Airline Ancillary Services by Service Type (Baggage Fees, Onboard Retail & A La Carte Services, Seat & Comfort Services, Airline Retail & Travel Add-ons, Others), by Carrier Type (Full-Service Carriers (FSC), Low-Cost Carriers (LCC), Hybrid Airlines), by Flight Type (Domestic Flights, International Flights), by Cabin Class (Economy Class, Premium Economy, Business Class, First Class), by Distribution Channel (Direct Channel, Indirect Channel), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 94

Srinwanti Kar

Senior Research Analyst

About Sector Data Insights

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Key Insights into the Airline Ancillary Services Market

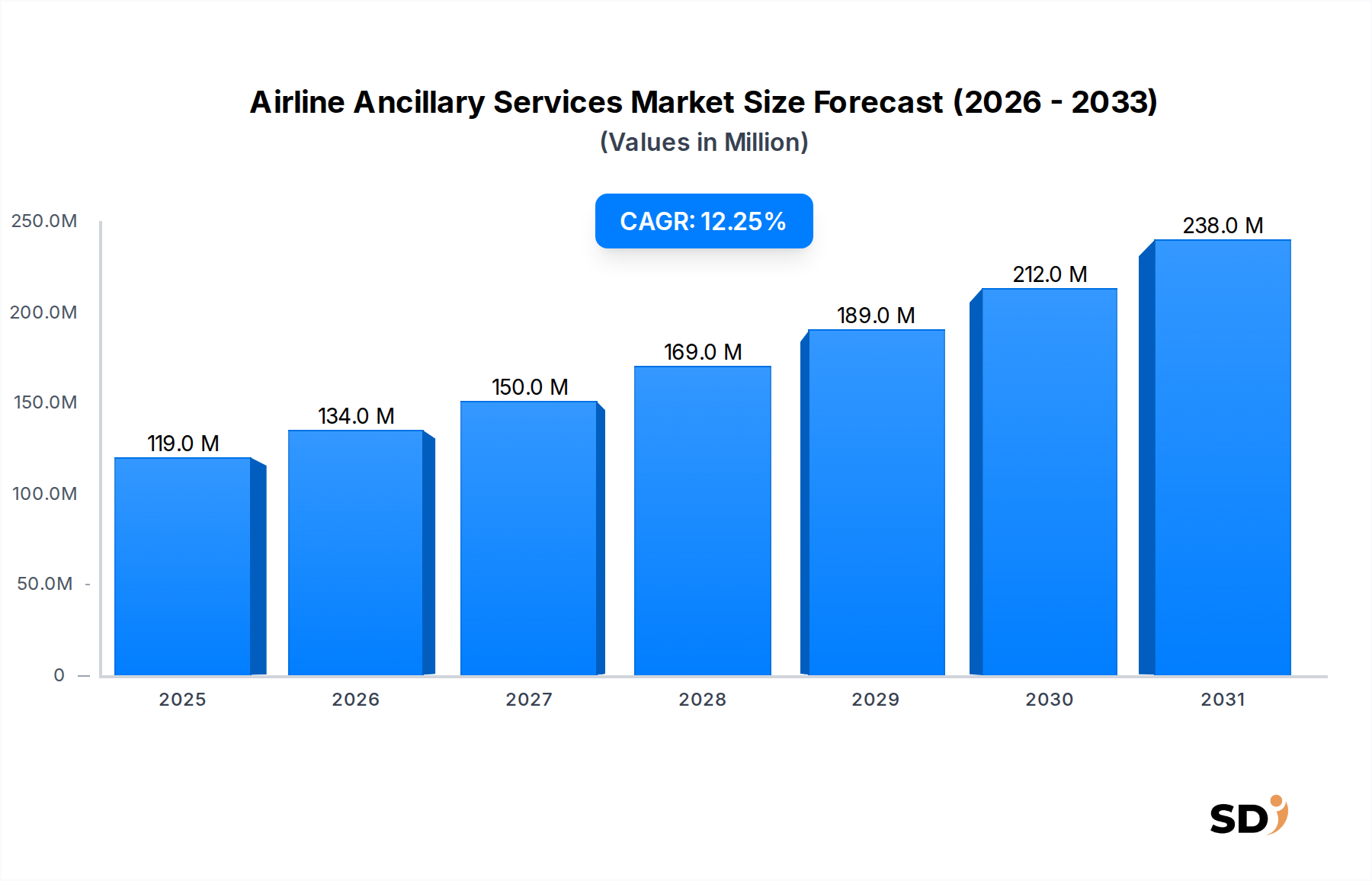

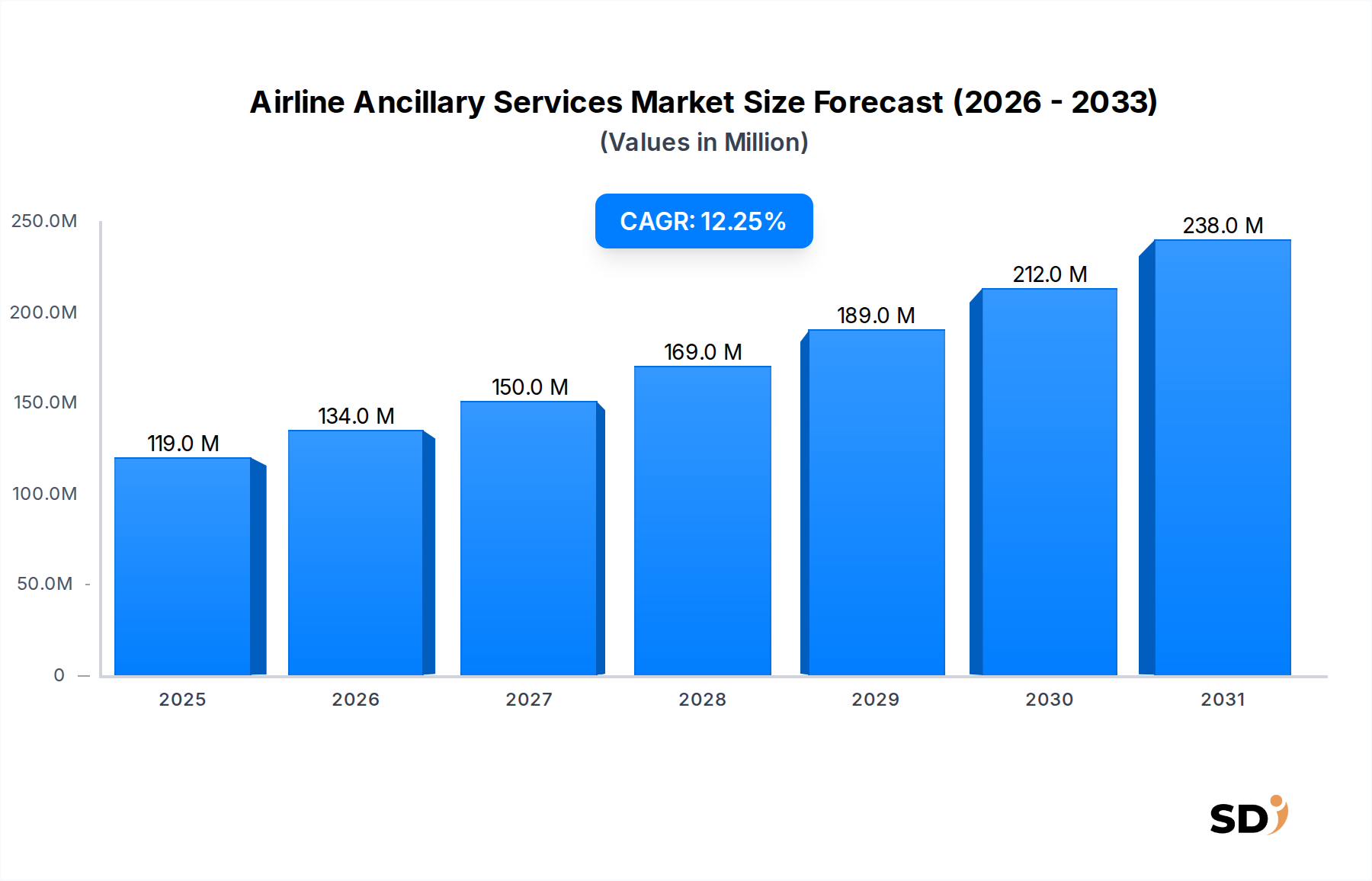

The Airline Ancillary Services Market is a critical and rapidly expanding segment within the broader aviation industry, driven by evolving airline business models and passenger demand for personalized travel experiences. Valued at $119.19 million in 2024, this market is projected to reach approximately $377.29 million by 2034, demonstrating a robust Compound Annual Growth Rate (CAGR) of 12.24% over the forecast period. This significant growth underscores airlines' strategic imperative to diversify revenue streams beyond traditional ticket sales, enhancing profitability and resilience in a highly competitive Aviation Services Market.

Airline Ancillary Services Market Size (In Million)

250.0M

200.0M

150.0M

100.0M

50.0M

0

119.0 M

2025

134.0 M

2026

150.0 M

2027

169.0 M

2028

189.0 M

2029

212.0 M

2030

238.0 M

2031

Key demand drivers propelling the Airline Ancillary Services Market include the aggressive expansion of low-cost carriers (LCCs) globally, whose fundamental strategy relies on unbundling services and monetizing additional offerings. Furthermore, a growing consumer preference for customized travel experiences, allowing passengers to pay only for the services they require, is fostering increased adoption of ancillary options. Technological advancements, particularly in the realm of Digital Travel Platform Market solutions and mobile applications, are simplifying the booking and management of these services, making them more accessible and attractive to travelers. The integration of advanced analytics, often supported by Data Analytics Software Market technologies, enables airlines to optimize pricing strategies and personalize offers, significantly boosting conversion rates for services ranging from seat selection to in-flight meals and Travel Insurance Market options. Macro tailwinds such as increasing global air travel demand, rising disposable incomes in emerging economies, and the continuous innovation in service offerings contribute to the market's upward trajectory. The forward-looking outlook indicates a continued emphasis on innovation in ancillary product development, deeper personalization through AI and machine learning, and strategic partnerships to offer a comprehensive travel ecosystem, further solidifying the market's robust growth.

Baggage Fees in Airline Ancillary Services Market

Within the multifaceted Airline Ancillary Services Market, the 'Baggage Fees' sub-segment consistently stands out as a dominant revenue generator, playing a pivotal role in the financial strategies of carriers worldwide. This segment encompasses a range of charges, including checked baggage fees, carry-on baggage fees, and excess/overweight baggage fees. Its dominance stems from several key factors: universality of application, high transaction volume, and its integral role in the low-cost carrier business model. For many passengers, carrying baggage is a non-negotiable aspect of air travel, making baggage fees a primary and highly predictable ancillary revenue stream. Low-cost carriers, in particular, pioneered the unbundling of baggage services from the base fare, allowing them to offer highly competitive ticket prices while significantly boosting their ancillary revenue per passenger.

The widespread adoption of baggage fees across both full-service carriers (FSCs) and LCCs has cemented its leading position. While FSCs initially resisted, many have gradually introduced or expanded baggage charges, especially for economy class and domestic routes, to align with industry trends and enhance profitability. The strategic importance of baggage fees is further amplified by dynamic pricing models, where charges can vary based on route, booking time, cabin class, and loyalty status, maximizing revenue capture. Although some passenger pushback exists, the market has largely adapted to this structure, viewing it as a standard component of air travel pricing. The ongoing growth in global air travel volumes directly translates to a proportional increase in baggage fee revenue. As carriers continue to seek diversified revenue streams, the 'Service Type' segment, particularly through its 'Baggage Fees' component, remains a cornerstone of the Airline Ancillary Services Market. Innovations in this area, such as bundled services that include baggage or subscription models, aim to enhance customer value while maintaining robust revenue generation, often facilitated by robust Payment Processing Software Market solutions for seamless transactions.

Digital Transformation & Personalization as Key Drivers in Airline Ancillary Services Market

One of the most significant drivers propelling the Airline Ancillary Services Market is the profound impact of digital transformation coupled with advanced personalization strategies. This driver is directly quantifiable by the rapid adoption of sophisticated Digital Travel Platform Market solutions and advanced Data Analytics Software Market across the industry. Airlines are investing heavily in these technologies to understand passenger behavior, preferences, and purchasing patterns with unprecedented granularity. For instance, the deployment of AI-powered recommendation engines on airline websites and mobile applications has been shown to increase conversion rates for ancillary purchases by an average of 10-15% in early adopter airlines, moving beyond simple static offers to dynamic, context-aware suggestions. This shift allows airlines to present highly relevant offers, such as preferred seating upgrades for frequent flyers or Car Rental Services Market bundles for destination-specific travelers, directly at the point of booking or during the journey.

Conversely, a notable constraint impacting the Airline Ancillary Services Market is the increasing regulatory scrutiny surrounding pricing transparency. Regions like Europe and North America have introduced regulations, such as the EU's "all-in" pricing rules, which mandate that the advertised price for a flight must include all non-optional charges, including certain taxes and fees. This regulatory environment restricts airlines' ability to obscure additional costs, requiring greater clarity in presenting ancillary options and their associated charges. While these regulations aim to protect consumers from hidden fees, they can limit the flexibility of airlines in dynamic pricing strategies and potentially lead to a perception of higher initial base fares, impacting booking psychology. Airlines must navigate this complex landscape by ensuring compliance while still innovating in their ancillary offerings. Furthermore, the intense competition within the broader Aviation Services Market can also act as a constraint. When base fares are aggressively low due to fierce competition, airlines become even more reliant on ancillary revenue, but simultaneously face pressure not to price ancillary services so high as to deter passengers, creating a delicate balance that requires continuous optimization and consumer perception management.

Competitive Ecosystem of Airline Ancillary Services Market

The Airline Ancillary Services Market features a diverse competitive landscape, primarily comprising major global and regional carriers, each implementing distinct strategies to maximize ancillary revenue. The competition extends beyond direct ticket sales to a comprehensive offering of supplementary services, often leveraging technology for personalization and distribution.

American Airlines Group: A major full-service carrier, American Airlines Group focuses on a hybrid approach, offering premium ancillary services while also diversifying its revenue streams through baggage fees, preferred seating, and loyalty program enhancements. Its strategy emphasizes personalization through its extensive customer data.

Delta Air Lines: Delta Air Lines employs a sophisticated ancillary strategy, particularly through its loyalty program (SkyMiles), premium cabin upgrades, and partnerships for ground services. The airline prioritizes customer experience, using ancillary services to enhance travel comfort and convenience.

United Airlines Holdings: United Airlines Holdings focuses on expanding its ancillary portfolio through dynamic pricing for seat selection, baggage, and In-flight Entertainment Market options. The airline actively leverages its MileagePlus program to drive engagement and ancillary purchases, often through targeted promotions.

Ryanair DAC: As a pioneering low-cost carrier, Ryanair DAC's business model is heavily reliant on ancillary revenues, which include a wide array of charges from baggage and priority boarding to Car Rental Services Market and hotel bookings. Their aggressive pricing strategy for base fares is directly offset by high ancillary capture.

Southwest Airlines: Known for its unique "bags fly free" policy, Southwest Airlines differentiates itself by minimizing certain traditional ancillary fees. Instead, it focuses on rapid turnarounds, higher load factors, and complementary services, while still generating revenue through upgrades like EarlyBird Check-In.

Lufthansa Group: The Lufthansa Group, encompassing several European carriers, balances premium service with a growing emphasis on ancillary revenues. They offer a range of services from enhanced baggage options to extensive lounge access and tailored vacation packages, increasingly digitalizing their offerings.

Air France–KLM: Air France–KLM strategically bundles and unbundles services to cater to diverse customer segments. Their ancillary strategy includes seat options, extra baggage, and a strong focus on premium services, often integrated with their Flying Blue loyalty program for personalized offers.

EasyJet: Another leading low-cost carrier in Europe, EasyJet generates substantial ancillary revenue through baggage fees, assigned seating, and food and beverage sales. The airline continually refines its ancillary offerings to complement its affordable base fares, supported by robust Payment Processing Software Market infrastructure.

AirAsia Group: Dominant in the ASEAN region, AirAsia Group is a prominent LCC with a strong focus on ancillary services, including extensive baggage options, meal pre-orders, and partnerships for hotels and Travel Insurance Market. Their digital platforms are key to driving these sales.

Qantas Airways: Qantas Airways, Australia's flagship carrier, offers a mix of full-service and low-cost (Jetstar) ancillary strategies. Qantas itself focuses on premium upgrades, lounge access, and loyalty program benefits, while Jetstar heavily relies on a broader range of unbundled services.

Recent Developments & Milestones in Airline Ancillary Services Market

May 2023: Several airlines intensified their focus on "unbundling" previously included services, leading to a broader array of fee-based options for amenities such as advanced seat selection, extra legroom, and enhanced In-flight Entertainment Market packages across domestic and international routes.

August 2023: There was a notable increase in strategic partnerships between airlines and third-party travel providers, including hotel chains and Car Rental Services Market operators, to offer comprehensive travel packages and generate referral commissions. This expanded the scope of ancillary offerings beyond airline-specific services.

November 2023: Airlines began investing more significantly in upgrading their Digital Travel Platform Market infrastructure and mobile applications. These enhancements aimed to provide a more seamless and intuitive purchasing experience for ancillary services, from booking to post-purchase management, often integrating more sophisticated Payment Processing Software Market solutions.

February 2024: The adoption of AI and machine learning algorithms became more widespread for personalized ancillary recommendations. Airlines leveraged Data Analytics Software Market capabilities to analyze passenger history and preferences, offering tailored upgrades, meal options, or Travel Insurance Market policies at optimal moments.

April 2024: New subscription and membership models emerged, allowing frequent travelers to pay a recurring fee for unlimited access to certain ancillary benefits like free baggage, preferred seating, or lounge access, signaling a shift towards loyalty-driven ancillary strategies.

July 2024: Increased efforts in sustainable ancillary offerings, such as carbon offset programs, eco-friendly in-flight products, and partnerships with sustainable tourism providers, began to gain traction, reflecting growing passenger demand for environmentally conscious travel choices.

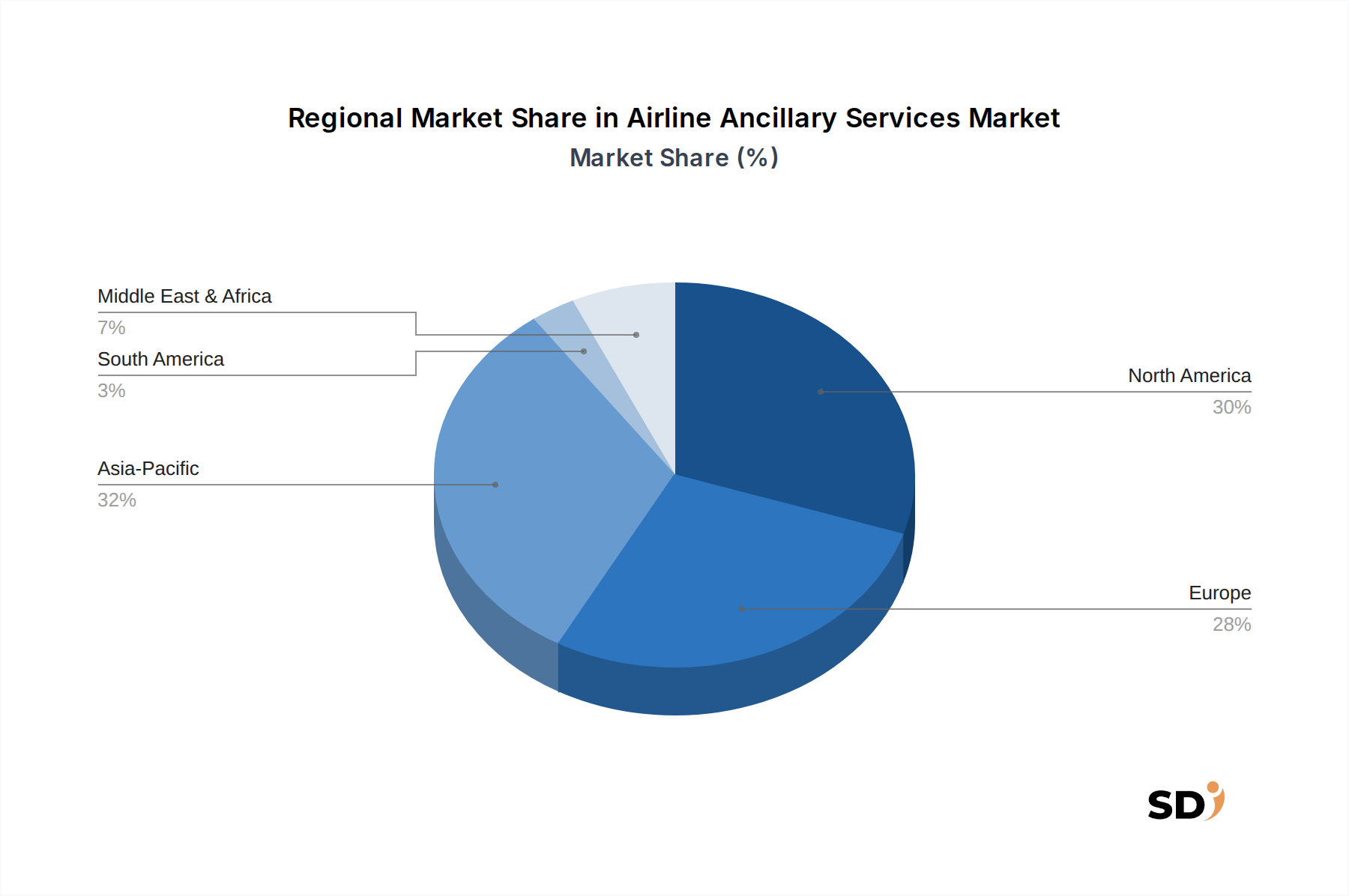

Regional Market Breakdown for Airline Ancillary Services Market

The Airline Ancillary Services Market exhibits distinct dynamics across various global regions, driven by differing regulatory landscapes, consumer behaviors, and the prevalence of specific carrier types. The global CAGR of 12.24% is an aggregate of these regional variations.

North America continues to hold the largest revenue share in the Airline Ancillary Services Market. This dominance is attributed to a mature aviation sector, high domestic air travel volumes, and the early adoption and widespread implementation of ancillary revenue strategies by both full-service and low-cost carriers. While a mature market, North America maintains steady growth driven by continuous innovation in service bundling and personalization, often leveraging robust Cloud Computing Services Market infrastructure for operational efficiency. The primary demand driver here is the established consumer acceptance of paying for unbundled services and a highly competitive carrier environment.

Europe represents another significant market for airline ancillary services, characterized by a high penetration of low-cost carriers like Ryanair and EasyJet, which have historically pioneered aggressive ancillary strategies. The region benefits from dense short-haul networks and a culture of budget travel. While growth is steady, it is influenced by stringent consumer protection regulations that mandate transparency in pricing, requiring airlines to adapt their communication strategies. The demand driver is rooted in cost-conscious travelers and the extensive inter-country connectivity.

Asia Pacific is recognized as the fastest-growing region in the Airline Ancillary Services Market. This rapid expansion is fueled by an burgeoning middle class, increasing disposable incomes, and the proliferation of new low-cost carriers in countries like India, China, and across ASEAN. The region also sees significant investment in enhancing the In-flight Entertainment Market and other premium ancillary offerings to cater to a diverse and growing passenger base. The primary demand driver is the surging air travel demand and expanding routes, coupled with a growing appetite for convenient and value-added services.

Middle East & Africa is an emerging market demonstrating strong growth potential. The region benefits from significant investments in aviation infrastructure, rising tourism, and increasing business connectivity. While starting from a smaller base, airlines in this region are rapidly adopting ancillary revenue strategies, particularly focusing on premium services and tailored offerings for both leisure and transit passengers. The primary demand driver is the region's strategic geographical location, serving as a hub for international travel, alongside government initiatives promoting tourism and economic diversification.

Supply Chain & Raw Material Dynamics for Airline Ancillary Services Market

For the Airline Ancillary Services Market, the concept of "raw materials" extends beyond physical goods to encompass digital infrastructure, intellectual property, and strategic partnerships that enable the delivery and monetization of supplementary services. Upstream dependencies are primarily concentrated on technology providers, content creators, and third-party service aggregators. Key inputs include advanced Digital Travel Platform Market solutions, sophisticated Payment Processing Software Market for seamless transactions, and robust Cloud Computing Services Market infrastructure for data storage and processing.

Sourcing risks involve vendor lock-in with core IT systems providers, cybersecurity vulnerabilities affecting customer data, and the reliability of third-party partners for services like Car Rental Services Market or hotel bookings. Price volatility is less about commodity raw materials and more about software licensing fees, transaction processing costs, and commission rates from partner agreements. For instance, the cost of data storage and processing via Cloud Computing Services Market can fluctuate based on usage and provider contracts. Similarly, the terms of content licensing for In-flight Entertainment Market (movies, music, games) can experience price adjustments based on exclusivity and demand. Disruptions can arise from system outages impacting online booking platforms, data breaches eroding customer trust, or shifts in partnership agreements that affect the availability or pricing of bundled Travel Insurance Market or ground transfer options. The market's heavy reliance on Data Analytics Software Market for optimizing pricing and offers means that the consistent performance and cost-effectiveness of these digital tools are crucial for maintaining revenue growth and competitive edge.

The Airline Ancillary Services Market operates within a complex and evolving regulatory and policy landscape across key geographies, designed primarily to protect consumers, ensure transparency, and foster fair competition. Major regulatory frameworks significantly impact how airlines can market, price, and sell ancillary services. In the European Union, regulations such as the EU Consumer Rights Directive and various sector-specific rules emphasize "all-in" pricing transparency. This means that airlines must prominently display the total price, including all non-optional fees and charges, from the outset of the booking process, impacting how fees for baggage or seat selection are presented. Recent policy changes have also focused on discouraging misleading marketing practices regarding "free" services that later incur charges, directly influencing how ancillary products are advertised. The United States has seen similar pushes from the Department of Transportation (DOT) for greater transparency, particularly regarding baggage fees and cancellation policies. Proposed rules often aim to ensure passengers are fully aware of all costs upfront, potentially leading to more standardized disclosure of ancillary charges across various booking channels.

Beyond pricing, data privacy regulations, such as the EU's General Data Protection Regulation (GDPR) and similar frameworks in other regions, significantly impact how airlines collect, process, and utilize passenger data for personalized ancillary offers. Compliance with these stringent privacy laws dictates the scope of personalized marketing for services like Travel Insurance Market or premium upgrades, requiring explicit consent and secure data handling. Competition authorities globally also scrutinize ancillary pricing practices to prevent anti-competitive behavior or abuse of dominant market positions, particularly in specific route monopolies. Future policy changes are likely to focus on further standardization of ancillary service definitions, greater interoperability of booking systems to enhance transparency across indirect channels, and potentially caps or stricter oversight on certain "surprise" fees. These regulations necessitate that airlines continuously adapt their operational and commercial strategies, often requiring upgrades to their Digital Travel Platform Market to ensure compliance while striving for continued growth in the Airline Ancillary Services Market.

Airline Ancillary Services Segmentation

1. Service Type

1.1. Baggage Fees

1.1.1. Checked Baggage Fees

1.1.2. Carry-on Baggage Fees

1.1.3. Excess / Overweight Baggage Fees

1.2. Onboard Retail & A La Carte Services

1.2.1. Food & Beverage Sales

1.2.2. Duty-Free Sales

1.2.3. In-flight Entertainment

1.2.4. Comfort Kits & Travel Accessories

1.3. Seat & Comfort Services

1.3.1. Seat Selection Fees

1.3.2. Extra Legroom Seats

1.3.3. Preferred / Premium Seating

1.3.4. Cabin Upgrades

1.4. Airline Retail & Travel Add-ons

1.4.1. Hotel Bookings

1.4.2. Car Rentals

1.4.3. Travel Insurance

1.4.4. Airport Transfers

1.4.5. Vacation Packages

1.5. Others

2. Carrier Type

2.1. Full-Service Carriers (FSC)

2.2. Low-Cost Carriers (LCC)

2.3. Hybrid Airlines

3. Flight Type

3.1. Domestic Flights

3.2. International Flights

4. Cabin Class

4.1. Economy Class

4.2. Premium Economy

4.3. Business Class

4.4. First Class

5. Distribution Channel

5.1. Direct Channel

5.1.1. Airline Websites

5.1.2. Mobile Applications

5.1.3. Airport Counters / Kiosks

5.2. Indirect Channel

5.2.1. Online Travel Agencies (OTAs)

5.2.2. Travel Agents

5.2.3. Global Distribution Systems (GDS)

Airline Ancillary Services Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Airline Ancillary Services REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 12.24% from 2020-2034

Segmentation

By Service Type

Baggage Fees

Checked Baggage Fees

Carry-on Baggage Fees

Excess / Overweight Baggage Fees

Onboard Retail & A La Carte Services

Food & Beverage Sales

Duty-Free Sales

In-flight Entertainment

Comfort Kits & Travel Accessories

Seat & Comfort Services

Seat Selection Fees

Extra Legroom Seats

Preferred / Premium Seating

Cabin Upgrades

Airline Retail & Travel Add-ons

Hotel Bookings

Car Rentals

Travel Insurance

Airport Transfers

Vacation Packages

Others

By Carrier Type

Full-Service Carriers (FSC)

Low-Cost Carriers (LCC)

Hybrid Airlines

By Flight Type

Domestic Flights

International Flights

By Cabin Class

Economy Class

Premium Economy

Business Class

First Class

By Distribution Channel

Direct Channel

Airline Websites

Mobile Applications

Airport Counters / Kiosks

Indirect Channel

Online Travel Agencies (OTAs)

Travel Agents

Global Distribution Systems (GDS)

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Service Type

5.1.1. Baggage Fees

5.1.1.1. Checked Baggage Fees

5.1.1.2. Carry-on Baggage Fees

5.1.1.3. Excess / Overweight Baggage Fees

5.1.2. Onboard Retail & A La Carte Services

5.1.2.1. Food & Beverage Sales

5.1.2.2. Duty-Free Sales

5.1.2.3. In-flight Entertainment

5.1.2.4. Comfort Kits & Travel Accessories

5.1.3. Seat & Comfort Services

5.1.3.1. Seat Selection Fees

5.1.3.2. Extra Legroom Seats

5.1.3.3. Preferred / Premium Seating

5.1.3.4. Cabin Upgrades

5.1.4. Airline Retail & Travel Add-ons

5.1.4.1. Hotel Bookings

5.1.4.2. Car Rentals

5.1.4.3. Travel Insurance

5.1.4.4. Airport Transfers

5.1.4.5. Vacation Packages

5.1.5. Others

5.2. Market Analysis, Insights and Forecast - by Carrier Type

5.2.1. Full-Service Carriers (FSC)

5.2.2. Low-Cost Carriers (LCC)

5.2.3. Hybrid Airlines

5.3. Market Analysis, Insights and Forecast - by Flight Type

5.3.1. Domestic Flights

5.3.2. International Flights

5.4. Market Analysis, Insights and Forecast - by Cabin Class

5.4.1. Economy Class

5.4.2. Premium Economy

5.4.3. Business Class

5.4.4. First Class

5.5. Market Analysis, Insights and Forecast - by Distribution Channel

5.5.1. Direct Channel

5.5.1.1. Airline Websites

5.5.1.2. Mobile Applications

5.5.1.3. Airport Counters / Kiosks

5.5.2. Indirect Channel

5.5.2.1. Online Travel Agencies (OTAs)

5.5.2.2. Travel Agents

5.5.2.3. Global Distribution Systems (GDS)

5.6. Market Analysis, Insights and Forecast - by Region

5.6.1. North America

5.6.2. South America

5.6.3. Europe

5.6.4. Middle East & Africa

5.6.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Service Type

6.1.1. Baggage Fees

6.1.1.1. Checked Baggage Fees

6.1.1.2. Carry-on Baggage Fees

6.1.1.3. Excess / Overweight Baggage Fees

6.1.2. Onboard Retail & A La Carte Services

6.1.2.1. Food & Beverage Sales

6.1.2.2. Duty-Free Sales

6.1.2.3. In-flight Entertainment

6.1.2.4. Comfort Kits & Travel Accessories

6.1.3. Seat & Comfort Services

6.1.3.1. Seat Selection Fees

6.1.3.2. Extra Legroom Seats

6.1.3.3. Preferred / Premium Seating

6.1.3.4. Cabin Upgrades

6.1.4. Airline Retail & Travel Add-ons

6.1.4.1. Hotel Bookings

6.1.4.2. Car Rentals

6.1.4.3. Travel Insurance

6.1.4.4. Airport Transfers

6.1.4.5. Vacation Packages

6.1.5. Others

6.2. Market Analysis, Insights and Forecast - by Carrier Type

6.2.1. Full-Service Carriers (FSC)

6.2.2. Low-Cost Carriers (LCC)

6.2.3. Hybrid Airlines

6.3. Market Analysis, Insights and Forecast - by Flight Type

6.3.1. Domestic Flights

6.3.2. International Flights

6.4. Market Analysis, Insights and Forecast - by Cabin Class

6.4.1. Economy Class

6.4.2. Premium Economy

6.4.3. Business Class

6.4.4. First Class

6.5. Market Analysis, Insights and Forecast - by Distribution Channel

6.5.1. Direct Channel

6.5.1.1. Airline Websites

6.5.1.2. Mobile Applications

6.5.1.3. Airport Counters / Kiosks

6.5.2. Indirect Channel

6.5.2.1. Online Travel Agencies (OTAs)

6.5.2.2. Travel Agents

6.5.2.3. Global Distribution Systems (GDS)

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Service Type

7.1.1. Baggage Fees

7.1.1.1. Checked Baggage Fees

7.1.1.2. Carry-on Baggage Fees

7.1.1.3. Excess / Overweight Baggage Fees

7.1.2. Onboard Retail & A La Carte Services

7.1.2.1. Food & Beverage Sales

7.1.2.2. Duty-Free Sales

7.1.2.3. In-flight Entertainment

7.1.2.4. Comfort Kits & Travel Accessories

7.1.3. Seat & Comfort Services

7.1.3.1. Seat Selection Fees

7.1.3.2. Extra Legroom Seats

7.1.3.3. Preferred / Premium Seating

7.1.3.4. Cabin Upgrades

7.1.4. Airline Retail & Travel Add-ons

7.1.4.1. Hotel Bookings

7.1.4.2. Car Rentals

7.1.4.3. Travel Insurance

7.1.4.4. Airport Transfers

7.1.4.5. Vacation Packages

7.1.5. Others

7.2. Market Analysis, Insights and Forecast - by Carrier Type

7.2.1. Full-Service Carriers (FSC)

7.2.2. Low-Cost Carriers (LCC)

7.2.3. Hybrid Airlines

7.3. Market Analysis, Insights and Forecast - by Flight Type

7.3.1. Domestic Flights

7.3.2. International Flights

7.4. Market Analysis, Insights and Forecast - by Cabin Class

7.4.1. Economy Class

7.4.2. Premium Economy

7.4.3. Business Class

7.4.4. First Class

7.5. Market Analysis, Insights and Forecast - by Distribution Channel

7.5.1. Direct Channel

7.5.1.1. Airline Websites

7.5.1.2. Mobile Applications

7.5.1.3. Airport Counters / Kiosks

7.5.2. Indirect Channel

7.5.2.1. Online Travel Agencies (OTAs)

7.5.2.2. Travel Agents

7.5.2.3. Global Distribution Systems (GDS)

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Service Type

8.1.1. Baggage Fees

8.1.1.1. Checked Baggage Fees

8.1.1.2. Carry-on Baggage Fees

8.1.1.3. Excess / Overweight Baggage Fees

8.1.2. Onboard Retail & A La Carte Services

8.1.2.1. Food & Beverage Sales

8.1.2.2. Duty-Free Sales

8.1.2.3. In-flight Entertainment

8.1.2.4. Comfort Kits & Travel Accessories

8.1.3. Seat & Comfort Services

8.1.3.1. Seat Selection Fees

8.1.3.2. Extra Legroom Seats

8.1.3.3. Preferred / Premium Seating

8.1.3.4. Cabin Upgrades

8.1.4. Airline Retail & Travel Add-ons

8.1.4.1. Hotel Bookings

8.1.4.2. Car Rentals

8.1.4.3. Travel Insurance

8.1.4.4. Airport Transfers

8.1.4.5. Vacation Packages

8.1.5. Others

8.2. Market Analysis, Insights and Forecast - by Carrier Type

8.2.1. Full-Service Carriers (FSC)

8.2.2. Low-Cost Carriers (LCC)

8.2.3. Hybrid Airlines

8.3. Market Analysis, Insights and Forecast - by Flight Type

8.3.1. Domestic Flights

8.3.2. International Flights

8.4. Market Analysis, Insights and Forecast - by Cabin Class

8.4.1. Economy Class

8.4.2. Premium Economy

8.4.3. Business Class

8.4.4. First Class

8.5. Market Analysis, Insights and Forecast - by Distribution Channel

8.5.1. Direct Channel

8.5.1.1. Airline Websites

8.5.1.2. Mobile Applications

8.5.1.3. Airport Counters / Kiosks

8.5.2. Indirect Channel

8.5.2.1. Online Travel Agencies (OTAs)

8.5.2.2. Travel Agents

8.5.2.3. Global Distribution Systems (GDS)

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Service Type

9.1.1. Baggage Fees

9.1.1.1. Checked Baggage Fees

9.1.1.2. Carry-on Baggage Fees

9.1.1.3. Excess / Overweight Baggage Fees

9.1.2. Onboard Retail & A La Carte Services

9.1.2.1. Food & Beverage Sales

9.1.2.2. Duty-Free Sales

9.1.2.3. In-flight Entertainment

9.1.2.4. Comfort Kits & Travel Accessories

9.1.3. Seat & Comfort Services

9.1.3.1. Seat Selection Fees

9.1.3.2. Extra Legroom Seats

9.1.3.3. Preferred / Premium Seating

9.1.3.4. Cabin Upgrades

9.1.4. Airline Retail & Travel Add-ons

9.1.4.1. Hotel Bookings

9.1.4.2. Car Rentals

9.1.4.3. Travel Insurance

9.1.4.4. Airport Transfers

9.1.4.5. Vacation Packages

9.1.5. Others

9.2. Market Analysis, Insights and Forecast - by Carrier Type

9.2.1. Full-Service Carriers (FSC)

9.2.2. Low-Cost Carriers (LCC)

9.2.3. Hybrid Airlines

9.3. Market Analysis, Insights and Forecast - by Flight Type

9.3.1. Domestic Flights

9.3.2. International Flights

9.4. Market Analysis, Insights and Forecast - by Cabin Class

9.4.1. Economy Class

9.4.2. Premium Economy

9.4.3. Business Class

9.4.4. First Class

9.5. Market Analysis, Insights and Forecast - by Distribution Channel

9.5.1. Direct Channel

9.5.1.1. Airline Websites

9.5.1.2. Mobile Applications

9.5.1.3. Airport Counters / Kiosks

9.5.2. Indirect Channel

9.5.2.1. Online Travel Agencies (OTAs)

9.5.2.2. Travel Agents

9.5.2.3. Global Distribution Systems (GDS)

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Service Type

10.1.1. Baggage Fees

10.1.1.1. Checked Baggage Fees

10.1.1.2. Carry-on Baggage Fees

10.1.1.3. Excess / Overweight Baggage Fees

10.1.2. Onboard Retail & A La Carte Services

10.1.2.1. Food & Beverage Sales

10.1.2.2. Duty-Free Sales

10.1.2.3. In-flight Entertainment

10.1.2.4. Comfort Kits & Travel Accessories

10.1.3. Seat & Comfort Services

10.1.3.1. Seat Selection Fees

10.1.3.2. Extra Legroom Seats

10.1.3.3. Preferred / Premium Seating

10.1.3.4. Cabin Upgrades

10.1.4. Airline Retail & Travel Add-ons

10.1.4.1. Hotel Bookings

10.1.4.2. Car Rentals

10.1.4.3. Travel Insurance

10.1.4.4. Airport Transfers

10.1.4.5. Vacation Packages

10.1.5. Others

10.2. Market Analysis, Insights and Forecast - by Carrier Type

10.2.1. Full-Service Carriers (FSC)

10.2.2. Low-Cost Carriers (LCC)

10.2.3. Hybrid Airlines

10.3. Market Analysis, Insights and Forecast - by Flight Type

10.3.1. Domestic Flights

10.3.2. International Flights

10.4. Market Analysis, Insights and Forecast - by Cabin Class

10.4.1. Economy Class

10.4.2. Premium Economy

10.4.3. Business Class

10.4.4. First Class

10.5. Market Analysis, Insights and Forecast - by Distribution Channel

10.5.1. Direct Channel

10.5.1.1. Airline Websites

10.5.1.2. Mobile Applications

10.5.1.3. Airport Counters / Kiosks

10.5.2. Indirect Channel

10.5.2.1. Online Travel Agencies (OTAs)

10.5.2.2. Travel Agents

10.5.2.3. Global Distribution Systems (GDS)

11. Competitive Analysis

11.1. Company Profiles

11.1.1. American Airlines Group

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Delta Air Lines

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. United Airlines Holdings

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Ryanair DAC

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Southwest Airlines

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Lufthansa Group

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Air France–KLM

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. EasyJet

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. AirAsia Group

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Qantas Airways

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Others

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Service Type 2025 & 2033

Figure 3: Revenue Share (%), by Service Type 2025 & 2033

Figure 4: Revenue (million), by Carrier Type 2025 & 2033

Figure 5: Revenue Share (%), by Carrier Type 2025 & 2033

Figure 6: Revenue (million), by Flight Type 2025 & 2033

Figure 7: Revenue Share (%), by Flight Type 2025 & 2033

Figure 8: Revenue (million), by Cabin Class 2025 & 2033

Figure 9: Revenue Share (%), by Cabin Class 2025 & 2033

Figure 10: Revenue (million), by Distribution Channel 2025 & 2033

Figure 11: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Service Type 2025 & 2033

Figure 15: Revenue Share (%), by Service Type 2025 & 2033

Figure 16: Revenue (million), by Carrier Type 2025 & 2033

Figure 17: Revenue Share (%), by Carrier Type 2025 & 2033

Figure 18: Revenue (million), by Flight Type 2025 & 2033

Figure 19: Revenue Share (%), by Flight Type 2025 & 2033

Figure 20: Revenue (million), by Cabin Class 2025 & 2033

Figure 21: Revenue Share (%), by Cabin Class 2025 & 2033

Figure 22: Revenue (million), by Distribution Channel 2025 & 2033

Figure 23: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Service Type 2025 & 2033

Figure 27: Revenue Share (%), by Service Type 2025 & 2033

Figure 28: Revenue (million), by Carrier Type 2025 & 2033

Figure 29: Revenue Share (%), by Carrier Type 2025 & 2033

Figure 30: Revenue (million), by Flight Type 2025 & 2033

Figure 31: Revenue Share (%), by Flight Type 2025 & 2033

Figure 32: Revenue (million), by Cabin Class 2025 & 2033

Figure 33: Revenue Share (%), by Cabin Class 2025 & 2033

Figure 34: Revenue (million), by Distribution Channel 2025 & 2033

Figure 35: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 36: Revenue (million), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Revenue (million), by Service Type 2025 & 2033

Figure 39: Revenue Share (%), by Service Type 2025 & 2033

Figure 40: Revenue (million), by Carrier Type 2025 & 2033

Figure 41: Revenue Share (%), by Carrier Type 2025 & 2033

Figure 42: Revenue (million), by Flight Type 2025 & 2033

Figure 43: Revenue Share (%), by Flight Type 2025 & 2033

Figure 44: Revenue (million), by Cabin Class 2025 & 2033

Figure 45: Revenue Share (%), by Cabin Class 2025 & 2033

Figure 46: Revenue (million), by Distribution Channel 2025 & 2033

Figure 47: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 48: Revenue (million), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Revenue (million), by Service Type 2025 & 2033

Figure 51: Revenue Share (%), by Service Type 2025 & 2033

Figure 52: Revenue (million), by Carrier Type 2025 & 2033

Figure 53: Revenue Share (%), by Carrier Type 2025 & 2033

Figure 54: Revenue (million), by Flight Type 2025 & 2033

Figure 55: Revenue Share (%), by Flight Type 2025 & 2033

Figure 56: Revenue (million), by Cabin Class 2025 & 2033

Figure 57: Revenue Share (%), by Cabin Class 2025 & 2033

Figure 58: Revenue (million), by Distribution Channel 2025 & 2033

Figure 59: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 60: Revenue (million), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Service Type 2020 & 2033

Table 2: Revenue million Forecast, by Carrier Type 2020 & 2033

Table 3: Revenue million Forecast, by Flight Type 2020 & 2033

Table 4: Revenue million Forecast, by Cabin Class 2020 & 2033

Table 5: Revenue million Forecast, by Distribution Channel 2020 & 2033

Table 6: Revenue million Forecast, by Region 2020 & 2033

Table 7: Revenue million Forecast, by Service Type 2020 & 2033

Table 8: Revenue million Forecast, by Carrier Type 2020 & 2033

Table 9: Revenue million Forecast, by Flight Type 2020 & 2033

Table 10: Revenue million Forecast, by Cabin Class 2020 & 2033

Table 11: Revenue million Forecast, by Distribution Channel 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Service Type 2020 & 2033

Table 17: Revenue million Forecast, by Carrier Type 2020 & 2033

Table 18: Revenue million Forecast, by Flight Type 2020 & 2033

Table 19: Revenue million Forecast, by Cabin Class 2020 & 2033

Table 20: Revenue million Forecast, by Distribution Channel 2020 & 2033

Table 21: Revenue million Forecast, by Country 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue million Forecast, by Service Type 2020 & 2033

Table 26: Revenue million Forecast, by Carrier Type 2020 & 2033

Table 27: Revenue million Forecast, by Flight Type 2020 & 2033

Table 28: Revenue million Forecast, by Cabin Class 2020 & 2033

Table 29: Revenue million Forecast, by Distribution Channel 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue (million) Forecast, by Application 2020 & 2033

Table 38: Revenue (million) Forecast, by Application 2020 & 2033

Table 39: Revenue (million) Forecast, by Application 2020 & 2033

Table 40: Revenue million Forecast, by Service Type 2020 & 2033

Table 41: Revenue million Forecast, by Carrier Type 2020 & 2033

Table 42: Revenue million Forecast, by Flight Type 2020 & 2033

Table 43: Revenue million Forecast, by Cabin Class 2020 & 2033

Table 44: Revenue million Forecast, by Distribution Channel 2020 & 2033

Table 45: Revenue million Forecast, by Country 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue (million) Forecast, by Application 2020 & 2033

Table 48: Revenue (million) Forecast, by Application 2020 & 2033

Table 49: Revenue (million) Forecast, by Application 2020 & 2033

Table 50: Revenue (million) Forecast, by Application 2020 & 2033

Table 51: Revenue (million) Forecast, by Application 2020 & 2033

Table 52: Revenue million Forecast, by Service Type 2020 & 2033

Table 53: Revenue million Forecast, by Carrier Type 2020 & 2033

Table 54: Revenue million Forecast, by Flight Type 2020 & 2033

Table 55: Revenue million Forecast, by Cabin Class 2020 & 2033

Table 56: Revenue million Forecast, by Distribution Channel 2020 & 2033

Table 57: Revenue million Forecast, by Country 2020 & 2033

Table 58: Revenue (million) Forecast, by Application 2020 & 2033

Table 59: Revenue (million) Forecast, by Application 2020 & 2033

Table 60: Revenue (million) Forecast, by Application 2020 & 2033

Table 61: Revenue (million) Forecast, by Application 2020 & 2033

Table 62: Revenue (million) Forecast, by Application 2020 & 2033

Table 63: Revenue (million) Forecast, by Application 2020 & 2033

Table 64: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

The market research methodology employed for the "Airline Ancillary Services" report is meticulously designed to deliver highly accurate, actionable, and comprehensive market insights. Our robust approach synthesizes an extensive blend of primary and secondary research, ensuring a holistic understanding of market dynamics, competitive landscapes, and future growth trajectories.

Global Distribution Systems (GDS) & Online Travel Agencies (OTAs)

15%

Payment Processing & Loyalty Program Providers

10%

Primary Research

Our primary research constitutes the bedrock of this report, accounting for 70-80% of the total research effort. This extensive phase involves in-depth, semi-structured interviews with a diverse array of industry stakeholders across the value chain. The objective is to gather firsthand qualitative and quantitative data, validate secondary findings, and identify nascent trends and market nuances. Our interviewees are strategically selected to provide multi-faceted perspectives, encompassing various geographic regions and business models within the airline and ancillary services ecosystem.

Key stakeholders engaged in our primary research include:

VP/Director, Ancillary Revenue

Head of Digital & E-commerce

VP/Director, Commercial Strategy

Product Manager, Ancillary Services

The primary research participants are drawn from a range of company types critical to the airline ancillary services market, ensuring comprehensive representation:

Global Distribution Systems (GDS) & Online Travel Agencies (OTAs)

Payment Processing & Loyalty Program Providers

Secondary Research & Industry Benchmarking

The remaining 20-30% of our research is dedicated to rigorous secondary research and industry benchmarking. This phase provides foundational data, industry trends, and validates information gathered during primary interviews. Our analysts meticulously scour reputable and authoritative sources, prioritizing data integrity and relevance.

Sources utilized include:

Standard Financial Databases: Bloomberg, Factiva, Hoovers, PitchBook.

Government & Organizational Publications: Official reports, whitepapers, and statistical data from relevant governmental bodies and intergovernmental organizations such as the International Civil Aviation Organization (ICAO) [www.icao.int], national aviation authorities (e.g., FAA [www.faa.gov], EASA [www.easa.europa.eu]), and departments of transportation.

Trade Associations & Industry Bodies: Publications, annual reports, press releases, and statistical yearbooks from global and regional aviation industry associations, including the International Air Transport Association (IATA) [www.iata.org] and the Airline Passenger Experience Association (APEX) [www.apex.aero].

Company Annual Reports & Investor Presentations: Publicly available financial statements, annual reports, and investor calls from key market players.

Academic Research & White Papers: Peer-reviewed journals and authoritative studies providing deeper insights into specific market segments or technological advancements.

Crucially, our secondary research explicitly avoids data from other market research websites to maintain the independence and originality of our findings. Every report is updated up to the date of purchase, ensuring the most current market information is reflected.

Demand Modeling & Market Estimation

Our market estimation framework integrates both top-down and bottom-up approaches, triangulated to ensure maximum accuracy and robustness.

Bottom-Up Approach: This method involves segmenting the market based on granular data points and aggregating them to arrive at the total market size.

Key metrics and variables used for bottom-up calculation include:

Average Ancillary Revenue Per Passenger (by carrier type, flight type, region)

Total Number of Passengers Carried (segmented by carrier type, flight type, region, cabin class)

Average Ancillary Spend per Flight Segment by Service Type (e.g., baggage, seat selection, onboard retail)

Growth Rate of Air Travel (passenger traffic and capacity expansion)

Top-Down Approach: This approach starts with the overall addressable market (e.g., global airline revenue, total passenger spend) and progressively narrows it down by applying relevant market share, penetration rates, and ancillary revenue percentages derived from primary and secondary research.

Multi-level Data Triangulation: Data points derived from primary interviews, secondary sources, and both top-down and bottom-up models are cross-referenced and validated. Discrepancies are rigorously investigated and reconciled through further research and expert consultation, ensuring a coherent and reliable market picture.

Data Accuracy & Quality Check

We guarantee an estimated data accuracy level of 85-90%. This high standard is maintained through a multi-tiered quality assurance process:

Expert Validation: Insights and projections are validated by seasoned industry experts and primary interviewees.

Statistical Analysis: Robust statistical models are applied to analyze trends, forecast growth, and identify outliers.

Internal Peer Review: All data, models, and conclusions undergo rigorous review by an independent team of senior analysts to eliminate biases and ensure methodological consistency.

Regular Updates: As a standard practice, our market intelligence is continuously refreshed, and every report delivered is updated to reflect the most current market conditions up to the date of purchase, guaranteeing timely and relevant insights.

Frequently Asked Questions

1. How has the Airline Ancillary Services market evolved post-pandemic?

Post-pandemic, the Airline Ancillary Services market has seen significant growth driven by airlines seeking new revenue streams and passengers valuing personalized experiences. This recovery has accelerated adoption of premium seating and flexible booking options across carriers.

2. What is the projected size and growth rate for Airline Ancillary Services?

The global Airline Ancillary Services market is valued at $119.19 million in 2024. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.24% through 2034, reflecting sustained demand for enhanced travel options.

3. Which are the primary service segments within Airline Ancillary Services?

Key service segments include Baggage Fees, Onboard Retail & A La Carte Services, and Seat & Comfort Services. Additionally, Airline Retail & Travel Add-ons like hotel bookings and car rentals contribute significantly to market revenue.

4. How do regulations impact the Airline Ancillary Services market?

Regulatory bodies influence ancillary services through consumer protection laws and transparency requirements, particularly concerning fee disclosures for checked baggage and seat selection. Compliance varies by region, affecting pricing and service offerings for airlines such as Lufthansa Group.

5. What are the competitive barriers in the Airline Ancillary Services market?

Competitive barriers include established airline loyalty programs, the high operational costs of integrating new services, and strong brand recognition. Major players like American Airlines Group and Delta Air Lines benefit from extensive networks and existing customer bases.

6. How are consumer purchasing trends shaping Airline Ancillary Services?

Consumer purchasing trends show a preference for customization and convenience, driving demand for extra legroom, in-flight entertainment, and travel insurance. Mobile applications and airline websites are becoming preferred direct channels for these purchases, enhancing accessibility.