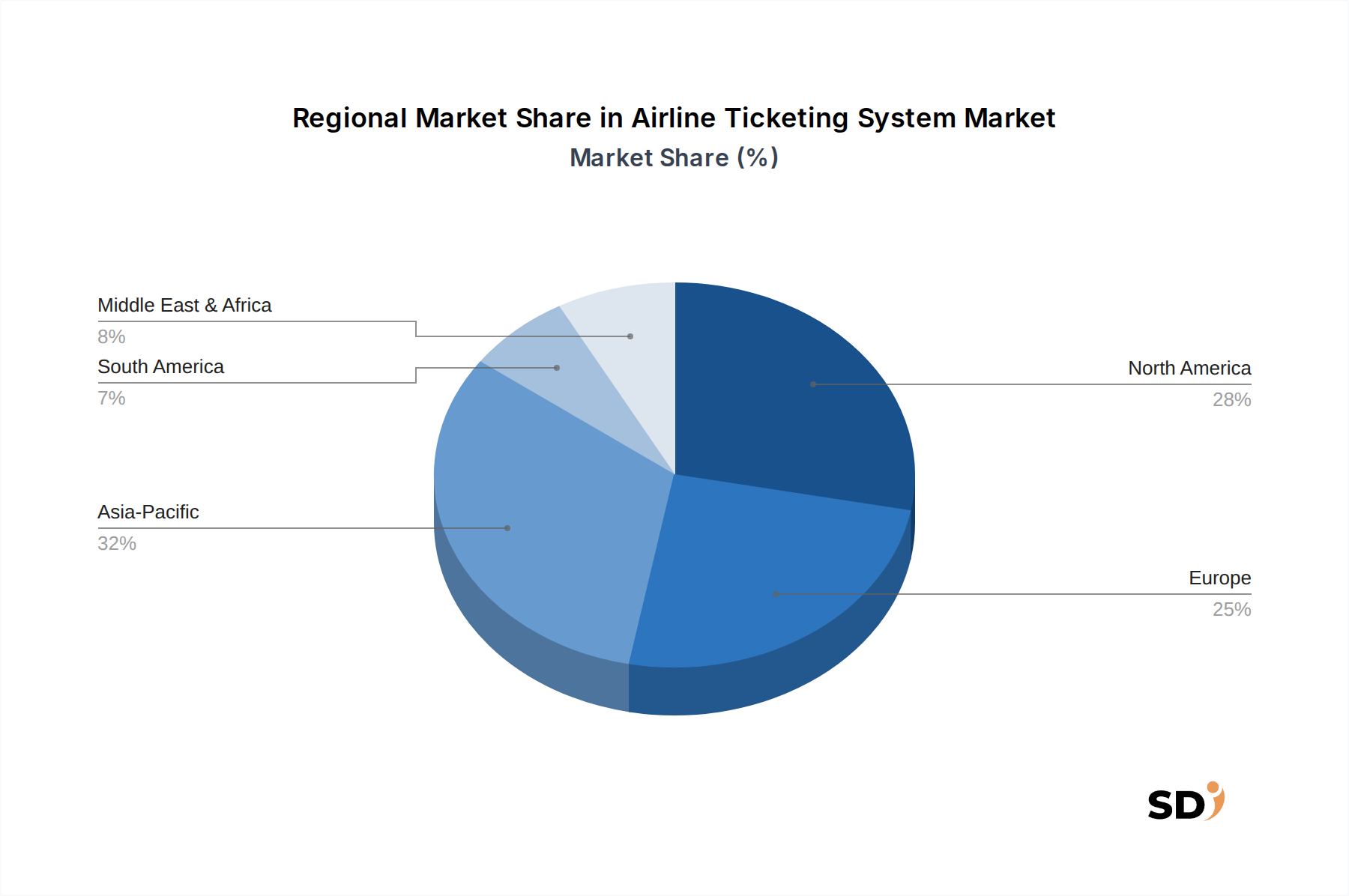

Regional Market Breakdown for Airline Ticketing System Market

Geographical analysis of the Airline Ticketing System Market reveals distinct growth patterns and demand drivers across key regions. While precise regional CAGRs are proprietary, industry trends indicate varying levels of maturity and adoption rates.

North America and Europe represent mature markets for airline ticketing systems. In these regions, the primary demand driver is the continuous upgrade and modernization of existing legacy systems, rather than the establishment of new ones. Airlines here are focused on enhancing customer experience, implementing advanced personalization, and leveraging Data Analytics Market for revenue optimization. The emphasis is on integrating NDC capabilities, cloud migration, and implementing robust Cybersecurity Market measures to protect sensitive passenger data. The presence of major airlines and a high volume of air travel necessitate sophisticated and resilient ticketing infrastructure, driving investments in advanced features and integration with broader IT Services Market offerings.

Asia Pacific is widely recognized as the fastest-growing region in the Airline Ticketing System Market. This growth is fueled by several factors, including the rapid expansion of the Airline Industry Market through new routes and carriers, a burgeoning middle class, and increasing disposable incomes leading to higher air travel demand. Countries like China and India are at the forefront, witnessing substantial investments in airport infrastructure and airline fleets. The region also shows strong adoption of Mobile Applications Market for booking and managing travel, pushing airlines to prioritize mobile-first ticketing solutions. This region's growth is often driven by the implementation of entirely new systems for emerging airlines and significant expansion projects for existing carriers.

Middle East & Africa shows significant potential for growth, primarily driven by the expansion of regional airlines, government initiatives promoting tourism, and the development of new aviation hubs. Investment in state-of-the-art ticketing systems is crucial for these airlines to compete on a global scale and to manage the increasing influx of international travelers. The focus here is on scalable solutions that can support rapid growth and cater to diverse international traveler needs.

South America demonstrates steady growth, influenced by improving economic conditions and increased intra-regional and international air connectivity. Airlines are investing in modern ticketing systems to improve operational efficiency and enhance customer service, aligning with global trends in Digital Transformation Market.

Pricing Dynamics & Margin Pressure in Airline Ticketing System Market

The pricing dynamics within the Airline Ticketing System Market are complex, driven by various factors including the scope of services, deployment model, level of customization, and the scale of airline operations. Predominantly, pricing models include transaction-based fees, subscription fees (especially for Cloud Computing Market SaaS solutions), or a hybrid approach. Transaction-based models, often employed by GDS providers, charge a fee per booking segment, which can exert significant margin pressure on airlines, particularly low-cost carriers (LCCs) who prioritize cost efficiency. Subscription models, favored by independent software vendors, offer more predictable costs and are gaining traction as airlines seek to move away from variable transaction fees.

Margin structures across the value chain differ. Software developers and integrators typically command higher margins due to intellectual property and specialized IT Services Market expertise. However, intense competition and the demand for constant innovation put pressure on these margins. For airlines, the cost of ticketing systems represents a substantial operational expenditure, impacting their overall profitability. Key cost levers for airlines include negotiating favorable terms with GDS providers, adopting NDC standards to enable direct distribution and reduce third-party fees, and migrating to cloud-based solutions to lower infrastructure and maintenance costs. The rise of LCCs has particularly intensified margin pressure, as these carriers prioritize lean operations and seek cost-effective solutions, pushing vendors to offer more competitive pricing. The increasing commoditization of basic ticketing functionalities, coupled with the high switching costs associated with changing core passenger service systems, creates a nuanced environment where premium pricing for advanced features (e.g., AI-powered personalization, complex Data Analytics Market) coexists with significant pressure on foundational service costs. This dynamic fosters a continuous cycle of innovation balanced against cost optimization imperatives.

Export, Trade Flow & Tariff Impact on Airline Ticketing System Market

The Airline Ticketing System Market, primarily driven by software and IT Services Market, is less susceptible to traditional tariffs on physical goods but is significantly impacted by regulations governing data flow, intellectual property, and cross-border service trade. Major trade corridors for these services often align with global aviation hubs and regions with advanced IT infrastructure. Leading exporting nations for airline ticketing system technologies are typically those with strong software development capabilities and established GDS providers, primarily North America and Europe. These regions export sophisticated software solutions, maintenance services, and technical expertise to airlines and travel agencies globally.

Importing nations include rapidly expanding Airline Industry Market regions such as Asia Pacific, the Middle East, and parts of Latin America, where local IT infrastructure or specialized software development may be less mature. These regions import advanced systems to support their growing air travel demand and Digital Transformation Market initiatives. The primary non-tariff barriers impacting this market are data localization laws and data privacy regulations, such as GDPR in Europe or similar enactments in other countries. These regulations often mandate that certain passenger data must be stored and processed within national borders, complicating global cloud deployments and requiring vendors to establish local data centers or secure robust data transfer agreements. Geopolitical tensions can also disrupt the trade flow of software services and support. For example, sanctions or restrictions on technology transfers can limit access to critical updates or support for certain markets. Furthermore, intellectual property rights and licensing agreements form a significant part of the cross-border "trade" in this market, with disputes or changes in these frameworks directly influencing market access and operational costs. While direct tariffs are minimal, the complex web of data governance, cybersecurity standards (which ties into the Cybersecurity Market), and licensing agreements effectively serve as modern trade barriers, shaping the strategies of key players and the flow of advanced ticketing system technologies globally.

Airline Ticketing System Segmentation

1. Component

1.1. Software

1.2. Hardware

1.3. Services

2. Deployment Mode

2.1. Cloud-based

2.2. On-premises

2.3. Hybrid

3. Platform

3.1. Desktop-Based Systems

3.2. Mobile-Based Systems

3.3. Web-Based Systems

4. End User

4.1. Commercial Airlines

4.2. Low-Cost Carriers (LCCs)

4.3. Charter Airlines

4.4. Cargo Airlines

4.5. Travel Agencies

4.6. Others

5. Booking Channel

5.1. Online Booking

5.2. Offline Booking

Airline Ticketing System Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Airline Ticketing System REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 9.9% from 2020-2034

Segmentation

By Component

Software

Hardware

Services

By Deployment Mode

Cloud-based

On-premises

Hybrid

By Platform

Desktop-Based Systems

Mobile-Based Systems

Web-Based Systems

By End User

Commercial Airlines

Low-Cost Carriers (LCCs)

Charter Airlines

Cargo Airlines

Travel Agencies

Others

By Booking Channel

Online Booking

Offline Booking

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Component

5.1.1. Software

5.1.2. Hardware

5.1.3. Services

5.2. Market Analysis, Insights and Forecast - by Deployment Mode

5.2.1. Cloud-based

5.2.2. On-premises

5.2.3. Hybrid

5.3. Market Analysis, Insights and Forecast - by Platform

5.3.1. Desktop-Based Systems

5.3.2. Mobile-Based Systems

5.3.3. Web-Based Systems

5.4. Market Analysis, Insights and Forecast - by End User

5.4.1. Commercial Airlines

5.4.2. Low-Cost Carriers (LCCs)

5.4.3. Charter Airlines

5.4.4. Cargo Airlines

5.4.5. Travel Agencies

5.4.6. Others

5.5. Market Analysis, Insights and Forecast - by Booking Channel

5.5.1. Online Booking

5.5.2. Offline Booking

5.6. Market Analysis, Insights and Forecast - by Region

5.6.1. North America

5.6.2. South America

5.6.3. Europe

5.6.4. Middle East & Africa

5.6.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Component

6.1.1. Software

6.1.2. Hardware

6.1.3. Services

6.2. Market Analysis, Insights and Forecast - by Deployment Mode

6.2.1. Cloud-based

6.2.2. On-premises

6.2.3. Hybrid

6.3. Market Analysis, Insights and Forecast - by Platform

6.3.1. Desktop-Based Systems

6.3.2. Mobile-Based Systems

6.3.3. Web-Based Systems

6.4. Market Analysis, Insights and Forecast - by End User

6.4.1. Commercial Airlines

6.4.2. Low-Cost Carriers (LCCs)

6.4.3. Charter Airlines

6.4.4. Cargo Airlines

6.4.5. Travel Agencies

6.4.6. Others

6.5. Market Analysis, Insights and Forecast - by Booking Channel

6.5.1. Online Booking

6.5.2. Offline Booking

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Component

7.1.1. Software

7.1.2. Hardware

7.1.3. Services

7.2. Market Analysis, Insights and Forecast - by Deployment Mode

7.2.1. Cloud-based

7.2.2. On-premises

7.2.3. Hybrid

7.3. Market Analysis, Insights and Forecast - by Platform

7.3.1. Desktop-Based Systems

7.3.2. Mobile-Based Systems

7.3.3. Web-Based Systems

7.4. Market Analysis, Insights and Forecast - by End User

7.4.1. Commercial Airlines

7.4.2. Low-Cost Carriers (LCCs)

7.4.3. Charter Airlines

7.4.4. Cargo Airlines

7.4.5. Travel Agencies

7.4.6. Others

7.5. Market Analysis, Insights and Forecast - by Booking Channel

7.5.1. Online Booking

7.5.2. Offline Booking

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Component

8.1.1. Software

8.1.2. Hardware

8.1.3. Services

8.2. Market Analysis, Insights and Forecast - by Deployment Mode

8.2.1. Cloud-based

8.2.2. On-premises

8.2.3. Hybrid

8.3. Market Analysis, Insights and Forecast - by Platform

8.3.1. Desktop-Based Systems

8.3.2. Mobile-Based Systems

8.3.3. Web-Based Systems

8.4. Market Analysis, Insights and Forecast - by End User

8.4.1. Commercial Airlines

8.4.2. Low-Cost Carriers (LCCs)

8.4.3. Charter Airlines

8.4.4. Cargo Airlines

8.4.5. Travel Agencies

8.4.6. Others

8.5. Market Analysis, Insights and Forecast - by Booking Channel

8.5.1. Online Booking

8.5.2. Offline Booking

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Component

9.1.1. Software

9.1.2. Hardware

9.1.3. Services

9.2. Market Analysis, Insights and Forecast - by Deployment Mode

9.2.1. Cloud-based

9.2.2. On-premises

9.2.3. Hybrid

9.3. Market Analysis, Insights and Forecast - by Platform

9.3.1. Desktop-Based Systems

9.3.2. Mobile-Based Systems

9.3.3. Web-Based Systems

9.4. Market Analysis, Insights and Forecast - by End User

9.4.1. Commercial Airlines

9.4.2. Low-Cost Carriers (LCCs)

9.4.3. Charter Airlines

9.4.4. Cargo Airlines

9.4.5. Travel Agencies

9.4.6. Others

9.5. Market Analysis, Insights and Forecast - by Booking Channel

9.5.1. Online Booking

9.5.2. Offline Booking

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Component

10.1.1. Software

10.1.2. Hardware

10.1.3. Services

10.2. Market Analysis, Insights and Forecast - by Deployment Mode

10.2.1. Cloud-based

10.2.2. On-premises

10.2.3. Hybrid

10.3. Market Analysis, Insights and Forecast - by Platform

10.3.1. Desktop-Based Systems

10.3.2. Mobile-Based Systems

10.3.3. Web-Based Systems

10.4. Market Analysis, Insights and Forecast - by End User

10.4.1. Commercial Airlines

10.4.2. Low-Cost Carriers (LCCs)

10.4.3. Charter Airlines

10.4.4. Cargo Airlines

10.4.5. Travel Agencies

10.4.6. Others

10.5. Market Analysis, Insights and Forecast - by Booking Channel

10.5.1. Online Booking

10.5.2. Offline Booking

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Amadeus IT Group

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Sabre Corporation

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Travelport

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Navitaire

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. SITA

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Hitit

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Lufthansa Systems

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. IBS Software

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Radixx

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. TravelSky Technology

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Others

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Component 2025 & 2033

Figure 3: Revenue Share (%), by Component 2025 & 2033

Figure 4: Revenue (million), by Deployment Mode 2025 & 2033

Figure 60: Revenue (million), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Component 2020 & 2033

Table 2: Revenue million Forecast, by Deployment Mode 2020 & 2033

Table 3: Revenue million Forecast, by Platform 2020 & 2033

Table 4: Revenue million Forecast, by End User 2020 & 2033

Table 5: Revenue million Forecast, by Booking Channel 2020 & 2033

Table 6: Revenue million Forecast, by Region 2020 & 2033

Table 7: Revenue million Forecast, by Component 2020 & 2033

Table 8: Revenue million Forecast, by Deployment Mode 2020 & 2033

Table 9: Revenue million Forecast, by Platform 2020 & 2033

Table 10: Revenue million Forecast, by End User 2020 & 2033

Table 11: Revenue million Forecast, by Booking Channel 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Component 2020 & 2033

Table 17: Revenue million Forecast, by Deployment Mode 2020 & 2033

Table 18: Revenue million Forecast, by Platform 2020 & 2033

Table 19: Revenue million Forecast, by End User 2020 & 2033

Table 20: Revenue million Forecast, by Booking Channel 2020 & 2033

Table 21: Revenue million Forecast, by Country 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue million Forecast, by Component 2020 & 2033

Table 26: Revenue million Forecast, by Deployment Mode 2020 & 2033

Table 27: Revenue million Forecast, by Platform 2020 & 2033

Table 28: Revenue million Forecast, by End User 2020 & 2033

Table 29: Revenue million Forecast, by Booking Channel 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue (million) Forecast, by Application 2020 & 2033

Table 38: Revenue (million) Forecast, by Application 2020 & 2033

Table 39: Revenue (million) Forecast, by Application 2020 & 2033

Table 40: Revenue million Forecast, by Component 2020 & 2033

Table 41: Revenue million Forecast, by Deployment Mode 2020 & 2033

Table 42: Revenue million Forecast, by Platform 2020 & 2033

Table 43: Revenue million Forecast, by End User 2020 & 2033

Table 44: Revenue million Forecast, by Booking Channel 2020 & 2033

Table 45: Revenue million Forecast, by Country 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue (million) Forecast, by Application 2020 & 2033

Table 48: Revenue (million) Forecast, by Application 2020 & 2033

Table 49: Revenue (million) Forecast, by Application 2020 & 2033

Table 50: Revenue (million) Forecast, by Application 2020 & 2033

Table 51: Revenue (million) Forecast, by Application 2020 & 2033

Table 52: Revenue million Forecast, by Component 2020 & 2033

Table 53: Revenue million Forecast, by Deployment Mode 2020 & 2033

Table 54: Revenue million Forecast, by Platform 2020 & 2033

Table 55: Revenue million Forecast, by End User 2020 & 2033

Table 56: Revenue million Forecast, by Booking Channel 2020 & 2033

Table 57: Revenue million Forecast, by Country 2020 & 2033

Table 58: Revenue (million) Forecast, by Application 2020 & 2033

Table 59: Revenue (million) Forecast, by Application 2020 & 2033

Table 60: Revenue (million) Forecast, by Application 2020 & 2033

Table 61: Revenue (million) Forecast, by Application 2020 & 2033

Table 62: Revenue (million) Forecast, by Application 2020 & 2033

Table 63: Revenue (million) Forecast, by Application 2020 & 2033

Table 64: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our analysis relies significantly on primary research, constituting approximately 75% of the total research effort. This robust approach involves extensive, in-depth interviews with key stakeholders across the value chain of the airline ticketing system market. These interviews are designed to gather qualitative and quantitative insights, validate secondary findings, and identify emerging trends and challenges directly from industry experts.

Key participant types for primary interviews include:

Global Distribution Systems (GDS) Providers: Insights into market share, technology roadmaps, and partnerships.

Airline IT Solution Providers: Direct information on product development, competitive landscape, and client acquisition strategies.

Airline Revenue Management Software Developers: Expertise on integration challenges, pricing strategies, and system evolution.

Travel Technology Integrators & Consultants: Perspectives on implementation complexities, customization requirements, and end-user adoption.

Major Airline Groups (Commercial, LCCs, Cargo): Direct feedback on system performance, pain points, purchasing decisions, and future investment plans.

Stakeholders targeted for interviews typically include senior decision-makers such as:

CIO/CTO of Major Airlines/LCCs: Offering strategic insights into technology adoption and infrastructure planning.

Head of Digital Transformation/Innovation (Airlines/OTAs): Providing perspectives on digital strategy and system modernization.

Senior Product Manager/Director (Ticketing Systems Vendors): Sharing granular details on product features, market positioning, and customer feedback.

VP/Director of Revenue Management & Pricing (Airlines): Offering insights into system requirements from a yield optimization and dynamic pricing standpoint.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

CIO/CTO of Major Airlines/LCCs

30%

Head of Digital Transformation (Airlines/OTAs)

25%

Senior Product Manager (Ticketing Systems Vendors)

25%

VP/Director of Revenue Management & Pricing (Airlines)

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Airline IT Solution Providers

30%

Global Distribution Systems (GDS) Providers

25%

Major Airline Groups (End-users)

20%

Airline Revenue Management Software Developers

15%

Travel Technology Integrators

10%

Secondary Research & Industry Benchmarking

Secondary research forms the remaining approximately 25% of our methodology, providing foundational data, market context, and historical trends. This phase involves a rigorous review of diverse, credible sources to ensure comprehensive coverage and accuracy.

Our secondary research extensively utilizes:

Financial Databases: Platforms such as Bloomberg, Factiva, Hoovers, and PitchBook are leveraged to gather company financials, investment activities, and competitive intelligence.

Government Publications (.Gov): Official statistics, economic reports, and regulatory frameworks impacting the aviation and travel sectors.

Industry Associations & Regulatory Bodies (.Org): Reports, whitepapers, and statistical data from recognized organizations. We specifically draw insights from:

International Air Transport Association (IATA) [Relevant Industry Report Source]

Airlines for America (A4A) [Relevant Association Data Source]

International Civil Aviation Organization (ICAO) [Relevant Regulatory Document Source]

Association of Asia Pacific Airlines (AAPA) [Relevant Regional Study Source]

Company Annual Reports and Investor Presentations: Detailed financial performance, strategic outlooks, and operational data of key market players.

Trade Journals and Publications: Specialised articles and analyses providing current industry developments and expert opinions.

Crucially, our secondary research meticulously avoids data sourced from other market research websites to maintain originality and prevent data duplication, ensuring independent validation.

Demand Modeling & Market Estimation

Our market sizing and forecasting approach employs a dual methodology: top-down and bottom-up, complemented by multi-level data triangulation to ensure robust estimates.

Top-Down Approach: We begin by estimating the overall market size based on macroeconomic factors, global aviation industry growth rates, and total IT spending within the airline sector. This aggregate figure is then systematically disaggregated by component, deployment mode, platform, end-user, booking channel, and geography.

Bottom-Up Approach: This method involves estimating market size by building up from granular data points. Key metrics and variables used in our bottom-up calculations include:

Number of active commercial aircraft in global fleets: Serving as a proxy for the installed base and potential for system upgrades/new deployments.

Annual passenger traffic volume (RPKs/PAX): Directly correlated with transaction volumes and the demand for efficient ticketing systems.

Average IT expenditure allocated to Passenger Service Systems (PSS) and ticketing solutions per airline: Providing a direct measure of spending capacity.

Deployment rates of next-generation ticketing and reservation systems: Indicating market penetration and growth opportunities across different airline segments.

Multi-Level Data Triangulation: The findings from both top-down and bottom-up analyses are rigorously cross-validated with insights from primary interviews and secondary sources. This iterative process allows for the reconciliation of discrepancies, identification of outliers, and refinement of market figures, leading to highly dependable estimates.

Data Accuracy & Quality Check

Maintaining the highest standards of data accuracy and reliability is paramount. Our research methodology is engineered to deliver an estimated data accuracy level of 88%.

Every data point, market figure, and forecast is subjected to a stringent multi-stage validation process:

Internal Validation: Our team of experienced analysts reviews all compiled data, ensuring consistency, logical coherence, and adherence to defined parameters.

Expert Review: Insights and findings are cross-checked with industry experts interviewed during the primary research phase, seeking their validation and feedback on market assumptions and projections.

Scenario Analysis: Various market scenarios (optimistic, conservative, realistic) are modeled to understand the sensitivity of our forecasts to different variables, enhancing the robustness of the predictions.

Furthermore, to provide the most current market intelligence, every report is updated up to the date of purchase, ensuring clients receive the latest available data and market perspectives.

Frequently Asked Questions

1. What are the key segments within the Airline Ticketing System market?

Key segments include Component (Software, Hardware, Services), Deployment Mode (Cloud-based, On-premises), End User (Commercial Airlines, Travel Agencies), and Booking Channel (Online Booking). Software components and cloud-based deployments are significant contributors to the market's $5225 million valuation in 2024.

2. Which region exhibits the fastest growth opportunities for Airline Ticketing Systems?

Asia-Pacific is projected to exhibit robust growth, driven by increasing air travel demand, infrastructure development, and digitalization efforts in countries like China and India. The market is forecasted to grow at a CAGR of 9.9% through 2034, with this region being a primary accelerator.

3. How have post-pandemic patterns influenced the Airline Ticketing System market?

The post-pandemic recovery has accelerated the adoption of cloud-based systems and online booking channels, emphasizing operational flexibility and efficiency. Airlines and travel agencies prioritize digital transformation to manage fluctuating demand and enhance customer experience, supporting the market's 9.9% CAGR.

4. Why is North America a dominant region in the Airline Ticketing System market?

North America remains a dominant region due to its mature aviation industry, high volume of air traffic, and early adoption of advanced ticketing technologies. The presence of major players like Sabre Corporation and strong digital infrastructure contribute significantly to its market share.

5. What recent developments are shaping the Airline Ticketing System market?

Recent developments focus on enhancing system integration, incorporating AI for personalized booking experiences, and expanding mobile-based ticketing solutions. Key companies such as Amadeus IT Group and Travelport continuously update platforms to meet evolving airline and traveler demands.

6. What disruptive technologies could impact the Airline Ticketing System market?

Disruptive technologies include blockchain for secure and transparent ticketing, potentially reducing fraud and intermediation costs. Additionally, enhanced direct-to-consumer platforms by airlines pose an emerging alternative to traditional Global Distribution Systems (GDS) offerings, influencing market dynamics.