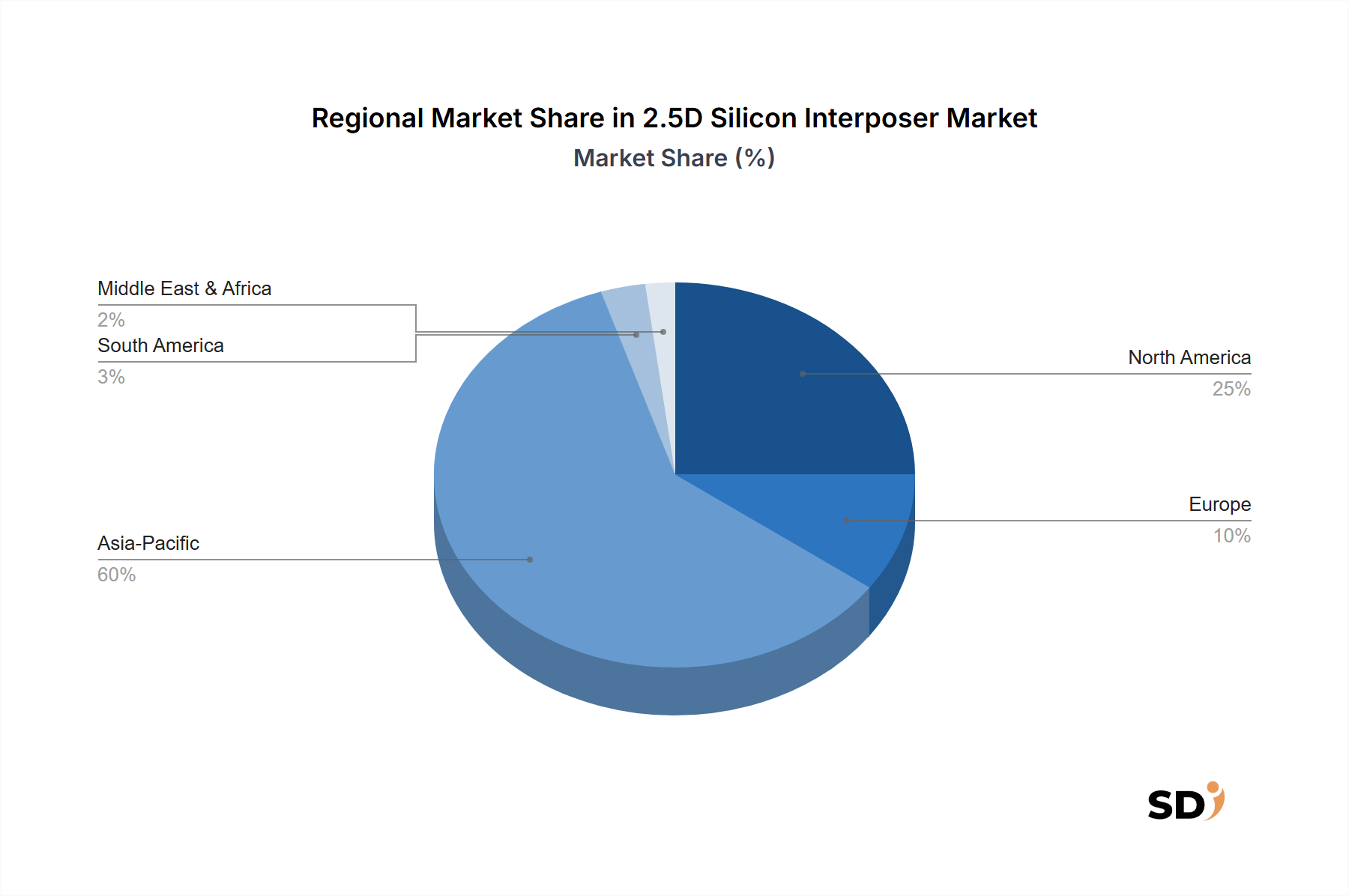

Regional Market Breakdown for 2.5D Silicon Interposer Market

The 2.5D Silicon Interposer Market exhibits distinct regional dynamics, largely influenced by the geographic concentration of semiconductor manufacturing, design houses, and end-use industries. The global landscape is dominated by a few key regions, each contributing uniquely to market growth.

Asia Pacific is undeniably the leading region in the 2.5D Silicon Interposer Market, accounting for the largest revenue share and also demonstrating one of the highest growth rates. This dominance is primarily driven by the presence of major foundries such as TSMC, Samsung, UMC, and GlobalFoundries, as well as leading outsourced semiconductor assembly and test (OSAT) providers like ASE, Amkor Technology, and Powertech Technology Inc. These companies possess the advanced fabrication and assembly capabilities essential for 2.5D interposer manufacturing. The region also hosts a significant portion of the global electronics manufacturing base and boasts rapidly expanding AI and High-Performance Computing Market infrastructures in countries like China, South Korea, and Japan. The burgeoning Consumer Electronics Market and Telecommunications Equipment Market in this region further fuel demand for advanced packaging solutions.

North America holds the second-largest share and is a crucial region for demand and innovation. The market here is primarily driven by the presence of major fabless semiconductor companies, leading hyperscale data center operators, and extensive R&D investments in AI, HPC, and defense applications. Companies like Intel, AMD, and NVIDIA, along with numerous startups, are at the forefront of designing high-performance processors that heavily rely on 2.5D interposers for HBM integration. This region is a major consumer in the AI Hardware Market and exhibits strong growth fueled by continuous technological advancements.

Europe represents a growing market, albeit with a smaller share compared to Asia Pacific and North America. The demand here is largely spurred by specialized applications in industrial electronics, the Automotive Electronics Market (particularly for advanced driver-assistance systems), and niche High-Performance Computing Market segments. European research institutions and companies are actively engaged in developing advanced semiconductor technologies, contributing to a steady, albeit slower, adoption rate of 2.5D interposers.

Rest of the World (RoW), encompassing South America, the Middle East, and Africa, currently holds a nascent share of the 2.5D Silicon Interposer Market. While there are emerging electronics industries and increasing digital infrastructure investments in these regions, the advanced manufacturing capabilities and demand drivers for 2.5D interposers are still in developmental stages. Growth in these regions is expected to be gradual, driven by global technology diffusion and localized growth in specific industrial or telecommunications sectors.

Overall, Asia Pacific is the fastest-growing region, simultaneously serving as the primary manufacturing hub and a significant demand center. North America remains the most mature market in terms of early adoption and advanced design, consistently pushing the boundaries of what 2.5D interposer technology can achieve.