Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

4-inch SiC Epitaxial Wafer: $1.3B, 18.04% CAGR Growth

4-inch SiC Epitaxial Wafer

4-inch SiC Epitaxial Wafer: $1.3B, 18.04% CAGR Growth

4-inch SiC Epitaxial Wafer by Type (N-Type, P-Type), by Voltage (Below 650 V, 650-1200 V, 1200-3300 V, Above 3300 V), by Production Technology (Chemical Vapor Deposition (CVD) Epitaxy, Hot-Wall CVD Epitaxy, Chlorinated Chemistry Epitaxy, Others), by End-Use Industry (Automotive & Transportation, Energy & Power, Telecommunications & RF Infrastructure, Aerospace, Defense & Space, Data Centers & Information Technology, Consumer Electronics, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 3, 2026|Base Year : 2025|Pages : 101

Key Insights for 4-inch SiC Epitaxial Wafer Market

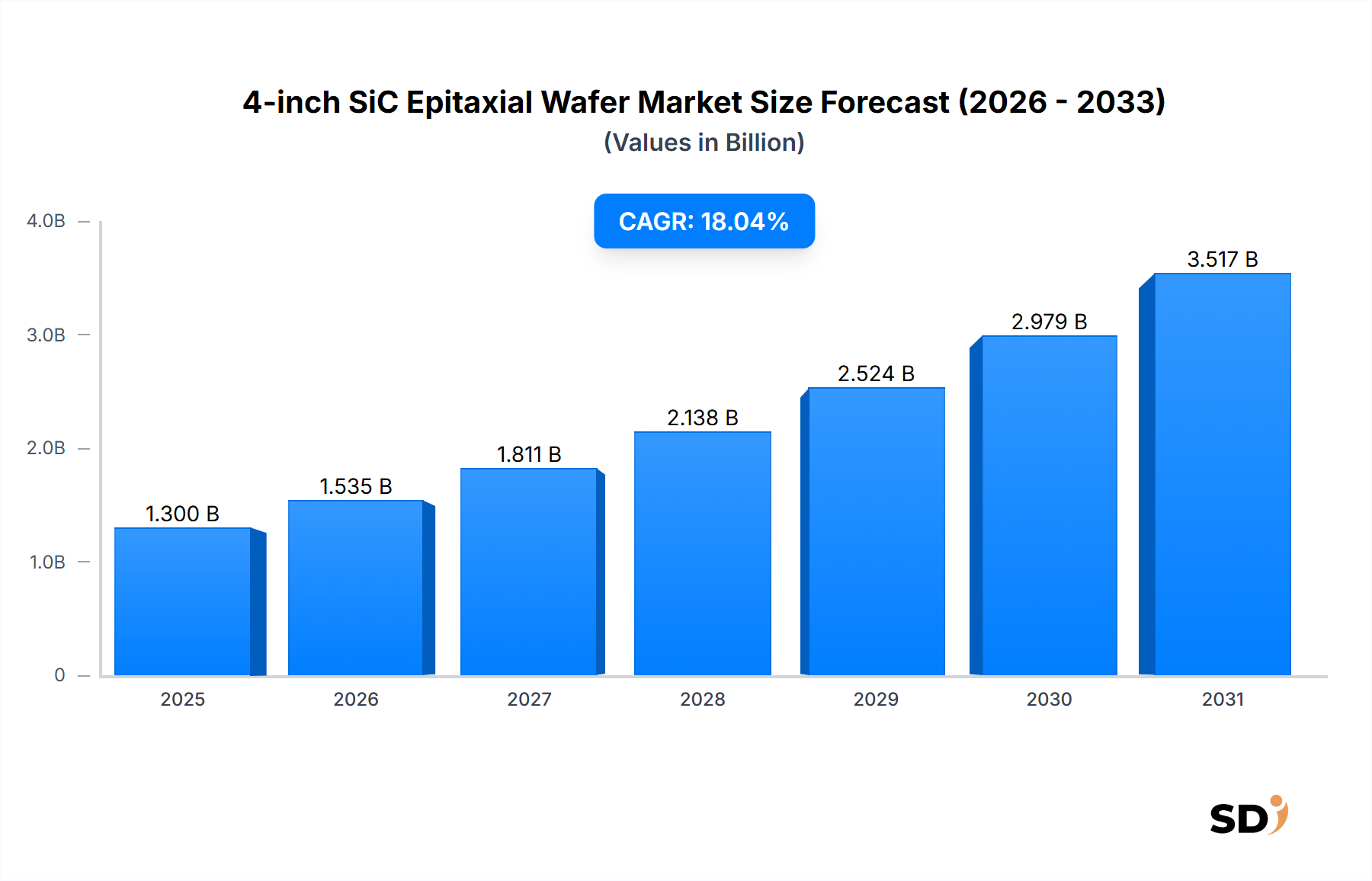

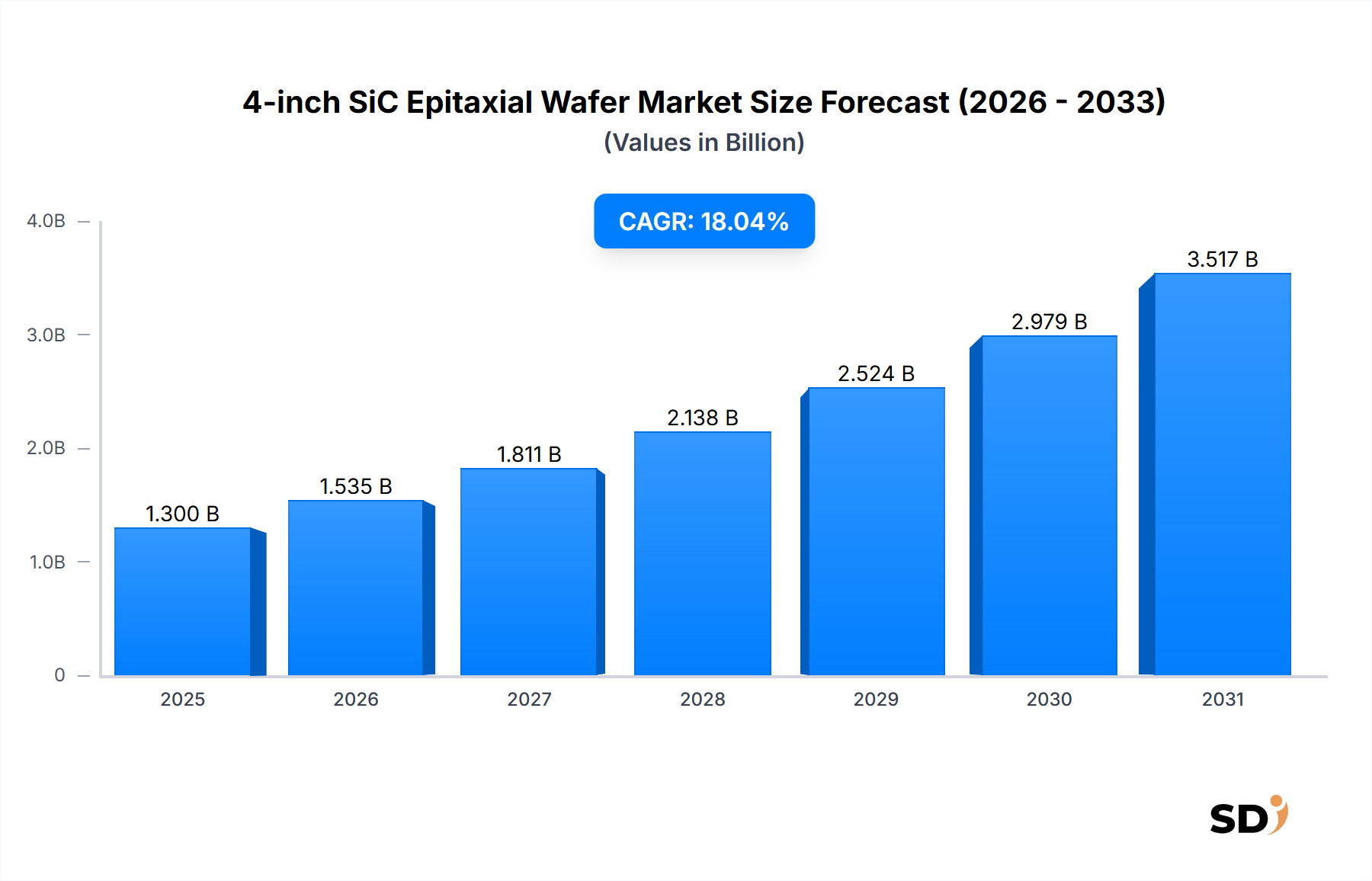

The global 4-inch SiC Epitaxial Wafer Market is positioned for robust expansion, driven by accelerating demand for high-performance power electronics across critical industries. Valued at an estimated $1.3 billion in 2024, the market is projected to grow at an impressive Compound Annual Growth Rate (CAGR) of 18.04% through the forecast period. This significant growth trajectory is underpinned by the intrinsic advantages of silicon carbide (SiC) over conventional silicon, particularly in applications requiring higher efficiency, increased power density, and superior thermal management. The transition towards electrification in the Automotive & Transportation sector represents a primary demand catalyst, as SiC epitaxial wafers are foundational components for inverters, onboard chargers, and DC-DC converters in electric vehicles (EVs) and hybrid electric vehicles (HEVs). These wafers enable compact, lighter, and more efficient power modules, directly contributing to extended battery range and faster charging capabilities.

4-inch SiC Epitaxial Wafer Market Size (In Billion)

4.0B

3.0B

2.0B

1.0B

0

1.300 B

2025

1.535 B

2026

1.811 B

2027

2.138 B

2028

2.524 B

2029

2.979 B

2030

3.517 B

2031

Beyond automotive, the proliferation of renewable energy infrastructure is a substantial macro tailwind for the 4-inch SiC Epitaxial Wafer Market. SiC power devices are integral to solar inverters, wind turbine converters, and energy storage systems, where their high breakdown voltage and low switching losses optimize energy conversion and reduce overall system costs. Furthermore, the rapid deployment of 5G telecommunications networks and the expansion of data centers are creating additional demand for SiC-based RF and power management solutions. These applications benefit from SiC's ability to operate at higher frequencies and temperatures, ensuring reliable performance in demanding environments. The continuous advancements in Chemical Vapor Deposition (CVD) Epitaxy technologies are crucial for producing high-quality 4-inch SiC epitaxial layers with reduced defect densities and improved uniformity, which are vital for enhancing device yield and reliability. As the technological landscape evolves, the SiC Power Devices Market is expected to leverage these advancements, further solidifying the position of 4-inch SiC epitaxial wafers as a cornerstone of next-generation power electronics.

Automotive & Transportation Segment Dominates in 4-inch SiC Epitaxial Wafer Market

The Automotive & Transportation sector stands as the unequivocally dominant end-use industry segment within the 4-inch SiC Epitaxial Wafer Market, commanding the largest revenue share. This supremacy is a direct consequence of the global automotive industry's aggressive pivot towards electrification. SiC power devices, fabricated on these advanced epitaxial wafers, are indispensable for the high-voltage and high-current applications inherent to modern electric vehicles. Specifically, they are critical components in traction inverters, which convert DC battery power into AC for electric motors; onboard chargers, which manage power from external charging stations; and DC-DC converters, which regulate voltage levels for various vehicle systems. The superior performance characteristics of SiC, including its higher electron mobility, wider bandgap, and excellent thermal conductivity, enable power modules to operate at higher switching frequencies and temperatures with significantly lower power losses compared to traditional silicon-based devices. This translates directly into more compact and lighter designs, which are vital for optimizing vehicle performance, enhancing fuel efficiency (or battery range for EVs), and reducing overall system weight.

Within this dominant segment, key players in the 4-inch SiC Epitaxial Wafer Market, such as Wolfspeed, Inc. and Resonac Corporation, have established strong partnerships and supply agreements with leading automotive OEMs and Tier 1 suppliers. These collaborations are crucial for co-developing application-specific SiC solutions that meet the stringent reliability and performance requirements of the automotive industry. The share of this segment is not only dominant but also experiencing accelerated growth, driven by several factors. Government mandates and incentives promoting EV adoption, increasing consumer demand for greener transportation, and continuous technological advancements in battery technology all contribute to this expansion. The inherent efficiency gains offered by SiC components allow for faster EV charging times and longer driving ranges, addressing key consumer concerns and accelerating the mass adoption of electric vehicles. As the global Automotive Electronics Market continues its profound transformation, the demand for high-quality 4-inch SiC epitaxial wafers is expected to sustain its upward trajectory, further consolidating the Automotive & Transportation segment's leadership position within the broader SiC ecosystem. This trend highlights a strategic shift where manufacturers are increasingly investing in dedicated SiC fabrication facilities to meet the escalating requirements of the automotive sector, ensuring both supply chain robustness and technological superiority.

Key Market Drivers & Constraints for 4-inch SiC Epitaxial Wafer Market

The growth trajectory of the 4-inch SiC Epitaxial Wafer Market is fundamentally shaped by a confluence of potent market drivers and inherent structural constraints. A primary driver is the pervasive trend of vehicle electrification, with the global electric vehicle market projected for substantial annual growth exceeding 20% over the next decade. This necessitates advanced power electronics for efficient energy conversion, a domain where SiC-based devices excel. For instance, SiC power modules in EV inverters can reduce power losses by up to 50% compared to silicon-based IGBTs, directly enhancing battery range and charging speed. This shift directly bolsters demand for 4-inch SiC epitaxial wafers as a foundational material.

Another significant driver is the increasing global investment in renewable energy infrastructure. The Energy & Power Electronics Market, particularly for solar inverters and wind power converters, is rapidly integrating SiC technology to maximize energy harvesting efficiency. For example, SiC inverters for solar PV systems can achieve efficiencies exceeding 99%, significantly higher than silicon alternatives, translating into greater power output from the same solar array. The expanding Telecommunications Equipment Market and growth in data centers also represent strong drivers. SiC devices offer superior performance in high-frequency RF applications and power supplies, addressing the escalating power consumption and thermal management challenges in these sectors. Finally, the inherent material properties of SiC, such as its higher breakdown voltage (up to 10x that of Si), superior thermal conductivity (up to 3x), and lower switching losses, make it the preferred choice for demanding power applications above 650 V.

However, the market faces notable constraints. The high manufacturing cost of SiC epitaxial wafers remains a significant barrier compared to mature silicon wafer technology. The raw material processing and epitaxy steps are complex and energy-intensive, directly contributing to higher per-wafer costs. Moreover, the scalability of SiC production, especially transitioning from 4-inch to 6-inch and 8-inch wafers, presents technical challenges related to crystal growth defects and yield management. The industry is characterized by a concentrated supply chain with a limited number of major players, which can lead to potential bottlenecks and supply stability concerns, particularly during periods of surging demand. While efforts are underway to address these constraints through R&D and capital investments, they continue to influence market dynamics and adoption rates.

Competitive Ecosystem of 4-inch SiC Epitaxial Wafer Market

The 4-inch SiC Epitaxial Wafer Market is characterized by a focused competitive landscape, where leading material science and semiconductor companies are making significant investments to capitalize on surging demand from power electronics applications.

Wolfspeed, Inc.: A global leader in silicon carbide technology, Wolfspeed focuses on providing comprehensive SiC solutions, from substrates and epitaxial wafers to discrete devices and power modules, maintaining a strong position through continuous R&D and strategic capacity expansions.

SK Siltron Co., Ltd.: A prominent player aggressively expanding its presence in the SiC wafer segment, SK Siltron is investing heavily in manufacturing facilities and R&D to enhance its epitaxy capabilities and meet the growing global demand for advanced semiconductor materials.

EpiWorld International Co., Ltd.: Based in China, EpiWorld International specializes in SiC epitaxial materials, focusing on product innovation and quality to serve the rapidly expanding domestic and international markets for power electronics and RF devices.

TYSiC Co., Ltd.: TYSiC is a dedicated supplier of SiC materials, including substrates and epitaxial wafers, concentrating on advanced material science to improve crystal growth techniques and defect reduction for high-performance applications.

Homray Material Technology Co., Ltd.: This company focuses on advanced material solutions for the semiconductor industry, leveraging its expertise in material synthesis and processing to produce high-quality SiC epitaxial wafers for demanding applications.

JXT Technology Co., Ltd.: JXT Technology is an emerging innovator in semiconductor materials, contributing to the development and supply of critical components like SiC epitaxial wafers, with an emphasis on performance and reliability.

Resonac Corporation: A diversified chemical company, Resonac (formerly Showa Denko) holds a significant position in the SiC materials market, offering high-quality SiC epitaxial wafers and contributing to the advancement of wide bandgap semiconductors.

Coherent Corp.: A global leader in materials, networking, and lasers, Coherent Corp. (formerly II-VI Incorporated) is a key supplier of SiC substrates and epitaxial wafers, benefiting from its deep expertise in crystal growth and precision materials engineering.

Recent Developments & Milestones in 4-inch SiC Epitaxial Wafer Market

The 4-inch SiC Epitaxial Wafer Market has been marked by several strategic advancements and investments, reflecting the industry's response to escalating demand and technological evolution.

Q4 2023: Several leading manufacturers announced significant capital expenditure expansions for SiC wafer and epitaxy production facilities, aimed at dramatically increasing output to address the surging demand from the Automotive Electronics Market and other high-growth sectors. These investments are critical for securing long-term supply capabilities.

Q2 2024: Collaborative R&D initiatives between epi-wafer suppliers and power module manufacturers intensified, focusing on optimizing SiC device performance, particularly for 650-1200 V applications. These partnerships are crucial for integrating advanced materials with device designs, leading to more robust and efficient power solutions.

Q1 2024: Breakthroughs in Chemical Vapor Deposition Market technologies were reported, leading to reduced defect densities and improved yield rates for 4-inch SiC epitaxial wafers. These process enhancements are vital for driving down manufacturing costs and increasing the overall quality and reliability of the wafers.

Q3 2023: Strategic long-term supply agreements were formalized between major automotive Tier 1 suppliers and key 4-inch SiC Epitaxial Wafer Market producers. These agreements aim to secure a stable and predictable supply of SiC materials for upcoming electric vehicle programs, mitigating potential supply chain risks.

Q1 2023: New material characterization techniques and in-line metrology solutions were introduced, enabling faster and more precise defect detection during the epitaxy process. This enhances quality control and accelerates the feedback loop for process optimization, benefiting the overall N-Type SiC Wafer Market segment.

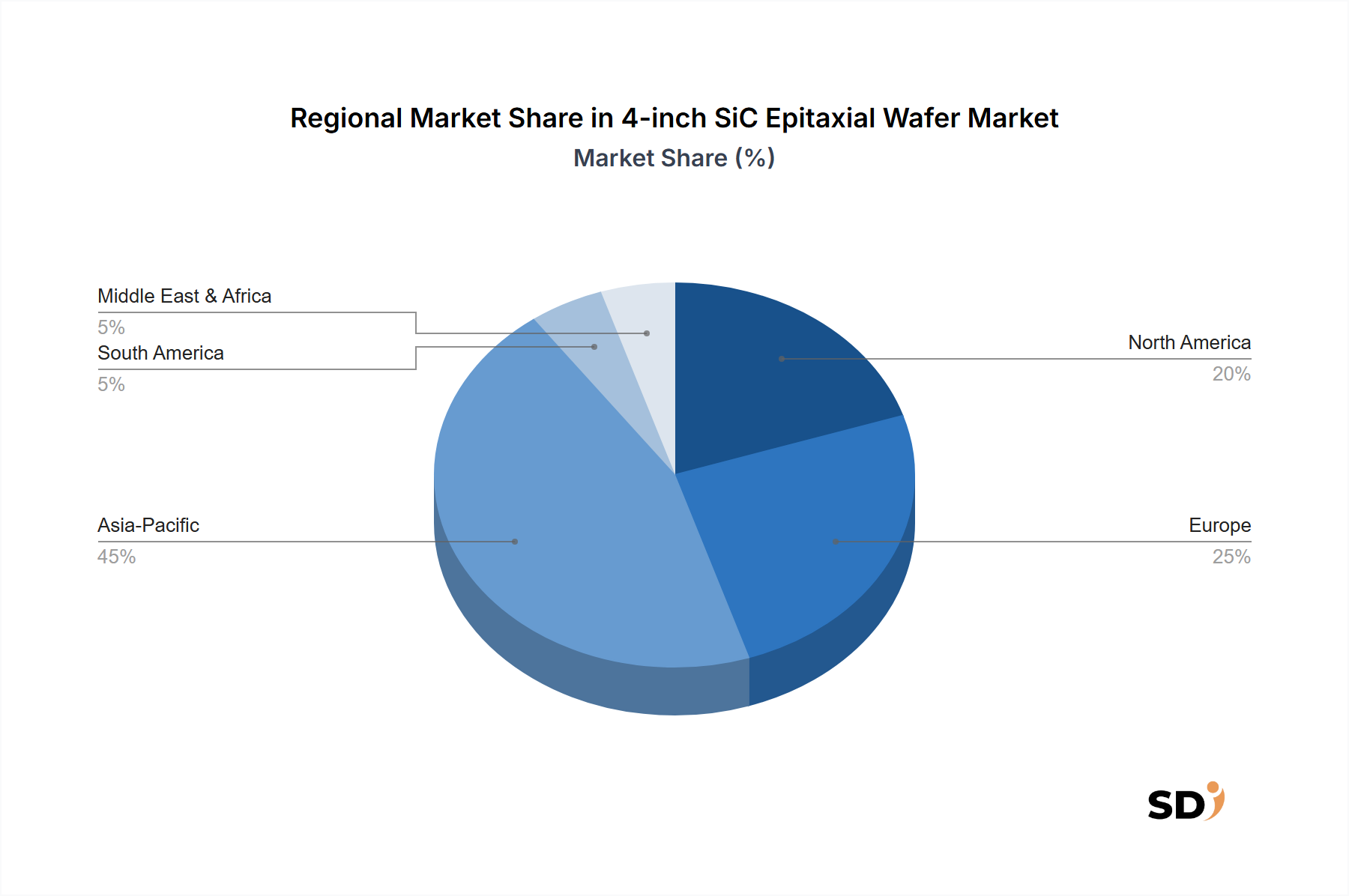

Regional Market Breakdown for 4-inch SiC Epitaxial Wafer Market

The global 4-inch SiC Epitaxial Wafer Market exhibits distinct regional dynamics, influenced by varying industrial infrastructures, government policies, and technological adoption rates. Asia Pacific is anticipated to emerge as the largest and fastest-growing region, primarily driven by its robust automotive manufacturing base, particularly in China, Japan, and South Korea, which are at the forefront of electric vehicle production. Additionally, significant investments in renewable energy projects, particularly solar and wind power, coupled with the rapid expansion of the Telecommunications Equipment Market, fuel substantial demand for SiC power devices across the region. Countries like India are also witnessing burgeoning industrial and EV sectors, further contributing to regional growth.

North America holds a substantial share in the market, characterized by strong R&D capabilities, early adoption of SiC technology in high-reliability applications such as aerospace and defense, and a significant presence of key market players like Wolfspeed, Inc. The region's push towards vehicle electrification and modernization of its energy grid provides consistent demand for 4-inch SiC epitaxial wafers. Innovation in power electronics design and manufacturing also originates heavily from this region.

Europe represents a mature yet rapidly growing market, propelled by stringent environmental regulations and ambitious decarbonization targets that accelerate the adoption of EVs and renewable energy systems. Countries such as Germany, France, and Italy are leading the charge in developing advanced SiC-based power solutions for automotive and industrial applications. The region benefits from a strong ecosystem of research institutions and component manufacturers, fostering continuous innovation in SiC technology.

Emerging regions, encompassing Middle East & Africa and South America, are showing nascent but promising growth. Demand in these areas is primarily driven by expanding industrial applications, increasing investments in renewable energy infrastructure, and gradual adoption of electric mobility solutions. While currently smaller in market share, these regions are expected to contribute increasingly to the global 4-inch SiC Epitaxial Wafer Market as their economies develop and technological adoption accelerates.

Sustainability & ESG Pressures on 4-inch SiC Epitaxial Wafer Market

The 4-inch SiC Epitaxial Wafer Market is increasingly subject to rigorous sustainability and ESG (Environmental, Social, and Governance) pressures, fundamentally reshaping product development and procurement strategies. The inherent energy efficiency of SiC devices is a major advantage, as they enable substantial reductions in energy consumption and greenhouse gas emissions in end-user applications such as electric vehicles and renewable energy systems. This intrinsic benefit aligns perfectly with global carbon neutrality targets and the drive for a greener economy, positioning SiC as a critical enabler of sustainable technology. Consequently, manufacturers of 4-inch SiC epitaxial wafers are under pressure to demonstrate the environmental benefits of their products throughout the entire lifecycle.

However, the manufacturing process itself, particularly crystal growth and epitaxy, is energy-intensive. This has led to increased scrutiny over the carbon footprint of production facilities. Companies are responding by investing in renewable energy sources for their fabrication plants, optimizing process parameters to reduce energy consumption, and exploring more environmentally benign etching and cleaning chemistries. For instance, the Automotive Electronics Market and the Energy & Power Electronics Market, major consumers of SiC wafers, are increasingly prioritizing suppliers who can demonstrate robust ESG credentials, including transparent supply chains, reduced waste generation, and responsible water management. Furthermore, investors are increasingly factoring ESG performance into their decision-making, influencing capital allocation and strategic direction within the Wide Bandgap Semiconductor Market. Circular economy principles are also gaining traction, with research into recycling pathways for SiC materials and exploring options for reducing material waste during wafer processing. Adherence to international environmental regulations, such as RoHS and REACH, is a baseline expectation, but the market is moving towards more proactive sustainability measures that aim for a net positive environmental impact.

Supply Chain & Raw Material Dynamics for 4-inch SiC Epitaxial Wafer Market

The supply chain for the 4-inch SiC Epitaxial Wafer Market is characterized by significant upstream dependencies and inherent sourcing risks, profoundly impacting market stability and pricing. The primary raw material is silicon carbide powder, which is synthesized into SiC ingots, then sliced into Silicon Carbide Substrate Market wafers, and finally coated with an epitaxial layer. The production of high-purity SiC substrates is a highly specialized process, involving extreme temperatures and pressures, leading to a concentrated supply base dominated by a few key players. This concentration inherently creates sourcing risks, as geopolitical events, trade policies, or natural disasters affecting these core suppliers can lead to significant supply disruptions and price volatility.

Key inputs for the epitaxial growth process, predominantly Chemical Vapor Deposition (CVD) Epitaxy, include high-purity gases such as silane (SiH4) or chlorosilanes (e.g., methyltrichlorosilane – MTS) as silicon precursors, and carbon-containing gases (e.g., propane) as carbon precursors, along with dopant gases. The availability and stable pricing of these specialty gases are crucial. Historically, disruptions such as the COVID-19 pandemic have highlighted the vulnerability of global supply chains, leading to extended lead times and fluctuating raw material costs that impact the final price of SiC epitaxial wafers. This has prompted efforts towards regionalization and diversification of supply chains, with companies investing in local substrate manufacturing capabilities and establishing redundant sourcing strategies. The overall Compound Semiconductor Market has also experienced similar pressures. Price trends for SiC substrates have generally been upward due to surging demand, particularly from the automotive sector, while innovations in epitaxy aim to reduce material waste and improve yield, partially offsetting these cost pressures. Effective supply chain management, including long-term agreements with material suppliers and strategic inventory management, is critical for mitigating risks and ensuring the consistent availability of 4-inch SiC epitaxial wafers to meet escalating industry demand.

4-inch SiC Epitaxial Wafer Segmentation

1. Type

1.1. N-Type

1.2. P-Type

2. Voltage

2.1. Below 650 V

2.2. 650-1200 V

2.3. 1200-3300 V

2.4. Above 3300 V

3. Production Technology

3.1. Chemical Vapor Deposition (CVD) Epitaxy

3.2. Hot-Wall CVD Epitaxy

3.3. Chlorinated Chemistry Epitaxy

3.4. Others

4. End-Use Industry

4.1. Automotive & Transportation

4.2. Energy & Power

4.3. Telecommunications & RF Infrastructure

4.4. Aerospace, Defense & Space

4.5. Data Centers & Information Technology

4.6. Consumer Electronics

4.7. Others

4-inch SiC Epitaxial Wafer Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

4-inch SiC Epitaxial Wafer REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 18.04% from 2020-2034

Segmentation

By Type

N-Type

P-Type

By Voltage

Below 650 V

650-1200 V

1200-3300 V

Above 3300 V

By Production Technology

Chemical Vapor Deposition (CVD) Epitaxy

Hot-Wall CVD Epitaxy

Chlorinated Chemistry Epitaxy

Others

By End-Use Industry

Automotive & Transportation

Energy & Power

Telecommunications & RF Infrastructure

Aerospace, Defense & Space

Data Centers & Information Technology

Consumer Electronics

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Type

5.1.1. N-Type

5.1.2. P-Type

5.2. Market Analysis, Insights and Forecast - by Voltage

5.2.1. Below 650 V

5.2.2. 650-1200 V

5.2.3. 1200-3300 V

5.2.4. Above 3300 V

5.3. Market Analysis, Insights and Forecast - by Production Technology

5.3.1. Chemical Vapor Deposition (CVD) Epitaxy

5.3.2. Hot-Wall CVD Epitaxy

5.3.3. Chlorinated Chemistry Epitaxy

5.3.4. Others

5.4. Market Analysis, Insights and Forecast - by End-Use Industry

5.4.1. Automotive & Transportation

5.4.2. Energy & Power

5.4.3. Telecommunications & RF Infrastructure

5.4.4. Aerospace, Defense & Space

5.4.5. Data Centers & Information Technology

5.4.6. Consumer Electronics

5.4.7. Others

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Type

6.1.1. N-Type

6.1.2. P-Type

6.2. Market Analysis, Insights and Forecast - by Voltage

6.2.1. Below 650 V

6.2.2. 650-1200 V

6.2.3. 1200-3300 V

6.2.4. Above 3300 V

6.3. Market Analysis, Insights and Forecast - by Production Technology

6.3.1. Chemical Vapor Deposition (CVD) Epitaxy

6.3.2. Hot-Wall CVD Epitaxy

6.3.3. Chlorinated Chemistry Epitaxy

6.3.4. Others

6.4. Market Analysis, Insights and Forecast - by End-Use Industry

6.4.1. Automotive & Transportation

6.4.2. Energy & Power

6.4.3. Telecommunications & RF Infrastructure

6.4.4. Aerospace, Defense & Space

6.4.5. Data Centers & Information Technology

6.4.6. Consumer Electronics

6.4.7. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Type

7.1.1. N-Type

7.1.2. P-Type

7.2. Market Analysis, Insights and Forecast - by Voltage

7.2.1. Below 650 V

7.2.2. 650-1200 V

7.2.3. 1200-3300 V

7.2.4. Above 3300 V

7.3. Market Analysis, Insights and Forecast - by Production Technology

7.3.1. Chemical Vapor Deposition (CVD) Epitaxy

7.3.2. Hot-Wall CVD Epitaxy

7.3.3. Chlorinated Chemistry Epitaxy

7.3.4. Others

7.4. Market Analysis, Insights and Forecast - by End-Use Industry

7.4.1. Automotive & Transportation

7.4.2. Energy & Power

7.4.3. Telecommunications & RF Infrastructure

7.4.4. Aerospace, Defense & Space

7.4.5. Data Centers & Information Technology

7.4.6. Consumer Electronics

7.4.7. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Type

8.1.1. N-Type

8.1.2. P-Type

8.2. Market Analysis, Insights and Forecast - by Voltage

8.2.1. Below 650 V

8.2.2. 650-1200 V

8.2.3. 1200-3300 V

8.2.4. Above 3300 V

8.3. Market Analysis, Insights and Forecast - by Production Technology

8.3.1. Chemical Vapor Deposition (CVD) Epitaxy

8.3.2. Hot-Wall CVD Epitaxy

8.3.3. Chlorinated Chemistry Epitaxy

8.3.4. Others

8.4. Market Analysis, Insights and Forecast - by End-Use Industry

8.4.1. Automotive & Transportation

8.4.2. Energy & Power

8.4.3. Telecommunications & RF Infrastructure

8.4.4. Aerospace, Defense & Space

8.4.5. Data Centers & Information Technology

8.4.6. Consumer Electronics

8.4.7. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Type

9.1.1. N-Type

9.1.2. P-Type

9.2. Market Analysis, Insights and Forecast - by Voltage

9.2.1. Below 650 V

9.2.2. 650-1200 V

9.2.3. 1200-3300 V

9.2.4. Above 3300 V

9.3. Market Analysis, Insights and Forecast - by Production Technology

9.3.1. Chemical Vapor Deposition (CVD) Epitaxy

9.3.2. Hot-Wall CVD Epitaxy

9.3.3. Chlorinated Chemistry Epitaxy

9.3.4. Others

9.4. Market Analysis, Insights and Forecast - by End-Use Industry

9.4.1. Automotive & Transportation

9.4.2. Energy & Power

9.4.3. Telecommunications & RF Infrastructure

9.4.4. Aerospace, Defense & Space

9.4.5. Data Centers & Information Technology

9.4.6. Consumer Electronics

9.4.7. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Type

10.1.1. N-Type

10.1.2. P-Type

10.2. Market Analysis, Insights and Forecast - by Voltage

10.2.1. Below 650 V

10.2.2. 650-1200 V

10.2.3. 1200-3300 V

10.2.4. Above 3300 V

10.3. Market Analysis, Insights and Forecast - by Production Technology

10.3.1. Chemical Vapor Deposition (CVD) Epitaxy

10.3.2. Hot-Wall CVD Epitaxy

10.3.3. Chlorinated Chemistry Epitaxy

10.3.4. Others

10.4. Market Analysis, Insights and Forecast - by End-Use Industry

10.4.1. Automotive & Transportation

10.4.2. Energy & Power

10.4.3. Telecommunications & RF Infrastructure

10.4.4. Aerospace, Defense & Space

10.4.5. Data Centers & Information Technology

10.4.6. Consumer Electronics

10.4.7. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Wolfspeed Inc.

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. SK Siltron Co. Ltd.

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. EpiWorld International Co. Ltd.

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. TYSiC Co. Ltd.

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Homray Material Technology Co. Ltd.

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. JXT Technology Co. Ltd.

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Resonac Corporation

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Coherent Corp.

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Others

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Type 2025 & 2033

Figure 3: Revenue Share (%), by Type 2025 & 2033

Figure 4: Revenue (billion), by Voltage 2025 & 2033

Figure 5: Revenue Share (%), by Voltage 2025 & 2033

Figure 6: Revenue (billion), by Production Technology 2025 & 2033

Figure 7: Revenue Share (%), by Production Technology 2025 & 2033

Figure 8: Revenue (billion), by End-Use Industry 2025 & 2033

Figure 9: Revenue Share (%), by End-Use Industry 2025 & 2033

Figure 10: Revenue (billion), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (billion), by Type 2025 & 2033

Figure 13: Revenue Share (%), by Type 2025 & 2033

Figure 14: Revenue (billion), by Voltage 2025 & 2033

Figure 15: Revenue Share (%), by Voltage 2025 & 2033

Figure 16: Revenue (billion), by Production Technology 2025 & 2033

Figure 17: Revenue Share (%), by Production Technology 2025 & 2033

Figure 18: Revenue (billion), by End-Use Industry 2025 & 2033

Figure 19: Revenue Share (%), by End-Use Industry 2025 & 2033

Figure 20: Revenue (billion), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (billion), by Type 2025 & 2033

Figure 23: Revenue Share (%), by Type 2025 & 2033

Figure 24: Revenue (billion), by Voltage 2025 & 2033

Figure 25: Revenue Share (%), by Voltage 2025 & 2033

Figure 26: Revenue (billion), by Production Technology 2025 & 2033

Figure 27: Revenue Share (%), by Production Technology 2025 & 2033

Figure 28: Revenue (billion), by End-Use Industry 2025 & 2033

Figure 29: Revenue Share (%), by End-Use Industry 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (billion), by Type 2025 & 2033

Figure 33: Revenue Share (%), by Type 2025 & 2033

Figure 34: Revenue (billion), by Voltage 2025 & 2033

Figure 35: Revenue Share (%), by Voltage 2025 & 2033

Figure 36: Revenue (billion), by Production Technology 2025 & 2033

Figure 37: Revenue Share (%), by Production Technology 2025 & 2033

Figure 38: Revenue (billion), by End-Use Industry 2025 & 2033

Figure 39: Revenue Share (%), by End-Use Industry 2025 & 2033

Figure 40: Revenue (billion), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (billion), by Type 2025 & 2033

Figure 43: Revenue Share (%), by Type 2025 & 2033

Figure 44: Revenue (billion), by Voltage 2025 & 2033

Figure 45: Revenue Share (%), by Voltage 2025 & 2033

Figure 46: Revenue (billion), by Production Technology 2025 & 2033

Figure 47: Revenue Share (%), by Production Technology 2025 & 2033

Figure 48: Revenue (billion), by End-Use Industry 2025 & 2033

Figure 49: Revenue Share (%), by End-Use Industry 2025 & 2033

Figure 50: Revenue (billion), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Type 2020 & 2033

Table 2: Revenue billion Forecast, by Voltage 2020 & 2033

Table 3: Revenue billion Forecast, by Production Technology 2020 & 2033

Table 4: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Revenue billion Forecast, by Type 2020 & 2033

Table 7: Revenue billion Forecast, by Voltage 2020 & 2033

Table 8: Revenue billion Forecast, by Production Technology 2020 & 2033

Table 9: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 10: Revenue billion Forecast, by Country 2020 & 2033

Table 11: Revenue (billion) Forecast, by Application 2020 & 2033

Table 12: Revenue (billion) Forecast, by Application 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue billion Forecast, by Type 2020 & 2033

Table 15: Revenue billion Forecast, by Voltage 2020 & 2033

Table 16: Revenue billion Forecast, by Production Technology 2020 & 2033

Table 17: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue billion Forecast, by Type 2020 & 2033

Table 23: Revenue billion Forecast, by Voltage 2020 & 2033

Table 24: Revenue billion Forecast, by Production Technology 2020 & 2033

Table 25: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 26: Revenue billion Forecast, by Country 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue (billion) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Revenue (billion) Forecast, by Application 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue billion Forecast, by Type 2020 & 2033

Table 37: Revenue billion Forecast, by Voltage 2020 & 2033

Table 38: Revenue billion Forecast, by Production Technology 2020 & 2033

Table 39: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 40: Revenue billion Forecast, by Country 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue billion Forecast, by Type 2020 & 2033

Table 48: Revenue billion Forecast, by Voltage 2020 & 2033

Table 49: Revenue billion Forecast, by Production Technology 2020 & 2033

Table 50: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market research approach places a strong emphasis on primary research, constituting 70-80% of our data collection efforts. This involves extensive qualitative and quantitative interviews with key opinion leaders, industry experts, and stakeholders across the 4-inch SiC Epitaxial Wafer value chain. These in-depth discussions are crucial for validating secondary findings, obtaining firsthand market insights, understanding emerging trends, and gathering proprietary data points that are not publicly available. Our structured interview process, utilizing detailed questionnaires, allows us to extract comprehensive perspectives on market dynamics, competitive landscape, technological advancements, pricing strategies, and future growth opportunities.

Primary research participants are meticulously selected to ensure a balanced representation of the market ecosystem. Our engagement strategy targets the following company types and job designations:

Company Types Interviewed:

SiC Substrate & Epitaxial Wafer Manufacturers

Power Semiconductor Device Manufacturers

Epitaxial Deposition Equipment Suppliers

Advanced Materials R&D & Testing Firms

Key Stakeholders Interviewed:

VP of Technology & Product Development

Director of SiC Wafer Operations/Supply Chain

Lead Process Engineer, Epitaxy

Market & Business Development Manager, Power Electronics

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP of Technology & Product Development

30%

Director of SiC Wafer Operations/Supply Chain

30%

Lead Process Engineer, Epitaxy

25%

Market & Business Development Manager, Power Electronics

15%

Industry Ecosystem Breakdown

Company Type

Representation (%)

SiC Substrate & Epitaxial Wafer Manufacturers

40%

Power Semiconductor Device Manufacturers

30%

Epitaxial Deposition Equipment Suppliers

15%

Advanced Materials R&D & Testing Firms

15%

Secondary Research & Industry Benchmarking

The remaining 20-30% of our research is dedicated to robust secondary research and industry benchmarking. This phase involves a rigorous collection and analysis of publicly available data from authoritative sources. We leverage premium financial databases such as Bloomberg, Factiva, Hoovers, and PitchBook to gather company financials, investment trends, and strategic developments. Furthermore, government publications (.Gov), organizational reports (.org), and trade association data provide invaluable insights into regulatory frameworks, industry standards, and market statistics. Crucially, we strictly avoid data from other market research websites to maintain the independence and integrity of our findings.

Key secondary sources for this specific market include, but are not limited to:

Industry Associations & Regulatory Bodies:

SEMI (Semiconductor Equipment and Materials International) Source

ECPE (European Center for Power Electronics) Source

All gathered data is continuously updated to the date of purchase, ensuring that our market assessments reflect the latest available information and industry developments.

Demand Modeling & Market Estimation

Our market estimation methodology integrates both top-down and bottom-up approaches, complemented by multi-level data triangulation to ensure maximum accuracy and reliability. The top-down approach involves analyzing the total available market (TAM) for 4-inch SiC epitaxial wafers by segmenting it based on type, voltage, production technology, end-use industry, and geographic regions as defined in the report title. This macro-level view is then refined with specific market penetration rates and growth projections.

Concurrently, the bottom-up approach aggregates market size from granular data points. Key metrics and variables used for bottom-up calculation include:

Annual production volume of 4-inch SiC epitaxial wafers (in units or square inches) across key manufacturers.

Average Selling Price (ASP) per 4-inch SiC epi wafer, segmented by type (N-Type, P-Type), voltage (Below 650 V, 650-1200 V, etc.), and production technology.

Deployment rates of SiC power devices in crucial end-use industries (e.g., Electric Vehicles, renewable energy inverters, data center PSUs) and the corresponding 4-inch SiC wafer equivalent per application unit.

Capital expenditure plans and reported capacity expansions of leading SiC epitaxy manufacturers and integrated device manufacturers (IDMs).

These estimates are further triangulated by cross-referencing data from primary interviews, secondary sources, and our proprietary market models. The forecast period extends from 2026 to 2034, projecting market growth and trends over the long term.

Data Accuracy & Quality Check

Ensuring the highest standard of data accuracy and reliability is paramount. We guarantee an estimated data accuracy level of 85-90% for our market projections. This high level of confidence is achieved through a rigorous, multi-stage data validation process. All collected primary and secondary data undergoes systematic verification by our team of senior analysts. Any discrepancies are resolved through additional research or further expert consultations.

Our multi-level data triangulation process serves as the final checkpoint, comparing and synthesizing findings from diverse sources to identify and mitigate potential biases or inconsistencies. This comprehensive validation framework ensures that our market estimates and forecasts are robust, defensible, and reflective of the true market landscape for 4-inch SiC Epitaxial Wafers.

Frequently Asked Questions

1. What technological innovations are shaping the 4-inch SiC Epitaxial Wafer industry?

Advancements in Chemical Vapor Deposition (CVD) Epitaxy and hot-wall CVD methods improve wafer quality and efficiency. Research focuses on reducing defect density and increasing yield, crucial for high-voltage applications like 1200-3300V devices. Companies like Resonac and Coherent invest in materials science to optimize wafer properties.

2. What are the primary barriers to entry in the 4-inch SiC Epitaxial Wafer market?

Significant capital investment in advanced manufacturing equipment, proprietary epitaxy growth processes, and stringent quality control standards create high barriers. Expertise in SiC material science and strong intellectual property portfolios, held by established firms like Wolfspeed and SK Siltron, form competitive moats. These factors ensure product reliability for critical end-use industries.

3. How are pricing trends and cost structures evolving for 4-inch SiC Epitaxial Wafers?

Pricing is influenced by raw material costs, energy consumption for high-temperature processes, and R&D investments. Increased production volumes driven by an 18.04% CAGR may lead to some cost optimization over time. However, the specialized nature of SiC manufacturing keeps wafer costs relatively high compared to silicon.

4. How have post-pandemic recovery patterns impacted the 4-inch SiC Epitaxial Wafer market?

The market experienced robust recovery post-pandemic, driven by accelerated digitalization and demand for efficient power electronics in electric vehicles and renewable energy. Long-term shifts include increased reliance on resilient supply chains and regional manufacturing capabilities. The market is projected to reach $1.3 billion, indicating sustained growth.

5. What is the impact of the regulatory environment on the 4-inch SiC Epitaxial Wafer market?

Regulations related to environmental standards, material sourcing, and product safety significantly influence manufacturing processes and market access. Compliance with international standards for automotive and aerospace applications is critical. Export controls on advanced technologies also shape global market dynamics for SiC components.

6. Which factors are the primary growth drivers for the 4-inch SiC Epitaxial Wafer market?

Key growth drivers include the rapid expansion of electric vehicles (EVs) and hybrid electric vehicles, alongside increased adoption in renewable energy systems and data centers. Demand for efficient power management in automotive & transportation and energy & power sectors is a significant catalyst. The market is projected to grow at an 18.04% CAGR.