Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

AI Mobile Phone Chip Market: $206M, 29.3% CAGR Growth

AI Mobile Phone Chip

AI Mobile Phone Chip Market: $206M, 29.3% CAGR Growth

AI Mobile Phone Chip by Chip Type (Graphics Processing Units (GPUs), Tensor Processing Units (TPUs), Application-Specific Integrated Circuits (ASICs), Field-Programmable Gate Arrays (FPGAs), Neural Processing Unit (NPU), Others), by Fabrication Node (Below 5nm, 6nm–10nm, Above 10nm), by Price Range (Premium, Mid-Range, Budget), by Application (Mobile Photography Enhancement, Virtual Assistants, Real-Time Language Translation, Facial Recognition, AR/VR Applications, Mobile Gaming, Video Processing & Streaming, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 86

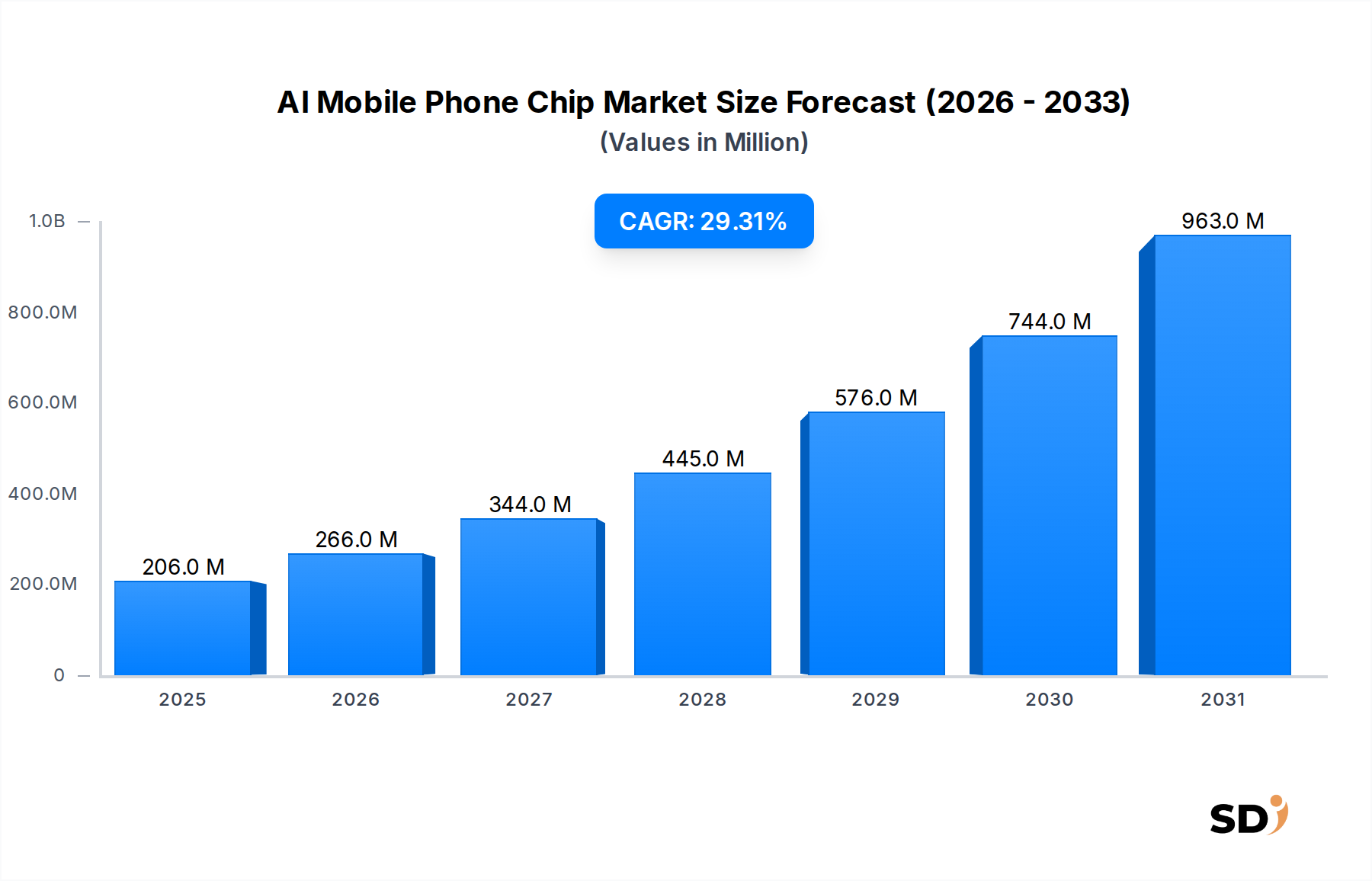

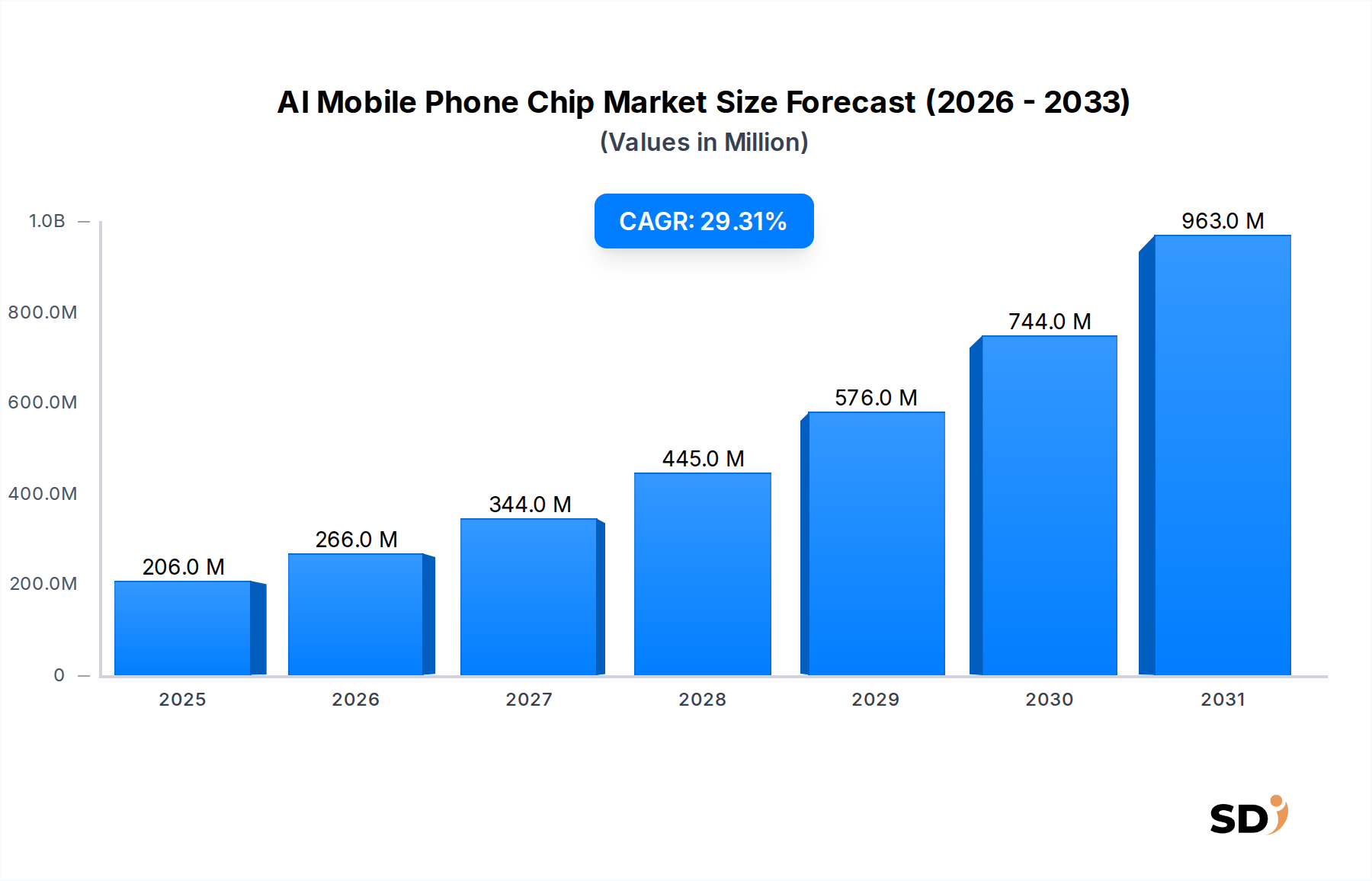

The global AI Mobile Phone Chip Market is currently valued at an impressive $206 million in 2025, poised for an exponential growth trajectory through the forecast period spanning 2026-2034. This robust expansion is underscored by a projected Compound Annual Growth Rate (CAGR) of 29.3%, propelling the market valuation to an estimated $2,266 million by 2034. The primary catalyst for this remarkable growth is the pervasive integration of Artificial Intelligence (AI) functionalities directly into mobile devices, shifting processing power from cloud-based servers to on-device hardware for enhanced privacy, speed, and efficiency.

AI Mobile Phone Chip Market Size (In Million)

1.0B

800.0M

600.0M

400.0M

200.0M

0

206.0 M

2025

266.0 M

2026

344.0 M

2027

445.0 M

2028

576.0 M

2029

744.0 M

2030

963.0 M

2031

Key demand drivers include the burgeoning proliferation of advanced mobile photography features, requiring sophisticated image signal processing and computational photography capabilities; the increasing demand for real-time language translation and virtual assistants that leverage localized AI models; and the rapid expansion of immersive Augmented Reality (AR) and Virtual Reality (VR) applications. Furthermore, the burgeoning Mobile Gaming Chipset Market is increasingly incorporating dedicated AI accelerators to optimize graphics, physics, and intelligent non-player character (NPC) behaviors, thereby enriching user experience. The strategic shift towards smaller fabrication nodes, particularly those below 5nm, is enabling the integration of more powerful yet energy-efficient AI engines within the compact form factor of smartphones. This technological advancement directly impacts the Smartphone Processor Market, where AI capabilities are now a fundamental differentiator.

The competitive landscape is characterized by intense innovation, with leading players continually pushing the boundaries of neural processing unit (NPU) architecture and software optimization. Geographically, the Asia Pacific region is expected to lead in both production and consumption, driven by high smartphone penetration rates and robust consumer electronics manufacturing ecosystems. The increasing consumer expectation for seamless, personalized, and intelligent mobile experiences ensures a sustained demand for high-performance AI mobile phone chips. This convergence of technological push and market pull firmly establishes the AI Mobile Phone Chip Market as a critical and rapidly evolving segment within the broader Consumer Electronics Market, with its innovations frequently setting benchmarks for adjacent segments like the Edge AI Market."

"## Neural Processing Unit Segment in AI Mobile Phone Chip Market

The Neural Processing Unit Market stands as the undisputed dominant segment within the broader AI Mobile Phone Chip Market, primarily categorized under 'Chip Type'. Its supremacy is a direct consequence of the industry's pivot towards on-device AI processing, driven by the critical need for low-latency, enhanced privacy, and reduced reliance on cloud infrastructure. While Graphics Processing Units (GPUs) have historically handled parallel processing tasks, including early AI workloads, and Application-Specific Integrated Circuits (ASICs) offer ultimate efficiency for fixed functions, NPUs are purpose-built architectures optimized for the specific mathematical operations inherent in neural networks, such as matrix multiplications and convolutions. This specialization grants NPUs significant advantages in power efficiency and performance for AI tasks compared to general-purpose CPUs or even GPUs in mobile environments.

The dominance of NPUs stems from their ability to efficiently accelerate a diverse range of AI applications on a smartphone. This includes real-time object recognition for enhanced mobile photography, sophisticated facial recognition and biometric security, always-on virtual assistants responding to voice commands, and power-efficient execution of machine learning models for predictive text, recommendation engines, and adaptive user interfaces. As consumers demand more intelligent and personalized experiences, the processing burden for these tasks falls increasingly on dedicated NPUs. This segment's share is not merely growing but actively consolidating its position as the core AI engine in modern mobile SoCs (System-on-Chips).

Key players like Qualcomm Technologies, Apple, Samsung Electronics, Mediatek, and Huawei are at the forefront of NPU innovation, continually introducing new NPU architectures with each generation of their flagship mobile processors. Qualcomm's Hexagon DSP with dedicated AI accelerators, Apple's Neural Engine, and Samsung's NPU integrated into Exynos chipsets exemplify this trend. These companies are investing heavily in both hardware design and the accompanying software frameworks and development kits (SDKs) to enable developers to harness NPU capabilities effectively. The integration of powerful NPUs is a significant differentiator in the competitive Smartphone Processor Market, directly influencing device performance benchmarks and consumer appeal. The trend is clearly towards more powerful, multi-core NPUs capable of handling increasingly complex AI models, solidifying their dominant position and ensuring continued growth within the AI Mobile Phone Chip Market."

"## Key Market Drivers for the AI Mobile Phone Chip Market

The AI Mobile Phone Chip Market is experiencing robust growth driven by several interconnected technological advancements and evolving consumer demands. A primary driver is the accelerating trend of on-device AI processing, moving computationally intensive tasks from cloud servers to the mobile device itself. This paradigm shift offers significant advantages in terms of data privacy, reduced latency, and decreased reliance on network connectivity. For instance, advanced facial recognition and biometric authentication systems, such as those used for secure payments, are increasingly executed locally by dedicated AI hardware to ensure sensitive data remains on the device, rather than being transmitted to a server.

Another critical driver is the continuous miniaturization and advancement in semiconductor fabrication nodes. The adoption of below 5nm process technologies enables chip manufacturers to integrate more transistors, higher performance AI accelerators, and greater power efficiency into the compact form factors required for smartphones. This technological leap directly impacts the performance ceiling of integrated NPUs and other AI-centric components. For example, the improved transistor density allows for more dedicated AI cores, directly enhancing computational photography algorithms that require immense processing power for real-time image enhancement and video processing.

The proliferation of AI-powered applications across various mobile use cases also acts as a significant market driver. The Mobile Photography Market has been profoundly transformed by AI, with features like scene recognition, object segmentation, low-light enhancement, and computational bokeh heavily relying on AI chip capabilities. Similarly, the demand for sophisticated virtual assistants that offer more natural language understanding and proactive assistance is pushing chip developers to create more powerful and energy-efficient AI engines. The burgeoning Augmented Reality Market on mobile devices also heavily depends on robust AI mobile phone chips for real-time environmental mapping, object tracking, and seamless integration of virtual content into the real world, necessitating high-performance computational vision capabilities. These application-specific demands collectively create a strong pull for innovation and investment in the AI Mobile Phone Chip Market."

"## Competitive Ecosystem of AI Mobile Phone Chip Market

The AI Mobile Phone Chip Market is characterized by intense competition among a few dominant players and several specialized innovators, all vying for market share through innovation in chip architecture, performance, and power efficiency.

October 2024: Qualcomm Technologies unveiled its next-generation Snapdragon flagship mobile platform, featuring a significantly enhanced Hexagon NPU with double the AI processing power for on-device generative AI applications, pushing capabilities for real-time content creation and advanced virtual assistants.

September 2024: Apple introduced its latest A-series chip, incorporating an updated Neural Engine designed to boost performance for complex machine learning models, specifically highlighting improvements in Mobile Photography Market features and advanced computational videography.

July 2024: Mediatek announced a strategic partnership with a leading AI software developer to optimize its Dimensity series chipsets for edge AI inference, focusing on improving performance for smart home integration and personalized user experiences on mid-range devices.

May 2024: Samsung Electronics showcased its new Exynos processor with an integrated AI coprocessor capable of delivering up to 1.5x more power-efficient AI computations, particularly beneficial for always-on features and prolonged AR/VR application usage within the Augmented Reality Market.

March 2024: Arm Holdings launched new CPU and GPU IP cores with tighter integration for AI accelerators, offering improved power efficiency and scalability for next-generation AI mobile phone chip designs from its licensees.

January 2024: Google’s Tensor chip was updated with a focus on enhancing its on-device machine learning capabilities for real-time language translation and advanced speech recognition, demonstrating advancements in processing complex neural network models directly on the device.

November 2023: Advancements in the Advanced Packaging Market enabled chip manufacturers to achieve higher transistor densities and improved thermal management, directly impacting the performance and miniaturization of AI mobile phone chips.

September 2023: A major trend observed was the increased focus on AI-driven power management, where on-chip AI optimizes resource allocation to extend battery life while maintaining high performance for demanding applications like those in the Mobile Gaming Chipset Market."

"## Regional Market Breakdown for AI Mobile Phone Chip Market

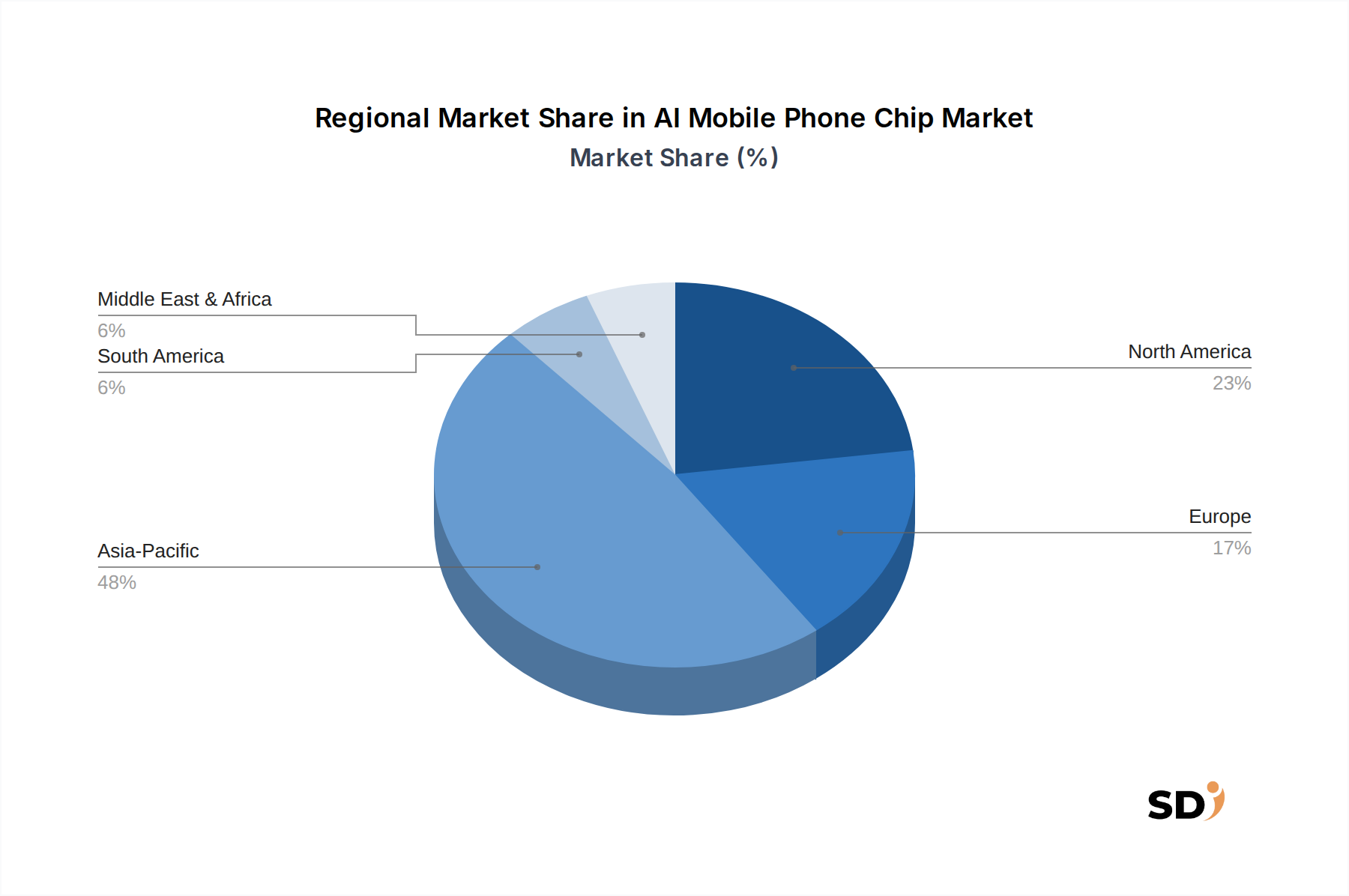

The global AI Mobile Phone Chip Market exhibits distinct regional dynamics, influenced by technological adoption, manufacturing capabilities, and consumer purchasing power. Asia Pacific stands as the largest and fastest-growing region, projected to hold a substantial revenue share throughout the forecast period with an anticipated CAGR significantly above the global average. This dominance is primarily driven by the region's massive smartphone manufacturing hubs in China, South Korea, Japan, and Taiwan, coupled with an immense consumer base and high smartphone penetration rates in countries like India and China. The rapid adoption of AI-enabled features in smartphones, particularly in areas like Mobile Photography Market enhancements and mobile gaming, fuels demand. Key players like Samsung, Huawei, and Mediatek have strong roots and extensive operations within this region.

North America is another significant market, characterized by high-value consumption and a strong focus on premium smartphones. This region is a hub for innovation, with companies like Apple and Qualcomm driving advanced chip development. While its growth rate is robust, it might be slightly lower than Asia Pacific's, reflecting a more mature smartphone market, yet its contribution in terms of average selling price and cutting-edge technology adoption remains critical. The demand here is driven by early adoption of new AI features and services, including advanced AR/VR applications within the Augmented Reality Market.

Europe represents a mature market with a steady demand for AI mobile phone chips, particularly in the premium and mid-range segments. The region benefits from strong regulatory frameworks promoting data privacy, which further incentivizes on-device AI processing. Countries like Germany, France, and the UK are key markets, driven by consumer expectations for high-performance and secure mobile experiences. The CAGR for Europe is expected to be solid, supported by ongoing smartphone upgrades and the increasing integration of AI across various applications.

The Middle East & Africa and South America regions are emerging markets with significant growth potential, albeit from a smaller base. These regions are witnessing increasing smartphone penetration and a growing appetite for affordable yet feature-rich devices, including those with AI capabilities. While initial growth may be concentrated in budget and mid-range AI mobile phone chips, rising disposable incomes and improving digital infrastructure are expected to accelerate demand across all segments. These regions present opportunities for market expansion, particularly for companies offering cost-effective and localized AI solutions."

"## Sustainability & ESG Pressures on AI Mobile Phone Chip Market

Sustainability and ESG (Environmental, Social, and Governance) pressures are increasingly shaping the development and procurement strategies within the AI Mobile Phone Chip Market. A primary environmental concern revolves around the energy efficiency of AI mobile phone chips. As AI tasks become more complex, the computational load increases, potentially leading to higher power consumption and reduced battery life. Manufacturers are under pressure to design NPUs and other AI accelerators that deliver maximum performance per watt, minimizing the carbon footprint associated with device charging and overall energy usage. Innovations in process technology, such as FinFET and Gate-All-Around (GAA) architectures, are crucial in achieving this goal, influencing the Semiconductor Manufacturing Market to prioritize green fabrication methods.

Furthermore, the circular economy mandate impacts material sourcing and end-of-life management. The production of AI chips relies on various critical and sometimes rare earth minerals, prompting scrutiny over ethical sourcing and supply chain transparency. Companies are encouraged to implement responsible mineral sourcing policies to avoid conflict minerals and ensure fair labor practices. The issue of e-waste management is also paramount; as smartphones have shorter upgrade cycles driven by new chip generations, the volume of electronic waste increases. Industry players in the AI Mobile Phone Chip Market are exploring modular designs, easier repairability, and effective recycling programs to mitigate environmental impact.

From a social and governance perspective, the ethical implications of AI are becoming a significant concern. The AI algorithms processed by these chips, particularly in areas like facial recognition and data analysis, raise questions about bias, privacy, and surveillance. Developers and chip manufacturers face pressure to implement 'responsible AI' principles, ensuring fairness, transparency, and accountability in their AI hardware and software solutions. ESG investors are increasingly scrutinizing companies' environmental impact, labor practices, and ethical governance, influencing investment decisions and pushing companies within the AI Mobile Phone Chip Market to adopt more sustainable and responsible business practices across their entire value chain."

"## Export, Trade Flow & Tariff Impact on AI Mobile Phone Chip Market

The AI Mobile Phone Chip Market is intrinsically linked to complex global supply chains, characterized by intricate export and trade flows. Major trade corridors for these chips primarily run from Asia, where the bulk of Semiconductor Manufacturing Market operations are concentrated, to consumer markets worldwide. Leading exporting nations for advanced mobile chips and their components include Taiwan (TSMC, MediaTek), South Korea (Samsung), and China (Huawei's HiSilicon, though under restrictions). The United States, Europe, and other parts of Asia represent major importing regions, consuming these chips for integration into their own consumer electronics devices. The Advanced Packaging Market, a crucial segment for high-performance mobile chips, also follows similar trade patterns, with specialized assembly and test facilities often located in different countries than the initial wafer fabrication.

Recent geopolitical tensions and trade policies, particularly between the United States and China, have significantly impacted cross-border trade volumes and investment strategies. Tariffs and export control restrictions, such as those imposed on certain Chinese technology companies, have altered traditional supply chain configurations, leading to efforts towards regional diversification and reshoring of manufacturing capabilities. For example, restrictions on access to leading-edge fabrication technologies for some Chinese entities have spurred domestic investment in their own chip design and manufacturing, albeit facing technological hurdles.

Non-tariff barriers, including stringent export licensing requirements for dual-use technologies, intellectual property protection concerns, and complex customs regulations, also influence trade flows. These barriers can increase lead times, escalate costs, and limit market access for companies operating in the AI Mobile Phone Chip Market. The globalized nature of the Smartphone Processor Market means that disruptions in any part of the supply chain, whether due to trade disputes, natural disasters, or geopolitical events, can have cascading effects on product availability and pricing worldwide. Companies are increasingly adopting multi-sourcing strategies and building more resilient supply chains to mitigate these risks and ensure uninterrupted access to critical components for their AI mobile phone chip designs.

Qualcomm Technologies: A market leader renowned for its Snapdragon series SoCs, integrating cutting-edge Hexagon DSPs and dedicated AI engines that power a vast majority of premium Android smartphones globally.

Apple: Integrates its custom-designed A-series and M-series chips, featuring a powerful Neural Engine, into its iPhones and iPads, offering highly optimized on-device AI capabilities exclusive to its ecosystem.

Samsung Electronics: Develops its Exynos line of mobile processors, incorporating its own NPU designs to power its flagship Galaxy smartphones, with a strong focus on enhancing photography and intelligent assistant features.

Mediatek: A rapidly growing competitor, providing a broad range of Dimensity series chipsets that deliver competitive AI performance across various price segments, particularly strong in the mid-range Smartphone Processor Market.

Huawei: Through its HiSilicon division, designs its Kirin series chips with integrated NPUs, primarily for its own mobile devices, showcasing advanced AI capabilities for diverse applications.

Google: With its Tensor chips, Google focuses on tightly integrating AI capabilities designed to optimize its Android software experience, particularly for Google Pixel devices' camera and voice processing.

Advanced Micro Devices (AMD): While historically focused on PC and console gaming GPUs, AMD is expanding its AI chip expertise, potentially leveraging its x86 and GPU architectures for mobile or adjacent AI edge applications.

NVIDIA Corporation: A global leader in GPU technology and AI acceleration, NVIDIA's expertise in AI platforms is primarily in data centers and automotive, though its research influences mobile AI chip design.

Arm Holdings: As the foundational intellectual property (IP) provider for most mobile processors, Arm's CPU and GPU architectures, along with its NPU IP, are critical enablers for the entire AI Mobile Phone Chip Market.

Sony Semiconductor Solutions: Known for its camera sensors, Sony's AI developments often focus on integrating AI directly into image processing units, enhancing computational photography capabilities on mobile devices.

Imagination Technologies: Provides GPU and AI accelerator IP that is licensed by various chip manufacturers, offering power-efficient solutions for on-device machine learning and graphics processing.

Others: This segment includes smaller, specialized AI IP providers, emerging startups focused on niche AI acceleration, and regional players contributing to specific components or software optimizations within the mobile AI ecosystem."

"## Recent Developments & Milestones in the AI Mobile Phone Chip Market

Figure 46: Revenue (million), by Price Range 2025 & 2033

Figure 47: Revenue Share (%), by Price Range 2025 & 2033

Figure 48: Revenue (million), by Application 2025 & 2033

Figure 49: Revenue Share (%), by Application 2025 & 2033

Figure 50: Revenue (million), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Chip Type 2020 & 2033

Table 2: Revenue million Forecast, by Fabrication Node 2020 & 2033

Table 3: Revenue million Forecast, by Price Range 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Revenue million Forecast, by Chip Type 2020 & 2033

Table 7: Revenue million Forecast, by Fabrication Node 2020 & 2033

Table 8: Revenue million Forecast, by Price Range 2020 & 2033

Table 9: Revenue million Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Country 2020 & 2033

Table 11: Revenue (million) Forecast, by Application 2020 & 2033

Table 12: Revenue (million) Forecast, by Application 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue million Forecast, by Chip Type 2020 & 2033

Table 15: Revenue million Forecast, by Fabrication Node 2020 & 2033

Table 16: Revenue million Forecast, by Price Range 2020 & 2033

Table 17: Revenue million Forecast, by Application 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue million Forecast, by Chip Type 2020 & 2033

Table 23: Revenue million Forecast, by Fabrication Node 2020 & 2033

Table 24: Revenue million Forecast, by Price Range 2020 & 2033

Table 25: Revenue million Forecast, by Application 2020 & 2033

Table 26: Revenue million Forecast, by Country 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue (million) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Revenue (million) Forecast, by Application 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue million Forecast, by Chip Type 2020 & 2033

Table 37: Revenue million Forecast, by Fabrication Node 2020 & 2033

Table 38: Revenue million Forecast, by Price Range 2020 & 2033

Table 39: Revenue million Forecast, by Application 2020 & 2033

Table 40: Revenue million Forecast, by Country 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue million Forecast, by Chip Type 2020 & 2033

Table 48: Revenue million Forecast, by Fabrication Node 2020 & 2033

Table 49: Revenue million Forecast, by Price Range 2020 & 2033

Table 50: Revenue million Forecast, by Application 2020 & 2033

Table 51: Revenue million Forecast, by Country 2020 & 2033

Table 52: Revenue (million) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Revenue (million) Forecast, by Application 2020 & 2033

Table 55: Revenue (million) Forecast, by Application 2020 & 2033

Table 56: Revenue (million) Forecast, by Application 2020 & 2033

Table 57: Revenue (million) Forecast, by Application 2020 & 2033

Table 58: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Primary research constitutes the cornerstone of our market analysis, accounting for approximately 75% of the total research effort. This robust approach ensures the collection of real-time, proprietary data directly from key industry participants, offering unparalleled insights into market dynamics, emerging trends, competitive landscapes, and future projections. Our primary research strategy involves a meticulously structured program of in-depth interviews, conducted predominantly via telephonic and web-based platforms, with industry leaders, technology experts, and decision-makers across the AI Mobile Phone Chip value chain. These qualitative and quantitative discussions are designed to validate secondary findings, gather granular data points, and capture nuanced perspectives not available through other means.

Our interview panel is strategically segmented to cover the breadth of the market's ecosystem. Key company types engaged include:

AI Mobile SoC Design Houses

Advanced Semiconductor Foundries

Mobile Device Original Equipment Manufacturers (OEMs)

AI IP Core Providers

Mobile Application Developers leveraging on-device AI

Interviews are conducted with specific, influential stakeholders to ensure the highest quality of information. Typical job titles engaged in our primary research include:

VP, Product Management (Mobile SoCs)

Head of AI/ML Engineering (Mobile Devices)

Senior Director, Foundry Technology & Operations

Principal Architect, Mobile AI Solutions

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP, Product Management (Mobile SoCs)

30%

Head of AI/ML Engineering (Mobile Devices)

25%

Senior Director, Foundry Technology & Operations

25%

Principal Architect, Mobile AI Solutions

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

AI Mobile SoC Design Houses

30%

Advanced Semiconductor Foundries

25%

Mobile Device Original Equipment Manufacturers (OEMs)

20%

AI IP Core Providers

15%

Mobile Application Developers leveraging on-device AI

10%

Secondary Research & Industry Benchmarking

The remaining 25% of our research effort is dedicated to comprehensive secondary research and rigorous industry benchmarking. This phase involves extensive data mining from a diverse array of credible, publicly available sources to establish a foundational understanding of the market, identify key trends, and corroborate primary research findings. Our secondary research framework systematically leverages:

Financial Databases: Including but not limited to Bloomberg, Factiva, Hoovers, and PitchBook, providing critical financial performance data, investment trends, and company profiles.

Government & Regulatory Publications: Official reports, policy documents, and statistical data from relevant .Gov agencies globally. For example, data from national statistical offices or trade ministries relating to mobile technology adoption or semiconductor manufacturing policies.

Organizational & Trade Association Publications: Reports, whitepapers, and statistical releases from reputable industry organizations (.org) and trade associations that provide industry-specific data and perspectives. Key organizations include:

SEMI (Semiconductor Industry Association) [Source]

GSMA (Global System for Mobile Communications Association) [Source]

Institute of Electrical and Electronics Engineers (IEEE) [Source] for technical standards and publications.

Company Annual Reports & Investor Presentations: Publicly available documents offering insights into corporate strategies, R&D investments, and market outlooks.

Academic Journals & Research Papers: Peer-reviewed publications providing in-depth scientific and technological analysis relevant to AI chip development and mobile integration.

All secondary data is cross-referenced and validated against multiple sources to ensure accuracy and reliability. Our policy mandates excluding data sourced from other market research websites to maintain the integrity and originality of our findings.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodology employs a robust combination of top-down and bottom-up approaches, further strengthened by multi-level data triangulation. This ensures a holistic and accurate estimation of the AI Mobile Phone Chip market:

Bottom-Up Approach: This method involves segmenting the market into its smallest constituent parts (e.g., by chip type, fabrication node, application, and region), estimating each segment individually, and then aggregating these estimates to arrive at the overall market size. Key metrics and variables used for bottom-up calculation include:

Global Shipments of AI-enabled Mobile Handsets

Average Selling Price (ASP) of AI Mobile Chips by Chip Type and Fabrication Node

Penetration Rate of Dedicated AI Accelerators (e.g., NPUs, TPUs) in Mobile SoCs

Revenue Contribution per AI Mobile Chip Application Segment

Top-Down Approach: This approach starts with a broader market estimate (e.g., total mobile SoC market or overall semiconductor market) and then applies relevant market share, penetration rates, and growth factors to derive the AI Mobile Phone Chip market size.

Multi-Level Data Triangulation: All market figures are subjected to rigorous triangulation, cross-referencing data points from primary interviews, secondary sources, and internal databases to ensure consistency and validate estimations across different perspectives and data collection methods.

Our forecasting model incorporates macroeconomic factors, technological advancements, regulatory changes, and competitive intelligence to project market growth from 2026 to 2034, segmented across all defined parameters.

Data Accuracy & Quality Check

We are committed to delivering highly reliable and accurate market intelligence. Through our rigorous methodology, we guarantee an estimated data accuracy level of 85-90%. Every report generated undergoes a stringent multi-stage quality control process, including data validation, analytical review, and peer review by senior analysts. This comprehensive quality assurance framework ensures that the data presented is consistent, verifiable, and reflective of current market realities.

Furthermore, our commitment to providing the most current market insights means that every report is meticulously updated with the latest available data and market developments up to the date of purchase. This continuous update mechanism ensures clients receive the most relevant and actionable intelligence for their strategic decision-making.

Frequently Asked Questions

1. What are the primary applications driving demand for AI mobile phone chips?

Demand for AI mobile phone chips is driven by enhanced mobile photography, virtual assistants, and real-time language translation. Other significant applications include facial recognition, AR/VR, and mobile gaming, all requiring on-device processing capabilities.

2. Which region presents the most significant growth opportunities for AI mobile phone chip manufacturers?

Asia-Pacific, encompassing countries like China, India, Japan, and South Korea, offers substantial growth for AI mobile phone chip manufacturers. Rapid smartphone adoption and evolving consumer AI feature demand in this region support its expansion.

3. Why is Asia-Pacific a dominant region in the AI mobile phone chip market?

Asia-Pacific dominates the AI mobile phone chip market due to its robust smartphone manufacturing ecosystem, with companies like Samsung and Huawei. The region also has a vast consumer base rapidly adopting AI-powered mobile features, contributing to its estimated 48% market share.

4. Who are the leading companies in the AI mobile phone chip competitive landscape?

Qualcomm Technologies, Apple, Samsung Electronics, and MediaTek are key players in the AI mobile phone chip market. These companies compete by integrating advanced AI capabilities like NPUs into their chipsets, enhancing mobile device performance and user experience.

5. What are the key supply chain considerations for AI mobile phone chip production?

The AI mobile phone chip supply chain heavily relies on advanced semiconductor fabrication capabilities, often concentrated in specific regions. Ensuring stable access to raw materials and maintaining robust manufacturing partnerships are critical for production continuity and cost efficiency.

6. What is the current investment activity within the AI mobile phone chip sector?

Investment in the AI mobile phone chip sector is driven by the growing demand for on-device AI processing and advancements in fabrication technology. Companies and venture capital firms are investing in R&D for next-generation Neural Processing Units (NPUs) and efficient chip architectures to capture market share.